In perhaps a massive understatement, volatility in the global financial markets picked up during the third quarter. Equity, fixed-income, and commodity markets all around the world were disrupted to varying degrees. Of course, the renewed volatility unsettled investors, and bears roared loudly while bulls pulled in their horns. To paraphrase Clement Clarke Moore, visions of 2008 danced in their heads.

The key question for investors is whether the secular bull market remains intact or whether a bear market and recession are looming. We think the secular bull market remains intact. Fear continues to overwhelm greed in most segments of the financial markets.

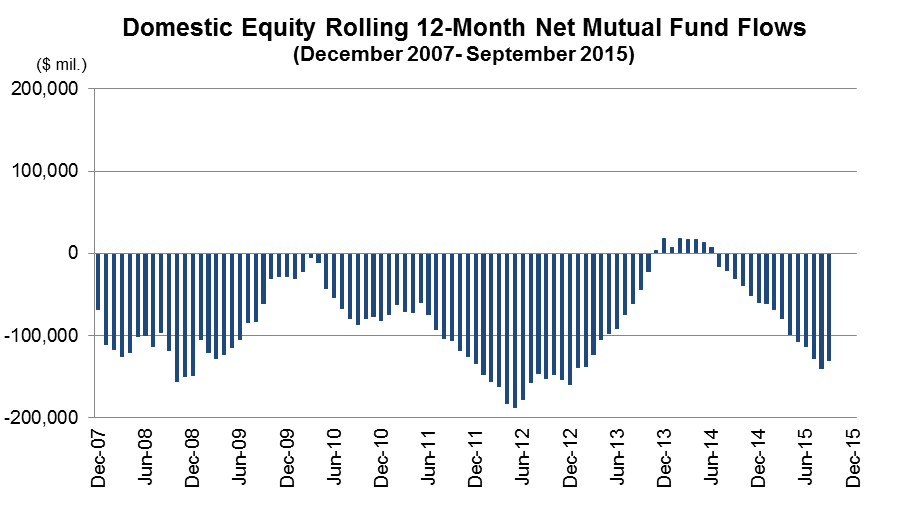

Waiting for an entry point?

For the past year or more, many investors suggested that fundamentals were improving, but that the equity market was overvalued at current levels and investors should use pullbacks in the market as entry points to invest. Investors have gotten their pullback, but it doesn’t look as though they are using the opportunity to buy equities. Rather, it appears that investors were too scared to invest as the stock market rose and are too scared to invest as the stock market corrects. One might say that one is waiting for the market to bottom; however, history suggests that the stock market bottoms at the point of maximum fear and not at a perceived point of maximum opportunity.

Whether one looks at ETF flows, mutual fund flows, Wall Street strategist recommended asset allocations, institutional portfolio allocations, or hedge fund positioning, the simple fact remains that investors are generally scared of equities. See Chart 1.

Source: Richard Bernstein Advisors, ICI

Why volatility now?

