El Niño Update

Meteorologists have been calling for an El Niño event since last year. Current forecasts place the likelihood of an El Niño occurrence this winter at over 90%. Now, talk has turned from the likelihood of an El Niño to whether the abnormal weather pattern event will be super-sized or monster-sized. Water temperatures in the Pacific, one of the first signs of a looming El Niño, have measured much higher than normal. In fact, water temperatures have been on par with the most severe El Niño event from the past 30 years. As investors, we monitor larger climate events as severe weather can have an effect on most commodity markets.

This week, we will look at how an El Niño develops and its possible climate, economic and geopolitical effects on the global economy. As always, we will outline the potential investment implications of this event.

What is an El Niño?

Years ago, Peruvian fishermen noticed a periodic warming of the ocean temperature. The warming cycle seemed to occur around Christmas in certain years, so it came to be called “the Christ Child,” or El Niño in Spanish.

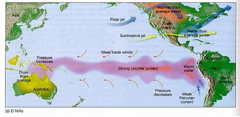

In general terms, an El Niño is an interruption of the ocean water and air-atmosphere in the Pacific Ocean. An El Niño starts as warm water near Indonesia rises to the surface of the Pacific. Weak easterly trade winds and strong counter-currents move warm water across the Pacific to the Pacific coast of South America. This ocean water movement also shifts air pressure, moving rain from Australia and Asia into the Americas. This unusually warm water along the Pacific coast of South America also increases water and air temperatures in Alaska and the northeastern United States.

The usual El Niño interval is between two and seven years and the warming period lasts nine months to two years. The warming trend causes a ripple effect throughout the world, resulting in a wide range of changes to global weather patterns.

The charts below show normal atmospheric conditions (top chart) and El Niño-induced global weather conditions (bottom chart). Under normal climate conditions, parts of the Americas experience relatively less precipitation and cool air and ocean temperatures. During El Niño years, those same areas experience warmer than normal ocean temperatures and more precipitation.

(Source: USC)

(Source: USC)

El Niño brings warmer temperatures to most of South America, the northern half of the United States and most of Europe. Cooler than normal temperatures are expected for the southern half of the United States, Australia and Asia.

Greater than normal amounts of precipitation is forecast for the southern half of the United States, most of South America and parts of central Africa. However, parts of the Americas, namely Mexico and Brazil, are more likely to experience droughts, although the majority of South America should experience increased precipitation. Less than normal amounts of precipitation is likely for Asia, Australia and southern Africa. Southeast Asia has historically been affected the most, with Indonesia and Australia especially vulnerable to droughts.

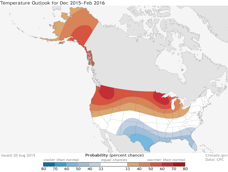

The charts below indicate the current domestic outlook for this winter (Dec 2015-Feb 2016). These forecasts place the likelihood of an El Niño occurrence at over 90%. The top chart shows the temperature outlook, while the bottom chart shows the precipitation outlook. The northern half of the country is likely to see warmer and drier than normal conditions, while the southern half is likely to see cooler and wetter than average conditions. California should benefit from the increased precipitation, although the threat of mudslides and storms also increases. El Niño years also usually see fewer hurricane developments.

(Source: Climate.gov)

Effects of El Niño

El Niño is associated with severe weather changes, so it is assumed that the climate consequences would be adverse. This assumption is not necessarily true. Although parts of the world may see the development of unfavorable weather, other parts may benefit. As the strength of El Niño varies, so will its effects on global climate and economic activity.

Many agriculture-dependent economies can be severely affected by a strong El Niño. Asia and Australia usually see droughts during El Niño years, which can be damaging to the local agriculture. Indonesia and the Philippines seem to be close to the epicenter of El Niño-induced droughts. The lack of rain caused by cooler ocean water can damage coffee, cocoa and palm oil yields.

In Southeast Asia, most of the effects of El Niño depend on its impact on the monsoons, which has been somewhat unpredictable. Most El Niños weaken the monsoons and Indian authorities have already indicated that they expect this year’s monsoon season to be weaker than average.

