KEY TAKEAWAYS

The approaching debt ceiling is a significant contributor to the state of T-bill yields.

Rather than an alarm signal, 0% yields are a reflection of current Fed policy and supply issues stemming from the Treasury’s extraordinary measures to delay reaching the debt ceiling.

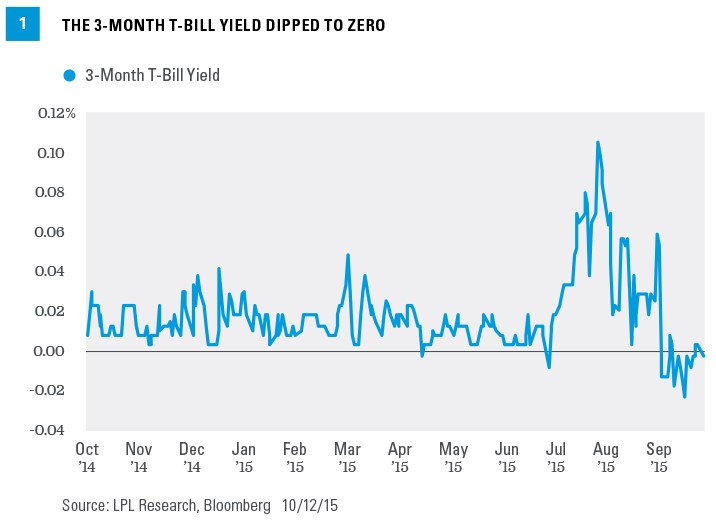

The Treasury issued new three-month Treasury bills (T-bills) at 0% yield at auction last week and is on pace to do so again on October 13, 2015. Zero percent T-bill yields, or even lower, are not new, but 0% prevailing at an auction is unusual and made media headlines. After trading in an extremely narrow range for most of the past year, the three-month T-bill yield increased in August, in large part due to the prospects of a Federal Reserve (Fed) rate increase, but has since turned lower [Figure 1]. Rather than an alarm signal, 0% yields are a reflection of current Fed policy and supply issues stemming from the Treasury’s extraordinary measures to delay reaching the debt ceiling.

A supply shortage has once again impacted very short-term Treasury yields. The approaching debt ceiling is a significant contributor to the state of T-bill yields. The Treasury has operated under “extraordinary measures,” one of which has been the reduction of T-bill issuance in favor of longer maturity debt. This enables the Treasury to maintain normal issuance of longer maturity notes and bonds, from 2 years to 30 years.

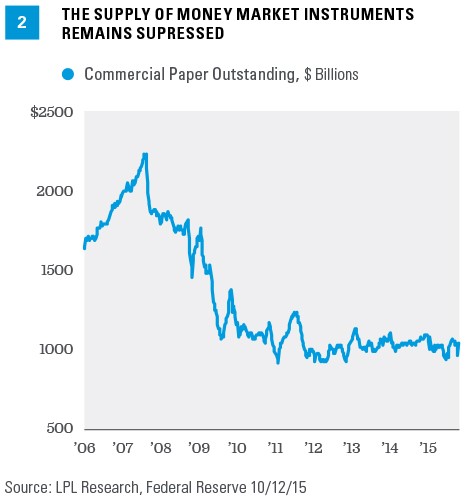

T-bill supply has been squeezed for several years, however. Since the end of the financial crisis, the Treasury has sought to take advantage of lower interest rates by issuing longer-term securities. The average maturity of outstanding marketable Treasury debt increased from four years in late 2008 to just under six years (according to Treasury data) as of June 2015. Furthermore, the reduction in commercial paper outstanding, the corporate version of a T-bill, also limited the availability of high-quality, very short-term debt obligations [Figure 2].

Of course the Fed is also largely responsible for the state of yields. Despite the recent changes in the three-month T-bill yield, the range continues to be very narrow (as Figure 1 also shows) due to the Fed’s maintenance of near 0% overnight lending rates. Any meaningful change to T-bill yields, or money market instruments in general, will therefore likely be limited until the Fed begins to raise interest rates, and the low-yield, low-return environment will likely persist.

