On October 6, trade negotiators announced a final agreement for the Trans-Pacific Partnership (TPP), a multilateral trade deal between 12 Pacific Rim nations in both the eastern and western hemispheres.

In this report, we will begin by discussing the nations involved. We will examine some of the details of the treaty. An analysis of the geopolitics will follow along with a look at specific political factors surrounding the treaty. As always, we will conclude with potential market ramifications.

The TPP Nations

The TPP began as a 2005 pact between four nations, Brunei, Chile, New Zealand and Singapore. In 2008, the U.S., Australia, Peru and Vietnam expressed interest in joining the original group. Malaysia entered negotiations to join in 2010, Mexico and Canada in 2012, and Japan in 2013. South Korea has also been in talks to join.

(Source: Wikipedia)

Conspicuous in its absence, China is not in the pact, although leaders have expressed interest in China joining at some later date. This is an important issue which will be discussed at greater length below. Taiwan, however, has expressed interest in the agreement. Due to the uncertainty surrounding Taiwan’s sovereignty, it is doubtful that it would join without China’s membership. Since the governments of mainland China and Taiwan officially hold that each are the legitimate representative of China, adding Taiwan to the pact would likely bring a vicious response from the Xi administration.

Some of the Details

Although it is beyond the scope of this report to examine all the details of the TPP, here are some of the key points:

- The TPP is big, covering 27% of global GDP.1 The U.S. exported $600 bn of manufactured goods to the TPP nations last year. It is currently the largest regional trade agreement in history.

- There will be major tariff reductions for American exporters. Currently, U.S. firms face tariffs as high as 55% on wine, 50% on motorcycles, 35% on plywood, 30% on tractors and 20% on cosmetics. Those will all go to zero in the coming years. Overall, 18,000 tariffs will be eliminated by the TPP. All tariffs against U.S. manufactured goods will be eliminated by the deal and nearly all on agricultural products.

- Since the U.S. is generally a free-trading nation, it has fewer barriers to trade. Currently, the average American tariff is less than half of the other members of TPP. However, some 6,500 American tariffs will be eliminated; automobiles will get a 25-year grace period.

- The trade deal doesn’t end all trade restrictions. Japan will still have some degree of protection for rice, although U.S. quotas will increase by 33%. Canada will relax quotas on dairy. On the other hand, the U.S. sugar lobby managed to mostly protect its closed American market.

- Given that tariffs have been falling since the U.S. fostered the General Agreement on Tariffs and Trade (GATT) program after WWII, the focus of much of the negotiations was on non-tariff barriers. Primary concerns included protection of intellectual property and regulations designed to protect the market share of domestic producers. The pharmaceutical, media and tobacco industries will be closely parsing the agreement and will likely publicly protest the deal.

The Geopolitics

The best insight into the geopolitics of the TPP is that China isn’t part of the deal. At first glance, this omission appears illogical. China is the world’s second largest economy and clearly an important customer and supplier to the Pacific Rim. For example, the World Bank reports that in 2014 50.7% of East Asia’s capital goods exports were absorbed by China and 48.4% of China’s capital goods exports went to the East Asia region. For North America, 44.1% of capital goods exports were sent to China and 35.5% of North American capital goods imports came from China.

The point of the TPP is to create a U.S.-led trading block that will set the rules of the road for most Pacific Rim trade. Although we don’t expect China to immediately join, if the treaty is successful, look for the U.S. to eventually invite China to enter the program. If it does, China will make the trading block formidable but will do so under U.S. rules.

China sees the TPP as a form of economic encirclement, which is probably a reasonable position to take. So, how will China react? We suspect, at least initially, China will try to reduce the impact of the TPP by encouraging more bilateral trade with the Pacific Rim, including members of the TPP. By increasing trade with TPP members, the economic effects of joining the pact are less important. In addition, China has embarked on the “Silk Road Initiative,” an attempt to build a land and sea bridge from Asia to Europe, and has also founded the Asian Investment and Infrastructure Bank as a way to foster dependence on China’s economy.2

Although this strategy will reduce the chances of isolating China’s economy, it won’t weaken the reasons why nations wanted to join the TPP in the first place. China’s rapid economic growth has raised concerns about its emerging geopolitical power. To a great extent, nations wanted to create the TPP to ensure the U.S. would remain involved in Asia. Asian nations, in particular, want strong relations with China; China’s economy is absorbing regional exports making the country important to their growth. At the same time, they fear Chinese belligerence and want the U.S. to act as a counterbalance to China’s rising geopolitical heft.

