Rising Rates and the Case for Leveraged Loans

The clamor around the timing of the first increase in US interest rates in more than seven years is reaching a crescendo, as the all-important September meeting of the Federal Open Market Committee (FOMC) draws closer. This may be causing investors to rethink their investment strategies. Mark Boyadjian and Reema Agarwal of Franklin Templeton Fixed Income Group take a look at the implications of a changing-rate environment for investors in bank loans, also called leveraged loans.

For certain investors—in particular pension funds and insurance companies that tend to follow a more cautious investment strategy—the extended period of record or near-record low US interest rates has been a thorn in the side. Many such institutions rely on investment returns to meet commitments or drive profitability and have been beleaguered by the low yields inherent in the current environment.

As a result of a search for yield among such constituents, some of these institutions have been looking at asset classes outside conservative low-yielding government and corporate bonds. One of these has been leveraged loans or bank loans, which offer the potential to provide a fairly attractive level of income with minimal interest-rate risk, because the coupon adjusts. For example, at the end of 2014, the Credit Suisse Leveraged Loan Index had an average coupon greater than 4.75%, duration1 positioning of less than 0.25 years, and an average dollar price below par.2

We believe concern regarding anticipated increases in US interest rates is going to continue to have implications for fixed-rate and floating-rate assets. In that context, our view is that fixed-rate assets—particularly those with a duration of five years or shorter—may be experiencing material principal declines as a result of the interest-rate risk they possess.

While our outlook for the corporate credit market generally is positive for the balance of this year, we’re growing increasingly concerned about the potential credit risks that could develop in 2016 and 2017. Our concerns stem from the sense that floating-rate debt, like many asset classes, is sensitive to the laws of demand and supply.

In the context of rising rates, we believe many investors will seek to shed their duration and flock to assets that they perceive as having yield without duration, which may include leveraged loans.

Bank loans may offer a few key characteristics that may look attractive to many investors within the context of a rising rate environment.

- The duration on a leveraged loan is typically very low. If interest rates rise, price sensitivity is generally much less relative to a high-yield bond alternative.

- Leveraged loans are considered below-investment-grade in credit quality, but their “senior” and “secured” status can provide investors/lenders a degree of potential credit risk protection.

- Historically, leveraged loans have had a relatively low or even negative correlation3 to traditional fixed income vehicles such as government bonds.

- The floating-rate feature in leveraged loans means that as short-term interest rates go up, the corresponding income on loans typically should go up as well.

