Global Economic Perspective: October

US Federal Reserve Continues to Wrestle with Rate-Hike Decision

Optimists regarding the US economy received somewhat of a jolt when the latest nonfarm payrolls report showed a sharp downturn in job growth during September, as well as downward revisions to figures for the previous two months. The outsized monthly gains in nonfarm payrolls seen in 2014, when they averaged 260,000, have slowed to average gains of 198,000 in 2015. Snippets of more positive data were buried in the Bureau of Labor Statistics report, such as the broader U-6 measure of unemployment,1 which fell to 10.0% in September from 10.3% in August. In addition, the strong jobs gains of the past mean the economy is required to create “only” about 100,000 new jobs per month to keep up with the population rate, and the headline unemployment rate held steady at 5.1%, which is well down from 5.9% a year ago. In a nutshell, as the United States edges toward full employment, slower job growth was to be expected.

Leaving short-term international concerns aside, we still believe a Federal Reserve (Fed) move will depend on continued signs of domestic labor market tightening and on inflation trends. With fewer jobs needed to bring the unemployment rate even lower than it is today, with US consumers still spending, and with headline inflation set to rise in the short term as the base effect of the steep drop in oil prices in the second half of 2014 fades, we still believe there is a window of opportunity for the Fed to begin raising rates soon.

It is possible to find legitimate reasons in the United States as well as abroad for the Fed’s decision to stay its hand. Part of the positive trend in the headline unemployment rate is due to Americans who are no longer counted in job statistics, while the labor force participation rate declined to 62.4% in September, its lowest rate in 38 years. Additionally, the relatively disappointing nonfarm payroll numbers came on top of a decline in the Institute for Supply Management’s (ISM’s) index of national factory activity to 50.2 in September from 51.1 the month before, suggesting that manufacturing activity is barely expanding.

In contrast, though it fell back a little from the prior month’s reading, the ISM survey of the service sector still came in at 56.9 in September, well above the 50 dividing line between expansion and contraction, pointing to continued buoyant domestic demand in the United States. The health of the US consumer is further underlined by data for personal spending, a measure of how much Americans paid for everything from health care to home appliances, which advanced at a month-on-month rate of 0.4% in August. Consumer spending was the main support in the United States’ strong growth in the second quarter, when gross domestic product (GDP) rose at a 3.9% annual rate, and a number of indicators—such as healthy car and new-home sales—have continued to point to the robust health of the US consumer in the third quarter.

All eyes are now focused on the corporate earnings season, with a number of observers fearful that while cost-cutting and productivity gains for much of corporate America have been boosting profitability for some time, top-line revenues are declining, at least for energy-related companies (which have been hit by weak commodity prices) and for exporters (hit by weakening growth in emerging markets and a strengthening US dollar). Prospects for US exporters have certainly dimmed, with statistics showing that the US trade deficit jumped sharply in August due to a drop in the export of goods to their lowest level since June 2011 and a rise in imports.

A faltering manufacturing and export sector on the one hand, and continued expansion of services thanks to strong US consumer spending on the other, offers a contrasting vision of prospects for the US economy, and GDP growth for the third quarter is set to be markedly lower than in the second. But since consumer spending accounts for about 70% of US GDP, we believe the US economy should be able to withstand global headwinds.

At the same time, gathering clouds in the global economy, plus signs of continued slack in the jobs market and low inflation, complicate the Fed’s efforts to normalize monetary policy by moving base rates up from close to zero, where they have been stuck since December 2008. The Fed passed on its chance to do so at the conclusion of its policy-making committee in mid-September. In comments after the meeting, Fed Chair Janet Yellen arguably fed confusion among market participants about the Fed’s intentions by dwelling on the global economic and financial developments that could damage US growth and inflation. Since then, however, Fed officials have tried to be more upbeat and opined that the slowdown in China would have only a small or fleeting impact on the US recovery. We likewise continue to believe the US economy should be well able to withstand a modest hike in rates, and we remain in step with a majority of Fed policymakers who, as the minutes from the September Fed meeting revealed, still believe it would be appropriate to raise rates by the end of this year.