In addition to the TPP, the U.S. is fostering Japan’s foreign policy normalization, which can be observed by PM Abe’s recent passage of new rules for military engagement. The U.S. needs a militarily active Japan to help counterbalance China. In addition, we note that the Philippines, which pressed the U.S. to leave American bases on its soil in the early 1990s, are considering inviting the U.S. military to return. In effect, the nations in the region want to benefit from China’s economic growth but want the U.S. to act as a check on China’s growing projection of power.

We note that there is a similar agreement being negotiated with Europe, called the Trans-Atlantic Trade and Investment Partnership (TTIP). Although negotiations continue, it doesn’t appear that completing the deal on the TPP will spur European and U.S. negotiators to reach a deal soon. If both treaties are passed, it would solidify the U.S. as the center of the trading world. The U.S. would be the unifying nation in both regional pacts and, coupled with the dollar remaining as the reserve currency, would essentially mean Washington will be key in global trade even if the U.S. share of world growth declines.

The Politics

Last week, hundreds of thousands marched in Germany against the TTIP. In the U.S., both the leading presidential candidates for the Democratic Party have come out against TPP. Although President Obama has “fast-track” authority, meaning that trade bills can neither be filibustered nor amended, there is significant opposition to TPP and its passage is not guaranteed.

All trade deals, to some extent, interfere with someone’s sovereignty. By establishing international rules of trade, domestic actors cannot take steps to interfere with trade. It is perfectly normal for citizens to fear loss of control over such trade agreements, fearing the lack of democratic influence on trade and the economy.

However, the opposition to TPP and TTIP goes beyond just the usual fear of sovereignty issues. Since 1980, the favored economic policies have been deregulation and globalization. The former allows for the rapid introduction of new technology and persistent economic disruption. The latter allows companies to source production in the most cost-efficient areas and sell goods and services across borders. For those who can successfully manipulate technology and operate in a global economic environment, the past 35 years have been a blessing. For those who cannot achieve these requirements, it has been a curse.

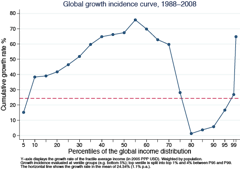

(Source: Milanovic and Lakner, CEPR, 2014)

This chart shows the real change in incomes from 1988 to 2008 for the world. Note that growth has been relatively robust for income deciles of 10% to 70%. Growth has been negative for the levels of 75% to 98%. This chart shows the power of globalization. It has been a major force in lifting global real incomes for much of the world, but for the developed world working class, it has been a difficult period. In a sense, globalization has generated a massive income transfer from the working classes of the developed world to those of the developing world. The very upper income levels in the developed world have also benefited from the policies of deregulation and globalization.

There has been a populist surge across Europe and in the U.S. Although often cloaked in terms like “liberal” and “conservative,” the real political sides are establishment versus populist. It appears that this divide is driven by the winners and losers from globalization and deregulation. As we detailed in our report on the 2016 elections,3 those who have not benefited from deregulation and globalization are rebelling; the fact that outsider candidates are surging shows how potent this issue has become.

Opposing trade agreements and immigration are part of the populist message. The establishment is very powerful. It represents the current national leadership in government, academia and business, and controls enormous economic resources. The populists are divided; the left and right wings don’t agree on how best to improve their economic conditions. However, both sides of the populist divide are anti-trade, and so the TPP may struggle to become law. The TTIP may not have a chance due to European opposition.

Ramifications

Although monetary policy gets the credit for ending the 1970s inflation crisis, in fact, we view it as a bit player. The real heroes were deregulation and globalization, which changed the shape of the aggregate demand curve. After the economy was deregulated and globalized, inflation steadily declined as the economy became more cost-efficient. However, the opportunity cost was increasing income inequality in the developed world.

If the TPP fails to pass Congress, it may be the first stage in undermining the policies that have led to low inflation. We would not expect inflation to become an immediate problem. History suggests it takes time for reregulation and deglobalization to undermine cost-efficiency. However, over time, perhaps a decade or so, pulling back from trade and using regulation to diminish creative destruction will put “sand in the gears of commerce” and lead to higher inflation.

On the other hand, if TPP does pass, it would suggest the establishment remains in control and inflation will remain low. This outcome is most likely, but given how fluid the political situation is, we will be monitoring developments closely.

Bill O’Grady

October 19, 2015

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

|

1 Purchasing power parity basis, international dollars, IMF

2 See WGR, 4/20/2015, The AIIB.

3 See WGRs: 3/31/2014, 2016 (Part 1, The Economic Issue); 4/14/2014, 2016 (Part 2, The Political Situation); and 4/21/2014, 2016 (Part 3, The Election Situation).

© Confluence Investment Management