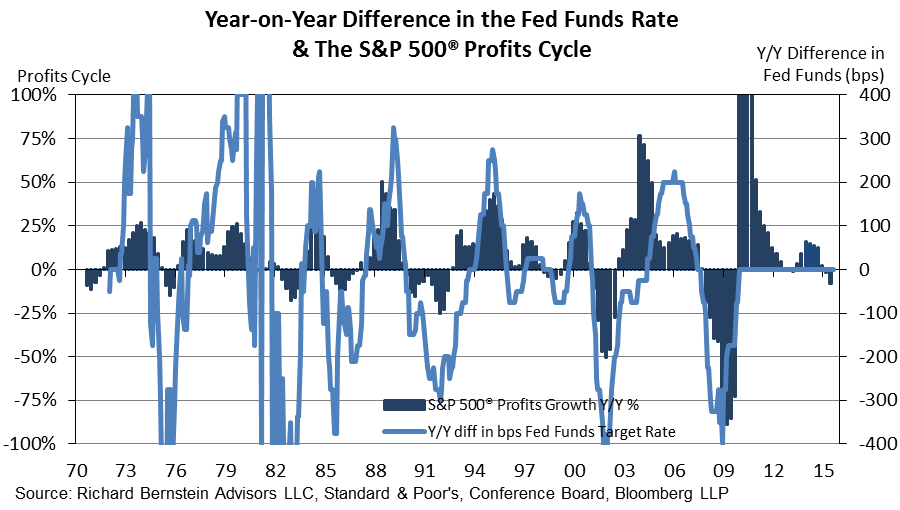

We pointed out last month that perhaps the main reason for the markets’ volatility is the odd combination of the Fed hiking interest rates when the profits cycle was decelerating. Chart 2 shows the historical positive correlation between changes in the Fed Funds rate and the profits cycle. Historically, profits were revving up when the Fed started increasing rates, and the positive of accelerating earnings would overwhelm the incremental negative of the Fed raising interest rates. However, this cycle appears unique in that the Fed is “threatening” to raise interest rates when the US is in a profits recession. Rather than a traditional offsetting relationship at this early point of the tightening cycle, the near-term interest rate outlook and the near-term profits outlook are both negative.

Is the secular bull market intact?

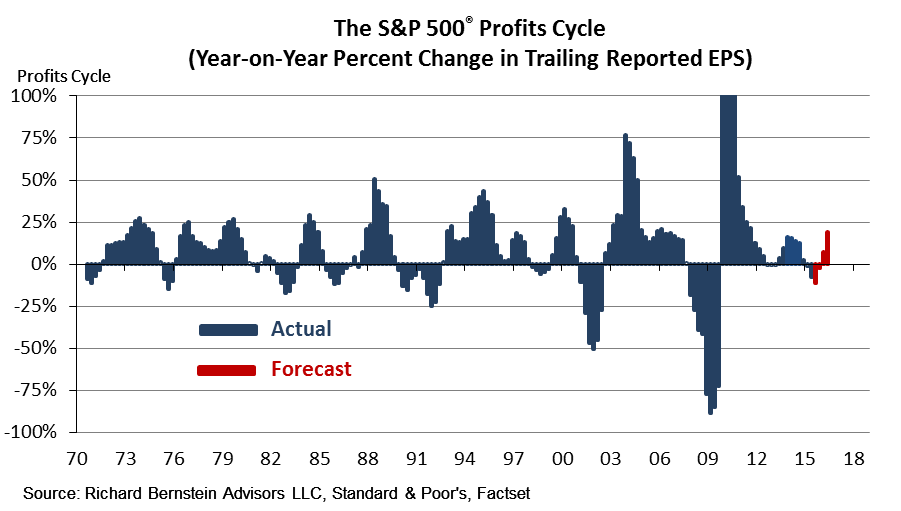

Our proprietary research suggests that the profits cycle is likely to trough either in the third or fourth quarter depending on the level of write-offs toward year-end (See Chart 3). That would imply that the relationship between Fed Funds and the profits cycle might return to a more normal one and, if that is the case, we think the equity market can continue advancing as it would during a mid/late-cycle environment.

Is the sky really falling?

Volatility is always unsettling for investors. However, one has to assess whether the volatility is forecasting an end to the profits, economic, and market cycles or whether the volatility is a correction within the context of a longer bull market. Our corporate motto is “Uncertainty = Opportunity®” and our portfolios are positioned accordingly.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results. Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

About Richard Bernstein Advisors

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $3.1 billion collectively under management and advisement as of September 30, 2015. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund, the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and the Eaton Vance Richard Bernstein Market Opportunities Strategy Fund and also offers income and unique theme‐oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial Renaissance® ETF and the First Trust RBA Quality Income ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS, Merrill Lynch, Morgan Stanley Smith Barney and on select RIA platforms. RBA's investment insights as well as further information about the firm and products can be found at www.RBAdvisors.com.

© Copyright 2015 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.