The global markets have experienced a late summer swoon, blamed on factors including concerns about slowing growth in China and the impact of a potential increase in US interest rates this autumn. Whatever the reason, we think it is important to put these types of market corrections in context, remain calm and look for potential opportunities.

We don’t know for sure whether the market rout has ended, or has further to go. We would note that many of the world’s stock markets have not seen a significant correction in many years. Individual markets like Brazil or Russia are down more than 30% this year, but many others have not experienced losses that we would classify as being in a bear market. General pessimism and uncertainty prevails in markets right now, so it is possible some markets could fall further before we see stabilization. Nevertheless, over the last 20 years or so, our team has witnessed a general increase in volatility in all markets (equity, commodities and fixed income) brought on, we think, by increased use of derivatives and the strong influence of changing government policies spread by an exponential increase in news flow on the Internet.

We do know valuations in a number of markets and sectors were getting quite expensive, so this market downturn isn’t all that surprising to us. Most notably in China, it was clear to us that the domestic A-Share market had seen intense speculation that had taken over and pushed that market up to unsustainable highs in record time on the back of government encouragement. With the inevitable denouement taking place, Chinese investors are now complaining about their market losses and the government has been active in trying to revive the market’s fortune.

China’s central bank has cut interest rates this week (the fifth rate cut since November), and has loosened reserve requirements. There isn’t a whole lot central bankers can do when the money that is already in the system isn’t being put back into the market; not only because confidence has been lost but also because of various prudential requirements, the banks have not increased lending. China’s central bank hopes its latest measures will enable the release of money from the banking system.

My main message during times like these? Don’t be afraid to buy when everyone else is selling. But remember also that the best time to buy is when all the sellers have finished their selling—which may be easier said than done!

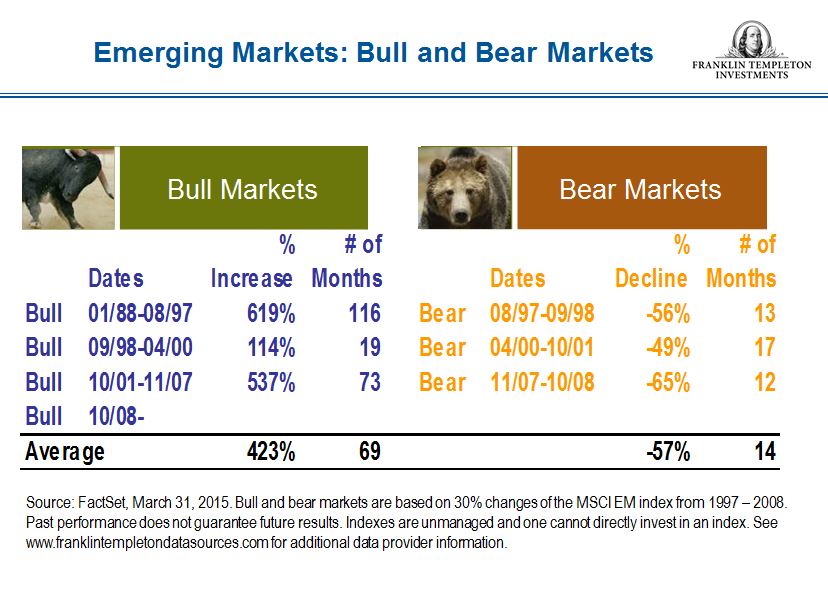

Bulls and Bears and Opportunities

While market declines can be painful for investors, we like to view them as periods of opportunity; we look to pick up bargains in anticipation of an eventual market recovery.

I have studied stock markets in emerging countries and found that their bull markets have generally lasted longer than their bear markets, and the bull markets have tended to go up more in percentage terms than bear markets went down.1 Of course, how emerging markets behaved in the past does not necessarily predict how they will behave in the future, but I believe one must take a long-term view and average your investments over a period of time—attempting to time the market can be a frustrating exercise. It can take fortitude to invest when the outlook is bleak and others are selling, but that’s often when the best values can be uncovered—if you do your homework.

That said, we use market corrections like the one we are experiencing to very cautiously and very selectively pick up stocks for our portfolios. Right now, we are particularly interested in consumer-oriented stocks in China and a number of other emerging market countries, because that is where we see growth long term.

Our Views on China Haven’t Changed

Despite recent market volatility, we consider the long-term outlook for China’s market and economy to be good. We don’t view this recent correction as the start of any sort of economic or market collapse underway, and it doesn’t change our view on investing there.

I would like to highlight some reform efforts in China that we believe appear to be positive:

- Ongoing efforts are being made to rebalance the economy away from exports and investment and toward domestic consumption, boosted by a continued rapid rise in wages.

- Plans to address overcapacity and promote an open, fair and transparent market suggest a more robust attitude to long-term profitability of state-owned enterprises (SOEs). While SOE reform has been a bit slow, we expect continued progress.

- We believe a more commercial approach among managements of SOEs could have a positive influence; we recently spoke with a manager from a major Chinese oil company who said they are implementing a system where pay is tied to performance. That’s the type of thing we are looking for, and view as positive.

- Monetary policy easing in China, the eurozone and Japan is supportive of the financial system and the sustainability of debt.

