US equities reached a major inflexion point in the year 2000. It was historic because it represented both a secular and primary reversal. A primary trend revolves around the business cycle and typically lasts 2-3 years, whereas a secular one lasts much longer and embraces several cycles. Our objective here is to revisit an article published earlier this year in which we pointed out some ominous signs for US equities. At that time some trend reversal signals, such as negative long-term moving average crossovers, were required as confirmation. Those signals have now been given, which is why the odds favor July 2015 as marking both a cyclical turning point and the start of the third down leg in the current secular bear market. Let us begin with a few words on secular price movements, and then proceed to examine the primary trend.

A realistic way of looking at secular trends in equities

Two hundred years of financial market history shows that secular trends for bonds, stocks and commodities last on average between 18-20 years. Some, such as the 8-year 1921-9 secular bull in equities are shorter and others, such as the 45-year post war secular uptrend in bond yields, evolve over a much longer period. It is not an exact science.

Many argue that the current secular trend is bullish because the S&P, in July 2015 was approximately 40% above its 2000 high. How can that possibly be a bear market? We think a more realistic way of looking at things is to measure these long-term price movements in terms of purchasing power. For example, if stock prices double over a 10-year period and the cost of living jumps by a similar amount, investors are no further ahead. Nominal prices give the illusion of greater prosperity, but when capital gains taxes are taken into consideration investors are actually worse off. Using inflation adjusted prices as our benchmark; the S&P was trading approximately 6% below its 2000 peak at the end of August. Chart 1 shows that the July high was very close to the 2000 peak. Previous highs and lows often represent potential support/resistance areas, so the July reading represented an ideal place for expecting a major turning point.

Chart 1 also compares the US to the world in the form of the MSCI World Stock ETF, adjusted by the G20 CPI. It is fairly evident that the secular bear since 2000 has been a global affair, as inflation adjusted equities have been working their way irregularly lower at each subsequent cyclical peak. Note also that the arrow, which also reflects a down trendline since 2000, became resistance in both 2007 and 2015.

Chart 1 Inflation Adjusted US versus Global (Source Reuters/OECD)

Inflation adjusted US and global equity prices experience similar secular price movements.

A second reason for believing that the secular bear is still intact arises from the fact that previous secular movements in US equity prices have been associated with multi-decade swings in sentiment, as market participants alternate between euphoria and despair. We can measure these mood swings using Robert Shiller’s famous P/E ratio (Chart 2). A high reading means investors are willing to pay an excessive price for $1 of real earnings. It is a strong vote of confidence that investors are expecting earnings to continue to grow, otherwise why would they be prepared to pay such an excessive price at a time when they are highly risky? By the same token, at secular lows, market participants are extremely pessimistic and are so disgusted with equities that they demand to be paid handsomely for those same stocks, the perceived outlook for which is now considered to be perilous. That is what 18-20 years of falling real prices does for you! In other words, the extremely low readings in the P/E ratio signal the capitulation or give-up phase for equities, thereby establishing a firm psychological foundation for the subsequent secular bull. The proverbial wall of worry is at its tallest and most threatening at such times.

There are two things worth noting about the current position of the indicator. First, the 2000-?? secular bear has yet to experience the Full Monty of fear, despair and pessimism, seen at previous secular lows; i.e., the indicator has yet to fall to the 6-7 times P/E typically seen at a secular low. Second, the August reading was well above the (red) excessive value/over believed optimistic level. It is therefore consistent with a market peak.

Chart 2 Inflation Adjusted US Stocks versus the Shiller P/E (Source Reuters/Yale University))

Stock prices experience multi-decade swings in psychology as reflected by major shifts in valuation.