Emerging Markets: Confidence Needed

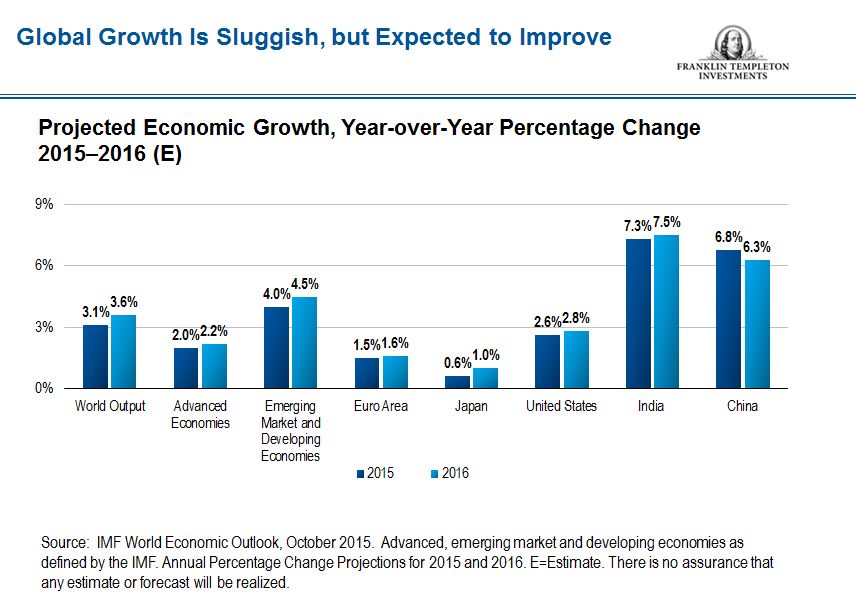

Prospects for global markets have taken a downturn in recent weeks. In September, the Organisation for Economic Cooperation and Development (OECD) cut its 2015 forecast for global growth to 3% from a previous forecast of 3.1% and its 2016 prediction from 3.8% to 3.6%. In early October, the International Monetary Fund (IMF) also lowered its forecast for global growth to 3.1% this year (down from 3.4% in 2014) and 3.6% in 2016.2

Both the OECD and the IMF pointed to the slowdown in emerging markets. Investors also continue to question prospects for emerging markets and have been removing money from these markets at a steady clip amid falling commodity prices, China’s slowdown and uncertainty over US interest rates. As a result, some emerging-market currencies had slid to their lowest levels in 16 years by the end of September. The extent to which emerging markets are out of favor can be gauged by a forecast from the Institute of International Finance that this year they face net capital outflows (of the order of US$540 billion) for the first time since 1988.

Although the late-September decision by the Fed to keep rates on hold for the time being may have helped to steady some investor nerves, at least in the short term, and although some commodity prices, notably oil, seemed to have bottomed out in late August for the moment, waning investor interest has generally pushed borrowing costs higher for emerging markets and served to curtail debt issuance.

Some commentators expect countries with strong fundamentals (such as sturdy domestic growth, current account surpluses and strong currency reserves) will prove less fragile than others, such as Russia, Turkey, Brazil and South Africa. They point out emerging-market central banks in general are in a far stronger position to deal with external economic shocks than they were in the 1990s, thanks to the greater prevalence of flexible exchange rates and the relative decline in foreign currency debt loads.

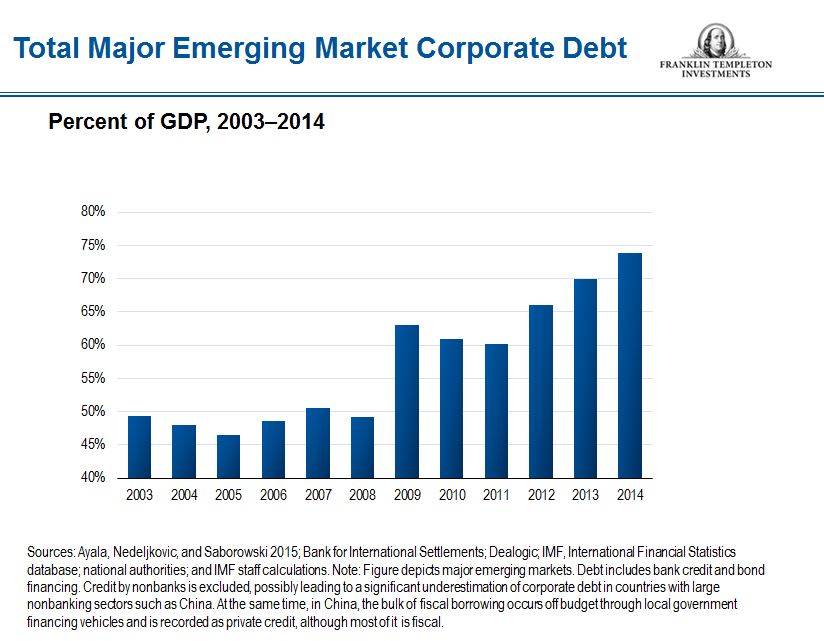

However, growing foreign currency debt levels among households and corporations are coming in for increasing attention. According to the IMF’s latest financial stability report, the debt of nonfinancial firms in emerging markets shot up from US$4 trillion to US$18 trillion between 2004 and 2014, while the average emerging-market corporate debt-to-GDP ratio grew by 26 percentage points in the same period, although with great variation from one country to another.3