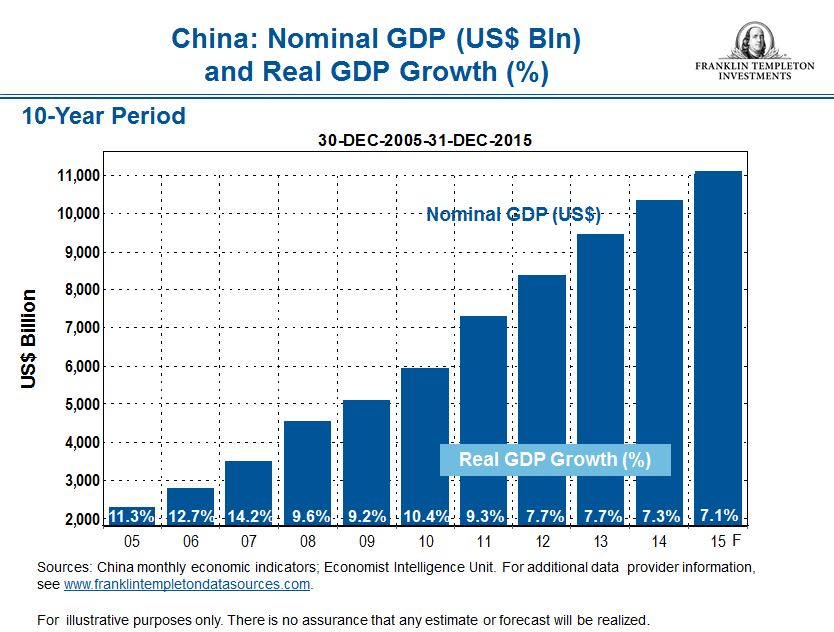

A lot of attention has been given to slowing gross domestic product (GDP) growth in China. It bears repeating—China’s growth rate may be slowing, but one of the things that gets lost in translation is that while the percentage increases in the economy are indeed slowing down, but the actual dollar amounts are going up. When China’s economy was growing at 10% in 2010, about US$844 billion was added to the economy, but with growth at 7.7% in 2013, US$986 billion was added.2 I would also emphasize that 7% growth is nothing to sneeze at, either, given the size of China’s economy. It should not be a shock to see growth slow.

I recently visited a mega-shopping mall in China, “The New Century Global Center in Chengdu.” This 1.7 million square meter mall—more like a small town—contains offices, shops, more than 800 hotel rooms, a skating rink and a water park with an artificial beach and an artificial sun. During my visit, the mall was packed and hotel rooms full. This provided confirming evidence to me of the retail sales numbers we have seen in China recently, which remain fairly robust. More importantly given the high admission price (equivalent of about US$25) to the full-to-capacity indoor water park, and the brisk business I saw at the major department store in the mall, it was clear to me that spending capacity is good.

Anticipating a US Rate Hike Ahead

In our view, the downturn in emerging markets generally this year can also be attributed to fears about an interest rate increase in the United States, which will act to stem liquidity. While we don’t know when the Federal Reserve (Fed) will start to tighten policy, the markets seem to be factoring it in. The uncertainty of the timing and degree of increases is what the market doesn’t like, so while there may be additional volatility when the Fed does raise rates, I would expect some relief as the uncertainty eases.

The two largest emerging market economies, China and India, seem to us to be better positioned to cope with rising US interest rates than some other emerging economies, as they have internal growth drivers that are not as dependent on the United States. I believe China and eventually India will be the main drivers of global growth rather than the United States or Europe. We seem to be in a transitional stage of that change right now. China represents the second-largest economy in the world, and even if we were to assume a 5% growth rate, it is still much more than either the United States or the eurozone has been able to achieve in many years.

Looking at emerging Asia generally, we believe a combination of rapid economic growth, generally strong national finances and economic fundamentals have created an attractive landscape for equity investors. Expectations of high economic growth rates in emerging Asia (driven by China and India) remain a key attraction to us and we believe such growth rates will be comfortably in excess of developed market growth rates in 2015 and beyond.3 Moreover, many Asian markets, among them China, India, Indonesia and South Korea, have announced or embarked upon significant reform measures differing in details, but generally aimed at sweeping away bureaucratic barriers to economic growth, encouraging entrepreneurship and exposing inefficient industries to market discipline. Most are also looking to rebalance economic activity away from export- and investment-heavy models to become more oriented toward consumer demand.

“Successful Investing Is Not an Easy Job”

Last but not least, I would like to emphasize that we are fundamental, bottom-up stock pickers, and the country and sector composition of our portfolios are the by-product of our stock selection process. Of course, we aren’t infallible, and our timing may not be in sync with the mainstream media view that is focused on short-term news and outcomes. What’s been happening in the energy sector is a case in point. The swift fall in crude oil prices that began last year surprised many portfolio managers and analysts, and many investors have fled companies in the energy sector. In our view, energy price volatility will likely always be present, but long-term demand growth remains intact. Despite witnessing softer commodity prices in general in recent years, we continue to invest in the sector and are focused on low-cost producers that we believe can withstand periods of lower prices. We also believe that many of these companies are trading at attractive valuations, appear to have solid fundamentals and should be more resilient during downturns.

At times, it can be quite difficult to withstand periods of uncertainty. But as Sir John Templeton once said: “Successful investing is not an easy job. It requires an open mind, continuous study and critical judgment.”

Mark Mobius’s comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding any country, region market or investment.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FTI affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including possible loss of principal. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets.

___________________________________________

1 Source: FactSet, March 31, 2015. Bull and bear markets are based on 30% changes of the MSCI EM index from 1997–2008. Past performance does not guarantee future results. Indexes are unmanaged, and one cannot directly invest in an index. See www.franklintempletondatasources.com for additional data provider information.

2 Source: China monthly economics indicators; EIU (Economist Intelligence Unit).

3 There is no assurance that any estimate or forecast will be realized.

© Franklin Templeton Investments

© Franklin Templeton Investments