Ominously Positioned Long-term Cyclical Indicators

- Stock versus Bond Returns

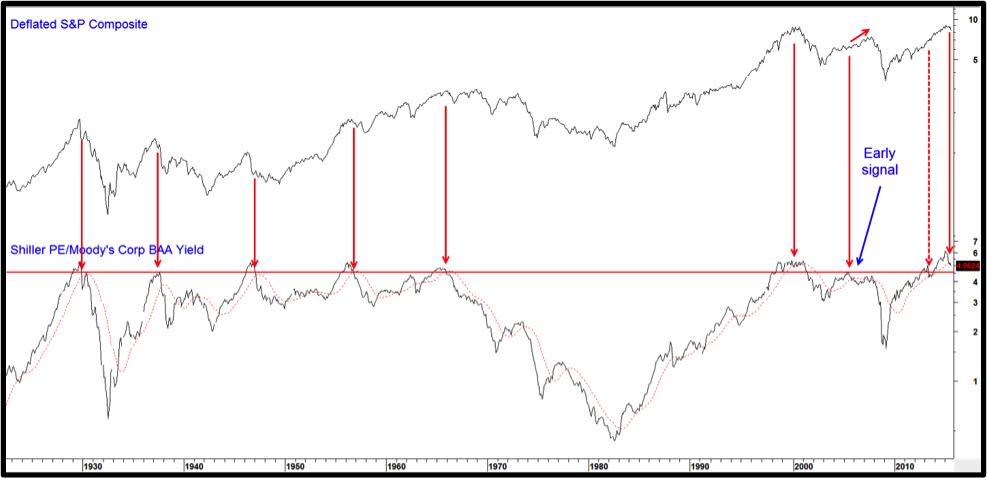

Chart 3 compares price to earnings relationship on stocks, as reflected in the Shiller P/E, to the yield on Moody’s corporate BAA quality bonds. A high reading tells us that stocks are overvalued relative to bonds and vice versa. The level of sentiment may tell us whether stocks are vulnerable or represent an attractive purchase. However, it is a change in direction of sentiment that signals when equities are likely to rise or fall. In this respect the arrows indicate those periods when the ratio crosses below its MA or the overstretched +5 line as these conditions provide a reliable signal that the sentiment pendulum has begun to reverse. At the August close the ratio was marginally below its average, thereby triggering a bearish signal. A review of the chart shows that the majority of such signals were reliable. There were only two false negatives in 2005 and 2013. A charitable interpretation would have the 2005 signal as an early one, but there is no getting around the 2013 failure. Even so, the latest MA penetration still leaves a 6 or 7-1 probability of it working, depending on which way the 2005 signal is interpreted.

Chart 3 Inflation Adjusted US Stocks versus a Stock/bond Valuation Ratio(Source Reuters/Yale/Moody’s)

Reversals in the stock/bond relationship from overstretched levels consistently signal bear markets.

- The 120% Rule

When stocks respond to falling rates by advancing a very favorable environment for equities is put in place. At Pring Turner Capital we call this the 120% rule, because when it is in force on the bullish side, gains are substantial and drawdowns relatively small. This condition comes into force when the yield on 3-month commercial paper crosses below its 12-month MA and the S&P votes its approval with a move above its 12-month average. Such periods have been flagged with the green highlights and have achieved monthly annualized gains of 16% since 1900. The model stays bullish until one of those conditions reverses, in which case it moves into a neutral (gray) condition. The commercial paper yield moved above its MA some time ago, but in August the S&P responded to this negative monetary development with a bearish cross of its own. The model is now in a negative (red) mode. This represents one of the worst environments to own equities as they have experienced a monthly annualized rate of return of close to -10% since 1900. The model tells us nothing about the magnitude or duration of the decline, nor does a neutral condition guarantee against losses, as you can see from the 1931, 2002 and 2008-9 periods. What it does tell us, is that when the commercial paper yield is above its MA and the S&P is below its average, stocks are extremely vulnerable. More to the point, the chart indicates that this condition almost invariably occurs during the course of a bear market.

Chart 4 The “120%” Model (Source Reuters/Federal Reserve)

When interest rates are above, and the S&P is below their respective 12-month moving averages equities are extremely vulnerable.

