Reader reactions to last month’s Macro Perspectives suggest that my thesis of a swelling rather than ebbing global savings glut, due mainly to demographics and the emerging market malaise, remains controversial. This is great, because it means we have a trade: Those of you who think the savings glut will be history soon should position for a significant increase in real rates over time and a long, protracted grind lower in risk assets, while I should position for rates remaining relatively low and risk assets (in developed markets) staying supported, in line with PIMCO’s secular New Neutral thesis.

But, tempting as it is, I won’t belabor the savings glut further today. Rather, this is the time to zoom in on another pillar of my “three gluts” thesis – the global money glut. Ever since the 2008–2009 financial crisis, central banks around the world have bravely battled the secular headwinds to growth and inflation emanating from global excess savings with the help of ZIRP (zero interest rate policy), NIRP (negative interest rate policy), and QE (quantitative easing). So there is nothing new about the money glut. However, there are two good reasons for focusing on it right now:

- First, it looks increasingly likely that each of the world’s four major central banks will adjust its monetary policy stance before year-end: The Federal Reserve on the whole seems likely to hike rates for the first time in more than nine years this December, while the European Central Bank (ECB), the Bank of Japan (BOJ) and the People’s Bank of China (PBOC) look likely to ease policy further. This highly unusual constellation requires some discussion.

- Second, and even more importantly, many market participants harbor increasing doubts that monetary policy can still be effective in propping up asset markets and thus economies further, and worry that we may be entering a phase of not only diminishing positive, but even potentially negative, returns from monetary easing. To those of us who, like me, believe that without past central bank actions we would be in a deep slump comparable only to the Great Depression and that the global economy continues to require ongoing, and in many places even more, stimulus in the face of mostly dysfunctional fiscal and structural policies, this popular thesis of “monetary impotency” is deeply disconcerting. To be sure, the thesis should be taken seriously, but there are compelling arguments against it. I continue to believe that it’s a money loser to try to fight the (global) central bank – at least as long as its board members Janet Yellen, Mario Draghi, Haruhiko Kuroda et al. are determined to do whatever it takes.

A quick history of extraordinary central bank activity

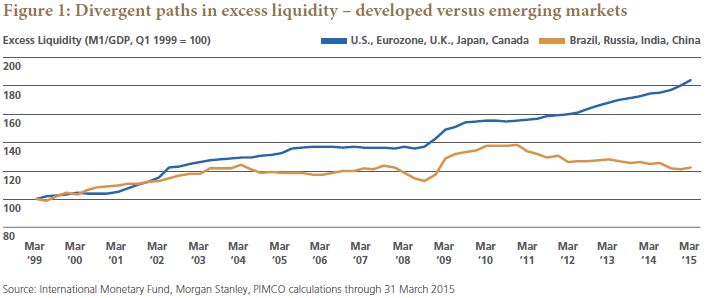

Let’s take a step back first, and briefly recap the enormous contribution monetary policy has made ever since the “Minsky Moment” (which PIMCO’s former chief economist, Paul McCulley, had predicted so clairvoyantly) arrived in 2008. Put very simply, the story can be summarized in Figure 1: Through massive unconventional monetary easing in various forms, the five central banks of the U.S., the Euro area, Japan, the U.K. and Canada (along with others of course) managed to keep enough money sloshing around in the economy to prop up economies and asset markets. For these five regions, the ratio of the monetary aggregate M1 (cash and sight deposits held by non-banks) to nominal GDP kept rising on its long-term trend path despite the massive deleveraging in the private sector following the crisis. In other words, central banks managed (through a much, much larger expansion in the monetary base) to keep money in circulation growing, and at a faster rate than nominal GDP, which helped to prop up asset markets and fed back into the real economy.

Now contrast this with the excess liquidity in the four largest emerging market (EM) economies, China, Russia, India and Brazil. Initially, during and soon after the financial crisis, excess liquidity in EM surged even more than in developed markets (DM) as ZIRP and QE in the DM economies pushed capital flows into EM, and central banks there eased monetary policy to stem excessive exchange rate appreciation. But when this surge in liquidity pushed up inflation in EM and growth recovered, EM central banks tightened policy in 2010–2011, which led to a long decline in excess liquidity that lasted until earlier this year. If you believe that asset markets are influenced by excess liquidity, then it shouldn’t come as a surprise that EM assets have underperformed DM assets in recent years.

So three cheers to the Fed et al. for keeping things humming along despite massive headwinds from a balance sheet recession and for preventing the Great Depression II. Sure, it would have been desirable for fiscal and structural policies to be more supportive. Central banks would then have had to take fewer risks with potential bubbles, bloated balance sheets and potential fiscal dominance. But that option simply was not available given the sad state of politics in many major countries.

