President Obama upped the ante on his pledge to reduce the US carbon footprint last month when he and the Environmental Protection Agency unveiled new regulations calling for a substantial cut in carbon emissions from power plants in the next decade and a half. The new rules—and the protests that followed—may have investors wondering how the Clean Power Plan potentially may affect the utilities sector. John Kohli of Franklin Equity Group identifies the types of utility companies that will likely be challenged by the proposed regulations and which companies have already shifted to a renewables focus, generating forward-looking investment opportunities.

Ambitious plans to cut national carbon dioxide (CO2) emissions by nearly a third by 2030, which were unveiled in August by the Obama administration, have provoked intense opposition from coal-dependent regions of the United States, although the response of the utilities sector has been more muted.

As investors, we have found that in general, the most forward-looking utilities have already started reducing emissions by using less coal power and more sources of renewable energy. We also recognize that as a result of the provisions of the Clean Power Plan (CPP), utilities that are heavily reliant on coal-fired energy today will require significant investment in cleaner technologies during the 2020s to meet the compliance requirement that’s due to come into force in 2030.

The CPP, which was unveiled in August by the Environmental Protection Agency (EPA) calls for a 32% reduction in emissions of CO2 from power plants. It has prompted legal action from at least 15 states and looks set to become a significant bone of contention between Republicans and Democrats in the Senate this fall.

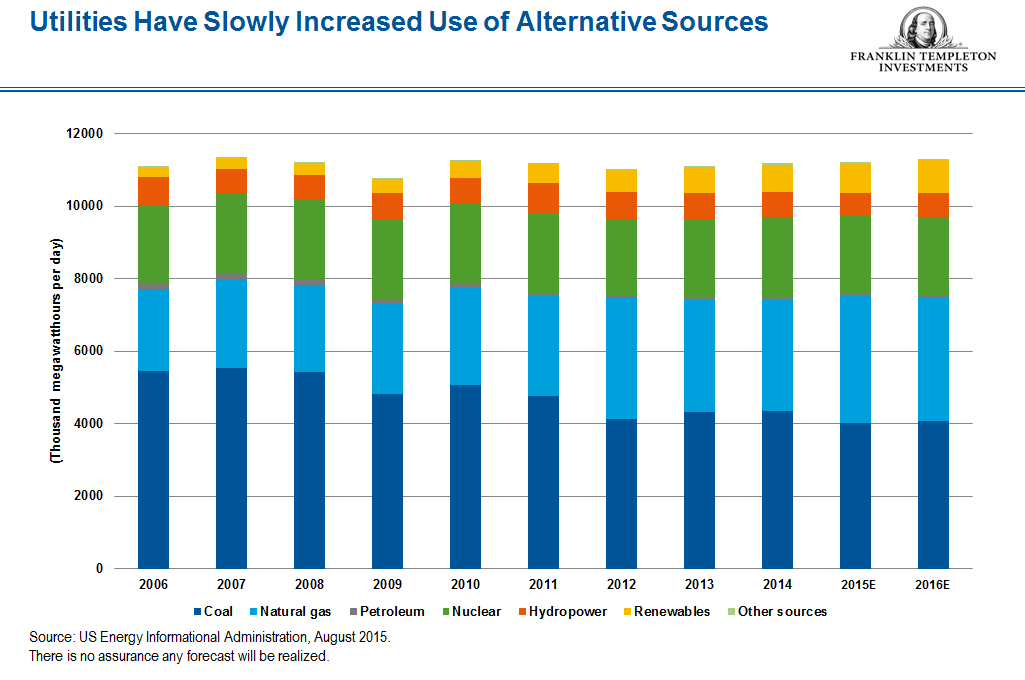

But many utilities, having seen the writing on the wall, have already made great inroads to reduce their carbon emissions; the call for cleaner sources of electricity is clearly not a new trend. It has been a major theme within the electric utilities industry over the past decade, as the industry has seen a shifting mix of power generation by fuel type, with greater emphasis on renewable sources and less reliance on coal.

This shift has occurred partly due to stricter EPA rules, but has intensified as states have implemented their own individual renewable portfolio standards (RPS). Meanwhile, the development of natural gas from shale gas has also lowered the cost of that fuel compared with other sources and has produced a growing percentage of gas-fired generation, mostly at the expense of coal-fired generation. The CPP would follow that trend, further pushing utilities toward integrating more renewables and natural gas into their generation mix, and requiring continued retirement of older, inefficient coal plants to remain compliant.

Digging for Opportunity

The CPP will likely influence our portfolio composition in much the same way increasingly strict emission standards have affected our investment decisions since the turn of the 21st century. Capital investment used to comply with environmental standards can be a strong driver of earnings growth for an electric utility, as the regulatory model is built around companies recouping the dollars they deploy into their businesses by passing the costs along to ratepayers. In contrast, rapidly rising levels of capital spending can also carry a major downside as they lead to unhappy customers facing higher bills to pay for these improvements. Our investment decisions will continue to focus on those utilities that appropriately balance their growth potential with the maintenance of healthy customer and regulatory relationships.

In general, we’ve found that the most forward-looking utilities already have started reducing emissions by using less coal-fired power and more sources of renewable energy. For the most part, utility company managers have been actively working with their state regulators and policymakers for many years on implementing energy policies that comply with anticipated future environmental restrictions. Many states today have RPS rules that feature incrementally higher targeted levels of renewables over time, and thus companies have been actively investing in wind and solar projects to meet those state RPS laws.