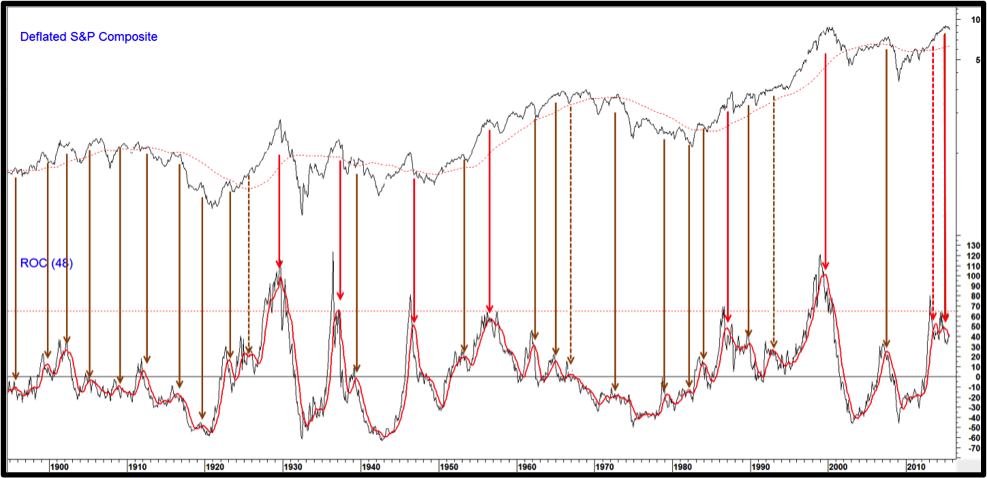

- The 48-month ROC of Real Stock Prices

Chart 5 compares inflation adjusted equities to their 48-month ROC, or more specifically to the 12-month MA of that momentum time span. The concept is that stocks move in a regular cyclic rhythm around the 4-year business cycle. Using a 48-month time span therefore helps to filter out most intermediate market setbacks until the cycle has had a chance to run its course. The red arrows tell us when the MA (red plot) reverses to the downside after the ROC itself has moved above the +65% overbought zone. These situations have a tendency to reflect the most extreme moves in crowd psychology, when prices are at their most vulnerable. Seven such signals have been triggered since 1890. All but the one in 2013 were followed by bear markets. In two cases (1929 and 2000) the market tops proved to be secular in nature. The brown arrows merely flag regular reversals by the MA i.e. those not associated with extreme ROC readings. In total there have been 24 signals, only three of which proved to be false. The recent drop in the MA again warns of equity market vulnerability.

Chart 5 Deflated US Equities versus a 48-month ROC (Source Reuters)

Reversing momentum warns of long-term equity market vulnerability.