And sadly, it ain’t over yet. The best we can say of fiscal policy in the U.S., Europe and Japan right now is that it is not damaging growth anymore (or at least less than it used to). And in many EM economies, fiscal and general economic policies are a source of uncertainty and volatility rather than stability.

The near future of monetary policy

So it’s all eyes on the global central banks again as the sad travails of many EM economies are an increasing drag on global growth and a driver of deflationary pressures through the exchange rate and commodity channels. Will the major central banks react?

I think so, even though the story is complicated by the Fed’s seemingly strong desire to get off the zero bound this year. But even there, don’t despair. By not tightening in September, the Fed acknowledged it is not blind to global developments, as these feed back into the U.S. growth and inflation outlook through weaker exports (and boy, have they been weak recently!), lower capital expenditures in the energy sector and tighter financial conditions due to a stronger dollar and soggy risk assets. And even if financial conditions ease between now and December and the Fed lifts off zero (our base case at this stage), it will probably be the most dovish rate hike ever, with plenty of assurances that the path will be very, very gradual.

By contrast, the other big players – the ECB, the BOJ and the PBOC – look set to ease policy further in the current quarter. The PBOC will probably be the first out of the blocks with another rate cut and also further reductions in banks’ required reserve ratios. However, surprises from the BOJ or the ECB as early as at their October policy meetings cannot be excluded. Both look set to upsize and/or extend their QE programs, and cuts in their deposit rates (more deeply negative at the ECB, down to zero at the BOJ) are well possible. The motivation would be clear: push inflation expectations and thus hopefully actual inflation closer to the target that has remained elusive so far due to global deflationary forces emanating from EM.

Will monetary easing continue to be effective?

So much for what central banks are likely to do: plenty of action ahead in the next few months. But will it work? Many believe, or fear, that it won’t anymore – as I said earlier, this is a deeply disconcerting thought that has to be taken seriously.

I see three main arguments being advanced for the monetary impotency thesis. First, the poor performance of risk assets and the renewed decline of market-implied inflation compensation in recent months are often viewed as signs that easy money has lost its mojo. Second, with risk assets such as equities and credit less “cheap” now than when central banks engaged in their various rounds of QE in the past, easing will get less “bang for the buck” this time as it will be more difficult to push asset prices higher still. Third, but not least, my colleague Qi Wang has proposed the thesis that monetary easing in current account surplus (or “producer”) economies such as the Euro area and China may be globally deflationary, in contrast to easing in deficit (or “consumer”) economies such as the U.S. or U.K.

Regarding the first argument, I doubt that soggy risk markets and inflation expectations in recent months tell us anything about the effectiveness, or lack thereof, of expansionary monetary policies. Rather, I view it as a consequence of (1) uncertainty about China’s economic outlook and its policymakers’ intentions regarding the exchange rate and (2) uncertainty about the Fed’s first rate hike and fears of related market turbulence. As Tony Crescenzi argues in the latest Global Central Bank Focus , the Fed’s “phantom rate hike” has led to a chain reaction in financial asset prices over the course of this year. So if anything, monetary policy seems to be still very effective in influencing markets. If fears about Fed tightening depress asset prices, why shouldn’t further rate easing help boost asset prices?

The second argument – that asset prices are less cheap and therefore more difficult to push higher still through monetary policy – sounds intuitive. I buy the argument of diminishing returns to QE via the asset market channel. Note, however, that both equities and credit have recently “cheapened” quite a lot. Also, I find it hard to believe that asset prices would go down if the ECB or the BOJ announced a significant increase of their respective programs.

This leaves us with the third argument: “Producer” QE may be deflationary, while “consumer” QE is reflationary. This is an interesting thesis that requires more reflection than the remaining space for this month’s column permits. Here’s my preliminary assessment: Yes, everything else unchanged, QE in a country that is a bigger consumer and importer will benefit the world (via higher exports to that country) more than QE in a country that is a relatively smaller consumer and larger exporter. However, there should be two offsets, and I’m not sure we can say a priori what the net global effect will be. First, if the central bank of a producer economy like, say, the Euro area eases policy, the currency would typically depreciate. But the resulting currency appreciation of a consumer economy like, say, the U.S. would benefit its consumers disproportionally as import price deflation would ease further. Moreover, lower inflation in the U.S. would allow the Fed to pursue a more expansionary (or less restrictive) monetary policy, which would help lift the boats in the U.S. and globally. But, again, I’ll have to think more about this argument.

Bottom line: Given global lowflation pressures emanating from EM and commodities, the central-bank-fueled money glut is likely to increase further before year-end as ECB, BOJ and PBOC easing should outweigh a potential “dovish hike” by the Fed. Thus the “AAA” liquidity cycle – where liquidity is ample, abundant and augmenting – continues, at least in DM. And while there are reasons to expect less bang for each QE buck than in previous QE episodes, the returns should still be positive. Actually, less bang for the buck is an argument for doing more rather than less.