Many emerging-market companies will find it difficult to service their debt when the Fed moves to raise rates, especially in the context of slowing growth in their domestic economies. As the IMF points out, emerging-market financial crises in the past have often been preceded by rapid growth in leverage. One nightmare deflationary scenario would have price declines in Asia continuing to cut corporate profits, prompting mass layoffs and reducing consumer demand. In this scenario, the drag from Asia would depress already-feeble economic growth in Europe and Japan and dampen dynamism in the United States.

For the moment, however, there is little sign of global growth collapsing. In our assessment, the US economy could potentially grow by 2%–3% this year, and the Chinese economy may grow by 6%–7%. The Japanese and European economies are also growing, however feebly. We also believe there is some scope for a lift in negative sentiment toward emerging markets. In particular, Chinese authorities’ bid to wean China’s economy away from exports and heavy investment and to promote a more sustainable growth model focused on domestic consumers was always likely to cause angst in some quarters. But there is still confidence in other quarters that the country can pull off this transition. In a recent media interview, IMF Managing Director Christine Lagarde even described the Chinese slowdown as the “healthy” result of needed reforms.

Indeed, some forward indicators are already indicating stabilization in the Chinese economy, for example. Thanks to repeated loosening of monetary policy since November 2014—as well as fiscal incentives that are moving the Chinese economy toward more domestic spending—retail sales have remained robust, and indicators suggest consumer sentiment in China is still buoyant in spite of the stock market havoc seen in June–August. Property prices in a number of large cities have also been rising again. Further clear signs the Chinese economy is stabilizing could lead investors to match the confidence in Chinese prospects shown by IMF Managing Director Lagarde.

The importance of market trust is demonstrated by India. Deemed one of the so-called “fragile five” in 2013 (along with Indonesia, Brazil, South Africa and Turkey), the arrival of a respected central bank chief and the subsequent election of Prime Minister Narendra Modi, touted for his willingness to reform the economy, have allowed India to avoid the worst of the recent rout. While other central banks have been forced to dip into foreign currency reserves to prop up their currencies, the Indian rupee lost just 4% against the US dollar in the first nine months of this year,4 and the country’s reserves have been left largely intact.

Overall, while there are plenty of problem children in the emerging-market space, there are undoubtedly assets and currencies being beaten down by broad-brush assessments of economic prospects that merit renewed attention. According to internal Franklin Templeton assessments, a number of emerging-market currencies are now 15%–30% undervalued. The question is thus whether one is willing to demonstrate enough evidence-based confidence in select emerging markets to look beyond short-term volatility or whether, in the words of one analyst, investing in a market with “strong fundamentals” is akin to “buying the best street in a town about to be hit by an earthquake.”

Europe Caught in the Crosscurrents

Outside the institutional crisis caused by Greece’s debt woes, the outlook for the eurozone has looked relatively benign this year. Ultra-loose monetary policy helped depreciate the euro and boost exports. Low interest rates have led to an upswing in credit, while corporate profitability has improved. The fall in oil prices has boosted real incomes and triggered a rise in consumer spending. On the political front, the populist wave has seemed to recede somewhat. Facing harsh economic reality, the radical left-wing Syriza party elected in Greece at the end of January has been tamed and turned into something akin to a mainstream left-wing party. Populists gained no traction in the early-October elections in Portugal, even though that country also had to implement sweeping spending cuts following an international bailout in 2011.

Many of the catalysts that have been helping Europe remain in place, but others have started to fade. Oil prices, for example, have stabilized since late August. In addition, the eurozone revealed some lackluster data in early October. One of the eurozone’s star performers, Spain, reported industrial output shrank by 1.4% month-on-month in August—an even sharper decline than the 1.2% fall in output reported for Germany. Factory orders in Germany for both July and August also declined.

After a growth spurt that enabled the eurozone to achieve year-on-year growth of 1.5% in the second quarter, such data suggest some of the currency bloc’s major economies are facing headwinds again, with the recent slowdown in the global economy catching up to Europe just as the region was beginning to emerge from multi-year recession and torpor. The German economy, in particular, is exposed to China, its fourth-largest export market. Additionally, matters are not helped by the relative strength of the euro, which has gained in value against a range of currencies, including the US dollar, over the past six months as market sentiment toward the eurozone has improved and the latest Greek crisis was unwound.