1.Industry Group Diffusion

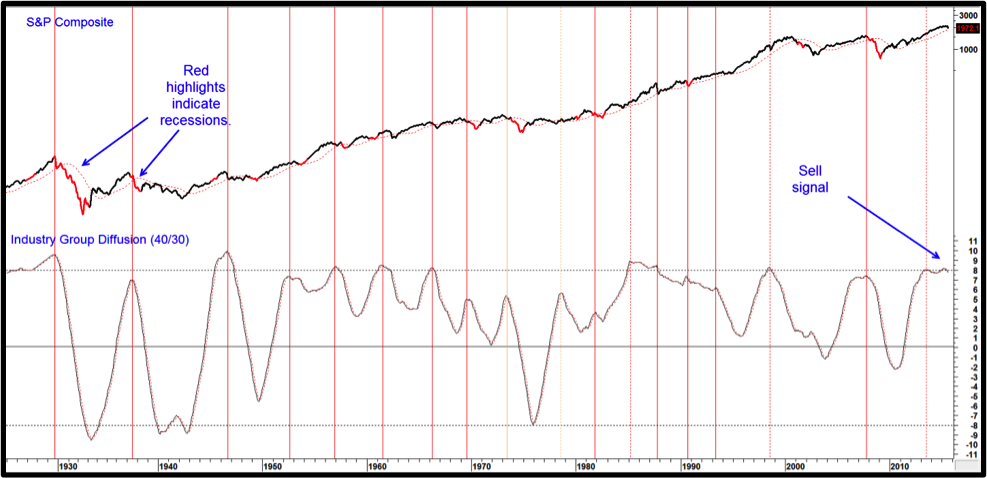

Finally, Chart 6, shows us that long-term industry group momentum has also triggered a sell signal. This series monitors a basket of S&P industry groups that are above their 40-month MA’s. The resulting calculation is quite jagged, so the data have been smoothed with a 30-month MA. Sell signals are triggered when it experiences a negative 4-month MA crossover (the red dashed line) from above the equilibrium level. The solid vertical red lines indicate valid, and dashed ones false signals. July’s marginal sell signal has now turned into a more decisive one and is a further indication that owning equities is very risky at the present time.

Chart 6 The S&P Composite versus Industry Group Momentum (Source Reuters/S&P)

Peaking industry group momentum warns of a more selective market ahead.

Equities and the Economy

The market’s relationship to changes in the level of economic activity is of paramount importance. In almost all cases, equities rally during a recovery, and sell-off during recession. One notable exception developed in the late 1920’s when equities rallied during a recession. Another developed in 2002, when prices declined in the face of a recovery. That disconnect was likely caused by the unwinding of the tech bubble. Generally speaking, the more severe is the economic contraction, the nastier the bear market. For example, in 1966 the growth rate of the economy slowed but a recession was avoided. The market escaped with a shallow 10-month decline. Compare that to the sharp economic contractions, say in 1974 and 2008, which experienced devastating bear markets.

The moral of the story is that it is very unlikely that a sustainable and deep market decline will take place unless the economy experiences a severe recession. The problem is that the lead time between market peaks and the onset of a recession has varied from none in 1929 to 12-months in 1956. Indeed, lead times of 7-9-months are not at all uncommon, which means that a bear market can be well underway before it is realized that a recession has begun. Almost no one is currently forecasting a recession, because pretty well all of the widely followed leading indicators are continuing to point north, but then, economists as a group have never been very good at identifying such turning points.

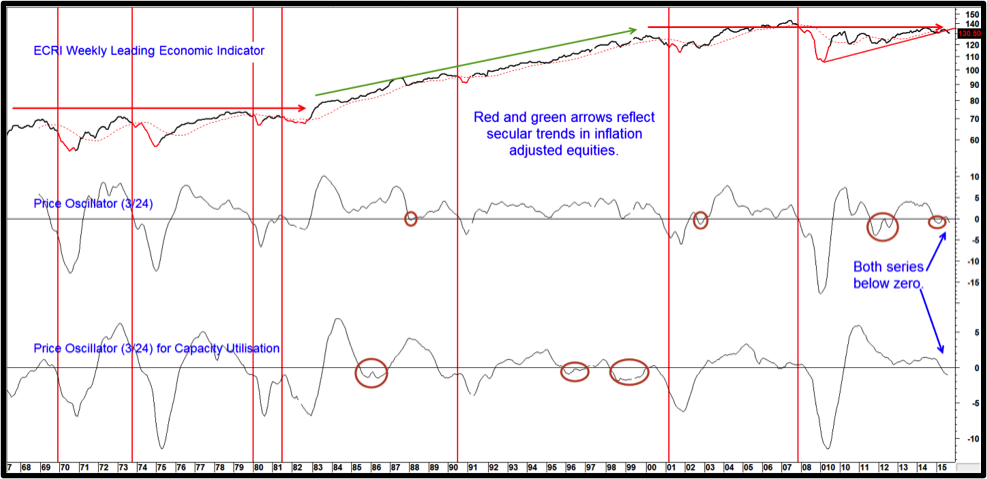

Chart 7 highlights previous recessionary periods in red and flags their onset with the vertical lines. The one green and two red arrows highlight the three secular trends in equities since the 1960’s. The two secular bears were associated with a range bound indicator reflecting structural problems. This compares to a rising trend during the 1982-2000 secular bull.