Supply and Demand

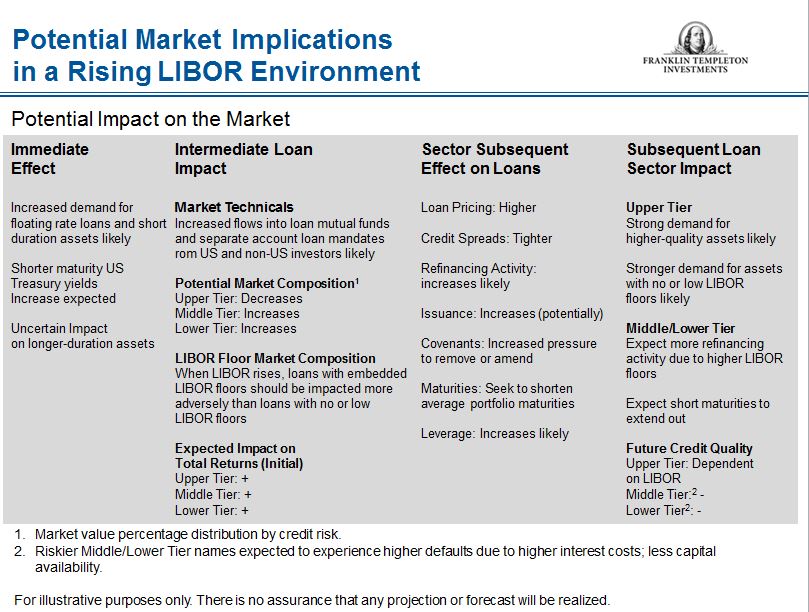

Interest rate dynamics can have important implications in terms of supply and demand for the asset class. Traditionally, leveraged loans have derived the majority of total return from income. The majority of that income is derived from the underlying benchmark; LIBOR (the London Interbank Offered Rate) is the benchmark for US dollar-denominated term loans. Euro-denominated loans use EURIBOR, a similar measure to LIBOR. LIBOR represents the average interest rate estimated by leading banks in London that the average leading bank would be charged if borrowing from other banks, and it tends to track movements in the US Federal Funds rate. As a result, LIBOR would be expected to rise as US interest rates rise. In a rising LIBOR environment, we expect the demand for leveraged loans as an asset class could likely exceed the supply.

When you put that in the context of three other crucial issues—rising leverage levels, increasing covenant-lite issuance4 and record collateralized loan obligations formation—what we see occurring is a ballooning of the level of credit risk as a result of the increase in demand. A covenant-lite loan is a type of loan whereby financing is given with limited restrictions on the debt-service capabilities of the borrower.

Rising Leverage Levels

In general, at this time, coverage levels—the notional ability to service debt— appear to be very comfortable.

Current leverage levels are approaching the historical peaks seen in 2007, but with historically lower interest rates, according to our analysis, companies in general appear well able to cover their interest costs at this time. In this context, leverage refers to the amount of debt used to finance a firm’s assets.

It’s also our view that adjustments to earnings before interest, taxes, depreciation and amortization (EBITDA) are likely to increase over time, so it is likely this leverage may be understated versus companies that are coming to the loan market at this point.

Leverage can increase for one of two reasons:

- The borrower can maintain their earnings but increase the amount of debt outstanding.

- The amount of debt can remain constant but the earnings can decline.

When it comes to the demand/supply situation, our concern is that there will be an increase in the total amount of debt outstanding—either senior or total—and in our opinion, that could cause a situation where credit quality may deteriorate and investors may in turn receive less compensation for it.

This is where credit quality comes in. Companies that are at the higher end of the company credit-quality spectrum should have a better ability to handle the eventual rise in interest rates. Conversely, we think that companies in the middle and lower tiers of credit quality are likely to suffer more of the pain when interest rates rise.

Continuously Callable

Although leveraged loans are very much like high-yield credit, they are different in important ways: They are floating rate versus fixed, and they are continuously callable. That means borrowers have the option to refinance their loans.

This influences the supply/demand concept and the deterioration of credit quality, because as demand exceeds supply and loans begin to trade above par, many borrowers will exercise their option and refinance their loans at a lower spread. This has two primary effects for investors: It caps principal appreciation potential, and it reduces the income they are receiving for the same level of credit risk.

When one sees higher demand levels, one would expect to see higher issuance levels. Our view is that issuance would be more rated toward the middle credit quality and the lower credit quality subspace of the loan market. As a result, we think the market composition would likely change to increase middle tier and lower tier.

Covenant-Lite

Generally as issuance and demand increases, companies would typically try to remove covenants or try to come to market without covenants.

While so-called covenant-lite loans are generally thought to be riskier since they include fewer potential opportunities to actively mitigate credit risk deterioration, it is helpful to view their proliferation in the context of our current investment climate. During periods of excess demand, it has not been historically uncommon to experience various forms of asset price inflation. With respect to leveraged loans, this can take the form of increased issuance of loans characterized by either higher leverage ratios or fewer, if any, covenants.