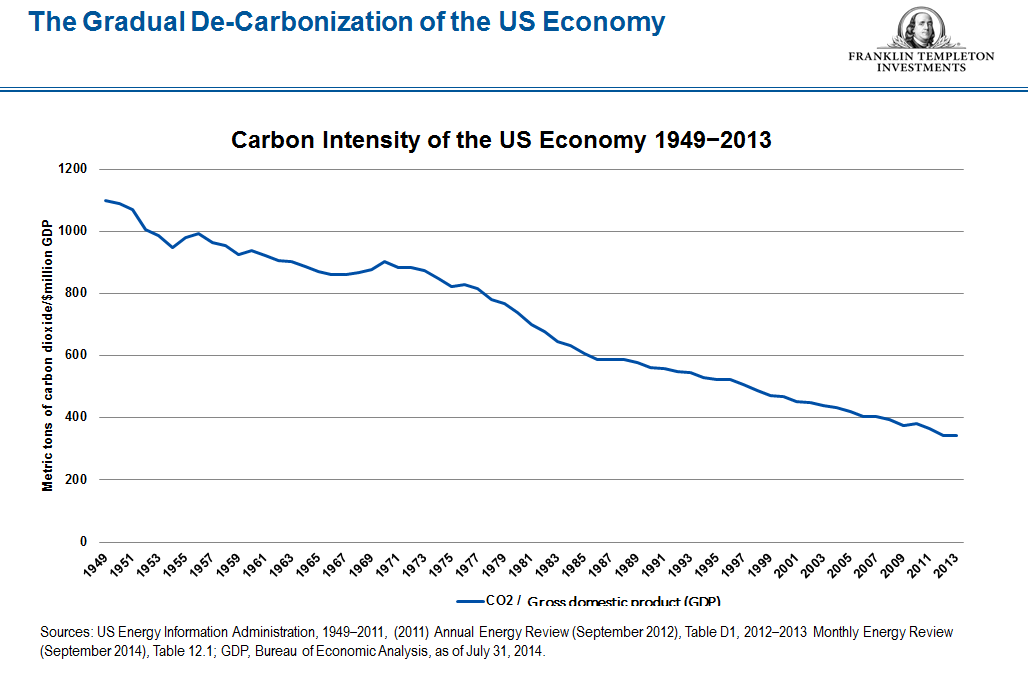

In our view, the industry as a whole has done an outstanding job at reducing the levels of hazardous emissions produced by its power plants. EPA rules have driven the pace of investment to meet the level of reductions that has been made, and this trend will continue as the industry takes on the carbon dioxide issue. The CPP, if it survives its legal battles, will ensure that all utility companies work toward reducing their carbon footprint. We favor those companies that manage their investment needs appropriately and effectively by working with and crafting appropriate implementation policies.

With demand growth for utility services essentially flat in the United States, it is difficult to identify opportunities on a purely organic basis. However, the infrastructure investment story is one that has played out over the past decade and, in our view, will likely continue to provide opportunities well into the 2020s. Not only is environmental compliance driving investment for electric utilities, but recent gas pipeline safety legislation has driven companies to invest more heavily in pipeline replacement programs to eliminate total exposure to piping made of cast iron and bare steel. Pacific Gas & Electric Corp.1 is an example of a utility that has witnessed a major transformation of its gas pipeline network over the past five years, in the aftermath of a tragic gas line explosion that killed eight people in a San Francisco suburb.

Effects of Potential (Interest) Rate Hike

We are also closely following US interest-rate trends, as utilities have historically faced a higher correlation to bond price movements than to general stock market changes. Utilities generally trade like bonds because they pay out relatively high levels of their income in the form of dividends. Any move higher in long-term bond yields should have a negative impact on the price of utilities stocks. Theoretically, however, changes in the short-term interest-rate benchmark, the federal funds rate, should not impact the price of utilities, unless there is a corresponding rise in the yield of long-dated bonds.

The utilities sector may also feel the sting of higher interest rates more than other sectors because its capital structure is balanced at about 50% debt and 50% equity, which indicates it employs slightly more leverage than some other industries. That said, utilities have their return on capital determined for them by their regulators, and thus their debt-cost recovery is generally passed directly through to customers.

Overall, we are positive on the fundamentals of utilities, believing that distribution payouts have the opportunity to grow over the next several years.2 With a current industry dividend yield of about 4%, we like the potential total return opportunity for the sector.3 In our view, utilities should also benefit versus other sectors if recent global economic worries continue to be a focus of investors, as this has historically been the case when investors seek what are perceived as less-risky assets.

John Kohli’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. To obtain a summary prospectus and/or prospectus, which contains this and other information, talk to your financial advisor, call us at (800) DIAL BEN®/342-5236 or visit franklintempleton.com. Please carefully read a prospectus before you invest or send money.

Hyperlink Disclaimer

Links can take you to third-party sites/media with information and services not reviewed or endorsed by us. We urge you to review the privacy, security, terms of use and other policies of each site you visit, as we have no control over and assume no responsibility or liability for them.

_______________________________________________________________

1 As of 6/30/2015, Pacific Gas & Electric Corp. represented 3.63% of total net assets of Franklin Utilities Fund. Holdings are subject to change without notice.

2 There is no assurance that any estimate or forecast will be realized.

3 Past performance is no guarantee of future results.

© Franklin Templeton Investments

© Franklin Templeton Investments