However, El Niño allows for various benefits to the eastern side of the Pacific. Plentiful rainfall in southern Brazil, central Argentina and Uruguay leads to better yields. Soybean and livestock supplies are likely to improve due to increased rainfall. At the same time, mineral exploration is likely to see work stoppages due to the rains.

Warmer winter temperatures in the northern U.S. as a result of El Niño mean lower heating costs across the northern United States. El Niño also brings fewer Atlantic hurricanes, but does not reduce the intensity of the hurricanes that do develop. This could help off-shore refiners and the insurance industry.

Although global temperatures generally rise during El Niño, Alaska seems especially susceptible. The warming jet stream melts more ice and snow, leading to higher ocean levels. Ocean levels around California could rise as much as 12 inches; given the current California drought, such storms would be welcome to replenish depleted reservoirs. Higher sea levels could also mean increased storm surges, leading to mud slides as seen in the San Francisco area during the 1997-98 El Niño.

Ramifications

Possible future El Niño effects have not been currently priced into the market. However, as we move further into Q3 and the intensity of El Niño becomes clearer, we would expect commodity markets to discount the climate effects.

In general, soft commodity prices rally between 10-40% during El Niño periods. Sugar, palm oil and coffee prices have risen the most during the last six El Niño events as their production is concentrated in areas mostly affected by droughts. The chart below shows the 20-year price chart for sugar. Sugar prices could spike as increasing rainfall in Brazil could lower yields. Tighter sugar supplies would pressure prices higher. However, sugar is also produced in Asia, where producers could benefit from higher prices while continuing to maintain volumes.

(Source: Bloomberg)

Palm oil production has already suffered due to recent dry spells in Indonesia and Malaysia, and may fall further if an El Niño develops. Palm oil prices have historically been highly affected by El Niño events and have the potential to be the most vulnerable commodity this year. The chart below shows the 20-year price chart of palm oil. Prices spiked during the 1997-98 El Niño and we would expect similar price action if El Niño materializes.

(Source: Bloomberg)

The chart below shows the 20-year price movement of coffee futures. The 1997-98 El Niño caused a steep spike in prices; however, this year producers are not expecting wild price swings.

(Source: Bloomberg)

Production of rice, the staple grain for over half the world’s population, has historically shifted between countries during an El Niño, but the total global production has been only modestly disrupted. For example, Indonesia’s rice imports will likely increase if El Niño strengthens. The chart below shows the 20-year rice futures. Rice prices were only modestly affected during the 1997-98 El Niño.

(Source: Bloomberg)

Increasing precipitation in the Americas would actually mean better corn and soybean yields, which could lower prices, especially after two years of record domestic corn yields. The chart below shows the corn futures.

(Source: Bloomberg)

Increasing grain volume is likely to benefit domestic producers, even in a lower price environment.

The milder weather in certain regions is also likely to decrease demand for natural gas for heating. Ample global supplies, warm end-of-summer weather and expectations of a mild winter have pressured natural gas prices to a 16-year low. The chart below shows the natural gas futures, which have suffered declines due to rising production.

(Source: Bloomberg)

Historically, base metal prices would have been affected as mining for copper and other metals would be disturbed by increasing precipitation in South America. However, no dramatic effect on industrial metals is expected this year given the current high global inventories. No price effect on precious metals is forecast, also due to high stockpiles.

As we mentioned, the commodity markets have not yet discounted the El Niño effect. In general, the impact on commodities can take 12 months to occur. However, commodity prices can move swiftly once the stronger El Niño effects materialize. We will continue to monitor this development closely, but we will have a better reading of its magnitude in the third quarter of this year.

Commodity production disruption will likely lead to a mild uptick in food inflation, especially in Asia. According to an IMF study, small rises in inflation (less than 1%) could be attributed to El Niño. Of the countries that are likely to see rising food inflation, Japan, India and Indonesia bear watching. Rising inflation would be welcomed in Japan; however, India and Indonesia have long struggled to control high inflation.

El Niño also affects global economic activity, but only in the short term. In general, Australia, Chile, Indonesia, India, Japan, New Zealand and South Africa have seen short-term declines in economic activity. On the other hand, historically, an El Niño environment has led to a short-term uptick in economic growth in the U.S. and Europe.

Kaisa Stucke

September 28, 2015

This report was prepared by Kaisa Stucke of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

|

© Confluence Investment Management