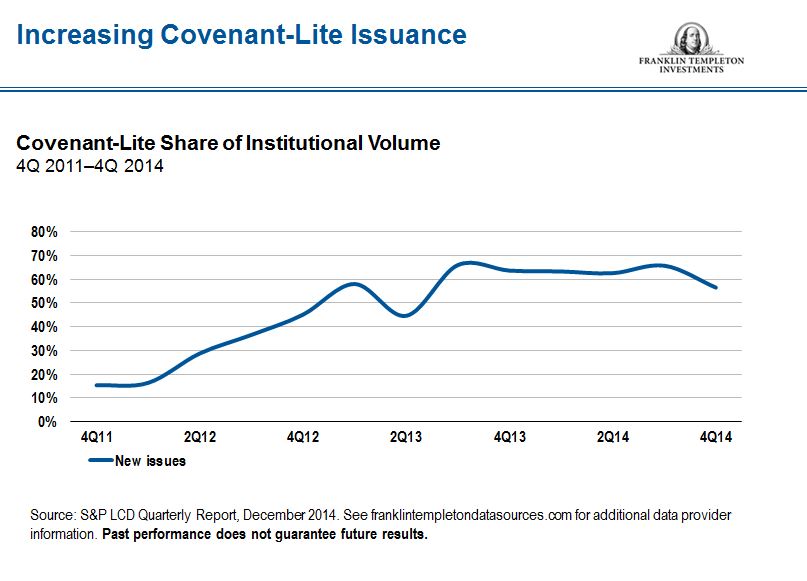

Covenant-lite loans formed 7% of the leveraged loan market in 2006.5 They comprised 20% of the market by 2012.6 At the end of May 2015, they represented 59%.7 Of the new issues that came to the market in 2014, 63% were covenant-lite loans.8 So, clearly there has been a trend to strip away covenants when companies come to the market.

The key point to note here is that the percentage of covenant-lite loans differs by credit quality. At the higher end of the credit-quality spectrum, the percentage of covenant-lite loans has tended to be lower than in the lower and middle tiers. Middle-tier companies have 68% covenant-lite issuance; in the upper tier it’s 46%.9

This is critical in our view. We think that covenants should be seen in the context of the overall credit quality. As an investor, we would be less concerned about the lack of covenants for a higher credit-quality issuer than for a company that we felt needed closer monitoring of its performance.

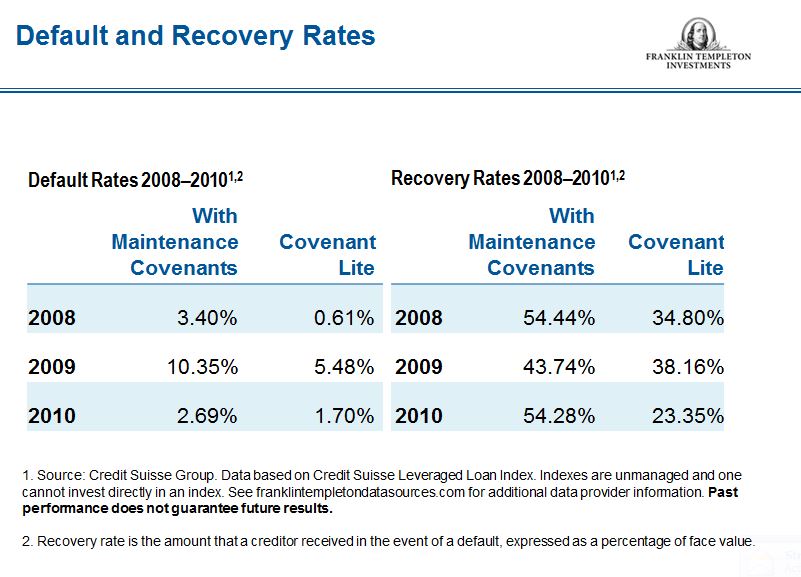

It is also worth noting that historically covenant-lite loans have had a lower payment default rate than covenanted loans.10

Of the loans that did default, the recovery levels of covenant-lite loans were lower than those of covenanted deals. So we think that has implications for when the next credit cycle turns, and we are trying to position the portfolio accordingly. In particular, given what we see in the loan market, we’re attempting to position our portfolios to move up in credit quality.

Eventually, we think the market will morph into one where you will see a greater percentage of lower- and middle-tier credit constituents and overall credit quality of the market will be lower than it is currently.

Collateralized Loan Obligations (CLOs)

CLOs are the largest investor group in the institutional loan market, representing 62% of the investor base in the loan market.11 In 2014, we saw record deal formation of $124 billion,12 and we believe CLO formation will continue to be strong through the remainder of 2015.