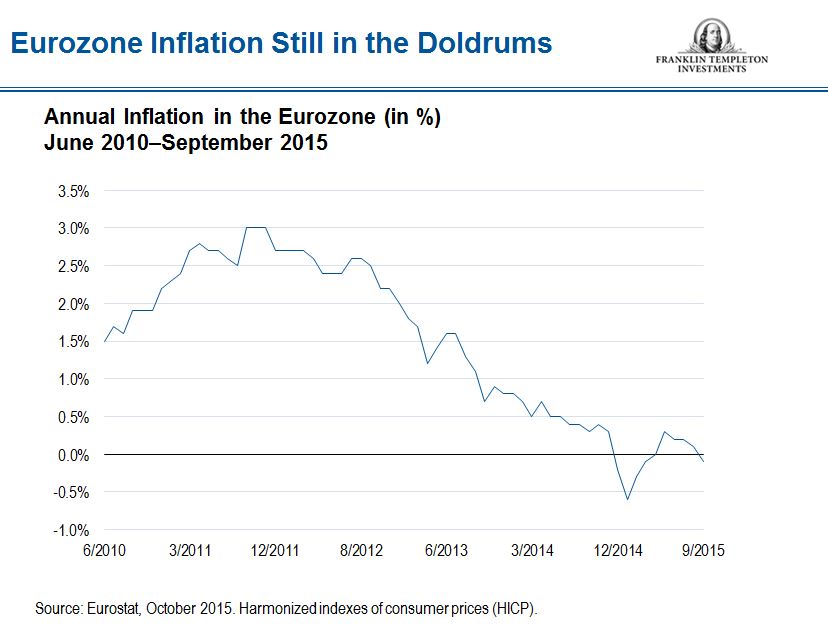

Europe’s prospects are also further complicated by stubbornly low inflation. According to Eurostat, headline inflation slipped back into negative territory in September, with prices 0.1% lower than a year earlier. A key gauge of the market’s long-term inflation expectations, the five-year/five-year breakeven forward rate, which shows investors’ expectations of long-term inflation, fell below 1.6% at the end of September. Such low inflation and inflation expectations come in spite of the European Central Bank’s (ECB’s) quantitative easing (QE) program, launched in March, whereby the central bank committed to purchasing up to €60 billion in assets per month, including government bonds, in a bid to return inflation to its target of close to 2%. At least until recently, many observers had remained confident the eurozone could still avoid a cycle of persistently falling prices. The slide in European inflation is due to lower energy costs, while inflation excluding energy reached an annual 0.9% in September (this figure is still well below the ECB’s target). Deflation imported from Asia remains a threat, while nominal hourly wage growth in the eurozone came in at the miserly rate of 1.6% year-on-year in the second quarter.

Unemployment remained unchanged at 11% in August, meaning that wage inflation is not really present outside some local markets. The sudden influx of migrants from outside Europe this year—especially to labor-starved Germany—further suggests wage pressures will remain weak.

Thus, the ECB may be forced to expand its QE program, especially if the slowdown in emerging markets continues to hit eurozone exports hard and upward pressure on the euro persists.

The ECB meeting in late October resulted in no changes in policy, but ECB President Mario Draghi dropped broad hints that the bank stood “ready to act” if the eurozone recovery continues to disappoint and that “the degree of monetary policy accommodation will need to be re-examined at our December monetary policy meeting.” If, as seems possible, the ECB’s own projections for growth and inflation are reduced in December, then the scene looks set for a range of new measures, which could include an extension of the ECB’s QE program beyond its termination date of September 2016, a hike in the volume of bonds bought (currently about €60 billion per month), an extension of the range of assets eligible for inclusion in the QE program beyond government bonds and certain bank loans, and even further cuts to the already-negative deposit rate charged on bank reserves parked at the central bank. Radical times indeed for monetary policy.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity.

_________________________________________________________________

1 Defined by the Bureau of Labor Statistics as “total unemployed, plus all persons marginally attached to the labor force, plus total employed part time for economic reasons, as a percent of the civilian labor force plus all persons marginally attached to the labor force.”

2 Source: IMF World Economic Outlook, October 2015.

3 Source: IMF Global Financial Stability Report, October 2015.

4 Source: Bloomberg.

© Franklin Templeton Investments

© Franklin Templeton Investments