From a cyclical aspect, you can see that both the momentum of the ECRI Weekly Economic Indicator and capacity utilization have both fallen to levels consistent with recessionary conditions. The ECRI WLEI itself has ruptured its 2009-2015 recovery trendline. The ellipses show periods when one or the other momentum series has fallen into negative territory, but the economy has avoided recession. Currently both series have slipped into negative territory. All other previous situations of this nature have been associated with a recession.

Chart 7 ECRI Weekly Economic Indicator and Two Momentum Series

Two price oscillators are warning of weakness. (Source ECRI/Federal Reserve)

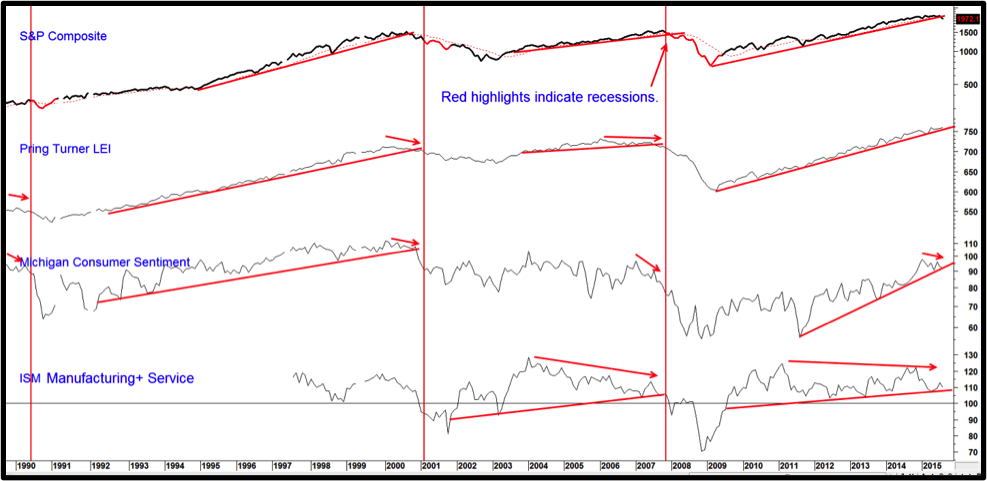

Chart 8 compares the S&P to three economic indicators, our own Pring Turner Leading Indicator, the University of Michigan Consumer Sentiment and a composite indicator combining the ISM Manufacturing PMI with its service industry counterpart. The Pring Turner series has led each recession since 1953, but is not yet showing weakness. Nevertheless it is very close to its recovery trendline. It would not take much to result in a penetration. Michigan Consumer Sentiment, another leading indicator, is currently right at its breakdown point. Finally the ISM manufacturing/service “combo” indicator is also in a finely balanced state. This chart is certainly not forecasting a recession, but it is evident that these indicators are in a fairly precarious position. Slight weakness from current levels could tip the balance in a negative way in which event things could unravel fairly quickly, certainly within the common 7-9-months lead time between market peaks and the onset of a recession.

Chart 8 S&P Composite versus Three Economic Indicators (Reuters/ISM)

Three economic indicators are at key juncture points.

Conclusion

Evidence continues to point to an extension of the secular bear market in inflation adjusted equities, both in the US and the rest of the world. That does not necessarily mean that the 2009 lows will be taken out but sufficient primary trend technical indicators have turned negative to conclude that investors should adopt a very defensive position. Current readings of most leading economic indicators argue for at least a slowdown but at the moment, fall short of signaling a recession. If that began to change the probability of a severe bear market would be greatly enhanced.

Martin Pring

Martin Pring is Chairman of Pring Turner Capital and publisher of The Intermarket Review, a monthly synopsis of the world’s principal financial markets.