However, new US regulations due to come into effect in 2016 would require managers of CLOs to support transactions in a more material way; therefore, we think CLO formation is likely to decline starting in 2016. The rules are designed to help mitigate the risk of a new credit bubble in the leveraged loan market, with a specific focus on rising leverage levels and the proliferation of covenant-lite loans. As a result, we expect the fall in issuance to be more pronounced in the upper-tier, higher-credit quality space, because that’s where CLOs are a bigger player and LIBOR is a bigger component of income for upper-tier loans.

Peak Default Cycle

Going into what we think will be a peak default cycle sometime in 2016 or 2017, we would expect investors to be looking to own the shortest default risk as possible, particularly for lenders with lower-tier or middle-tier credit risk.

We would therefore tend to be biased toward investing in loans that have higher credit quality. By the time we are in the environment we expect in 2016 and 2017, we anticipate seeking to position our portfolios to attempt to mitigate the increasing risk of the peak default cycle, while also potentially benefitting from a rising LIBOR.

We would also note that while we expect performance of the asset class to be good initially because of increased demand, the income levels could actually decline before rising due to LIBOR floors. The concept of a LIBOR floor may be confusing investors in terms of the compensation they are receiving. The LIBOR floor helps ensure that investors receive some minimum base level of compensation, in addition to the credit spread the bank loan may pay.

The primary risk an investor accepts when investing in bank loans is credit risk, and the compensation they receive is the spread over LIBOR. Given that LIBOR is currently so low (0.33%),13 many borrowers have agreed to pay a LIBOR level that’s above the current rate.

Many investors look at the LIBOR floor with the floating-rate spread as their compensation for the credit risk. That’s a mistake in our opinion. As LIBOR begins to rise, investors would want to participate in the income stream that will flow. But the floor becomes worth less as LIBOR rises.

So in a rising LIBOR environment, we would expect investors to be looking for loans with low or no LIBOR floors.

Comments, opinions and analyses expressed by the investment manager(s) are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Bond prices generally move in the opposite direction from interest rates. In general, an investor is paid a higher yield to assume a greater degree of credit risk. High-yield bonds involve a greater risk of default and price volatility than other high quality bonds and US government bonds. High-yield bonds can experience sudden and sharp price swings which will affect the value of your investment. Floating-rate loans and debt securities tend to be rated below investment grade. Investing in higher-yielding, lower-rated, floating-rate loans and debt securities involves greater risk of default, which could result in loss of principal—a risk that may be heightened in a slowing economy. Interest earned on floating-rate loans varies with changes in prevailing interest rates. Therefore, while floating-rate loans offer higher interest income when interest rates rise, they will also generate less income when interest rates decline. Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value.

________________________________________________________________________

1 Duration is a measurement of a bond’s—or a portfolio’s—sensitivity to interest-rate movements. Par value represents the face value of a bond.

2 Source: Credit Suisse, “2015 Leveraged Finance Outlook and 2014 Annual Review,” February 19, 2015.“Leverage Finance Strategy Update,” April 2, 2015. Indexes are unmanaged, and one cannot directly invest in an index. Past performance does not guarantee future results.

3 Correlation measures the degree to which investments move in tandem. Correlation will range between 1 (perfect positive correlation, moving in the same direction) to -1 (perfect negative correlation, moving in opposite directions)

4 Source: S&P LCD Quarterly Report, December 2014. See www.franklintempletondatasources.com for additional data provider information.

5 Source: Credit Suisse Group, July 2015.

6 Ibid.

7 Ibid.

8 S&P LCD Quarterly Report, December 2014. See www.franklintempletondatasources.com for additional data provider information.

9 Source: Credit Suisse Group, July 2015.

10 Source: Credit Suisse Group. Data based on Credit Suisse Leveraged Loan Index. Indexes are unmanaged and one cannot directly invest in an index. Past performance does not guarantee future results.

11 Source: S&P LCD Quarterly Report, December 2014. See www.franklintempletondatasources.com for additional data provider information.

12 Ibid.

13 As of August 21, 2015.

© Franklin Templeton Investments

© Franklin Templeton Investments