DEBT LIMIT Yield Bump

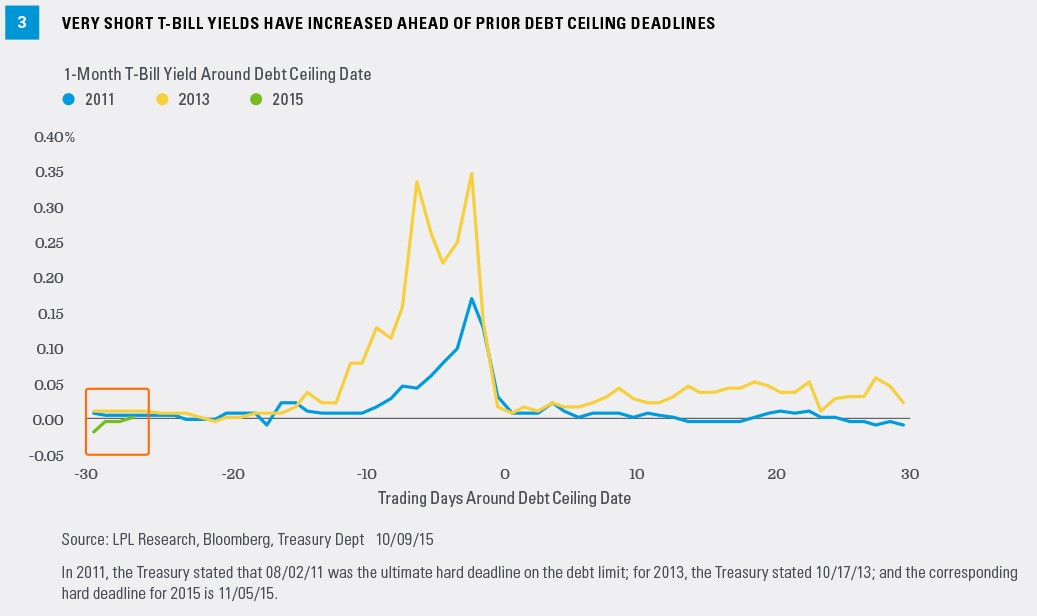

Yields may ultimately get a boost as the debt ceiling deadline draws near but not likely enough to change investment appeal for many investors. Treasury Secretary Jack Lew recently stated that November 5, 2015, is the drop dead date (i.e., the date at which time extraordinary measures will have been exhausted) to approve an increase in the debt limit. In the past, very short T-bill yields have increased as the U.S. government flirted with a potential disruption by waiting until the last minute to approve a debt limit increase [Figure 3].

We expect lawmakers to agree to raise the debt ceiling well ahead of any potential delay to Treasury interest payments. The potential disruption, however remote, has historically been limited and the likely change in yields in anticipation of the current episode is also likely limited. The uncertainty around the debt ceiling, however, is another factor that may provide modest support to high-quality bonds despite expensive valuations.

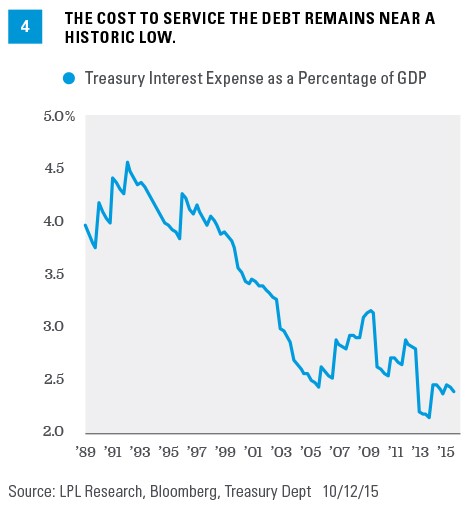

While the overall amount of Treasury debt outstanding remains high and continues to grow, the cost to service Treasury debt remains near a historic low [Figure 4]. Context is important. The low cost to service the debt is reflective of a high-quality bond issuer, 0% yields, and a possible debt ceiling showdown in Washington.

Like the amount of Treasury debt, context is also important regarding 0% T-bill yields. Rather than an alarm signal, 0% yields are a reflection of current Fed policy and supply issues stemming from the Treasury’s extraordinary measures to delay reaching the debt ceiling.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Commercial paper is a short-term unsecured promissory note issued by a finance company or a relatively large industrial firm. The notes are generally sold at a discount from face value with maturities ranging from 30 to 270 days. Although the large denominations ($25,000 minimum) of these notes usually keep individual investors out of this market, the notes are popular investments for money market mutual funds. Used interchangeably with the term paper.

The money supply is an economic term for the total amount of currency and other liquid assets available in an economy at a point in time. There are several ways to define this number. M1 includes physical money such as coins and currency, checking accounts (demand deposits), and Negotiable Order of Withdrawal (NOW) accounts. M2 includes all of M1, plus time-related deposits, savings deposits, and non-institutional money-market funds.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 5247 1015 | Tracking #1-429865 (Exp. 10/16)