REITs and other listed real estate companies own some of the finest commercial real estate properties in the United States and, in our view, have historically exhibited strong capital management and have delivered attractive dividend growth.1 Given their enormous capital growth over the past 20 years, REITs represent a significant component of the real estate investment and capital markets.

US REITs Are Readily Accessible

For this discussion, we are referring to publicly available, exchange-traded REITs, which are a type of publicly listed and traded company that invests directly in real estate and related assets. Many REITs specialize in a specific type of property such as shopping centers, warehouses, apartments, hotels, office buildings or self-storage units. REITs offer several potential benefits to investors: diversification from traditional stocks and bonds, income opportunity through relatively stable and potentially growing dividends, and exposure to the real estate sector through a regulated vehicle that trades on an exchange. Currently, we think REITs also look particularly compelling when examining valuations.

Real Estate Value in REITs

Investors in US REIT stocks may use a variety of valuation methodologies when making investment decisions, but we think one of the most important of those considers the underlying value of properties using transactional evidence in the real estate investment market itself.

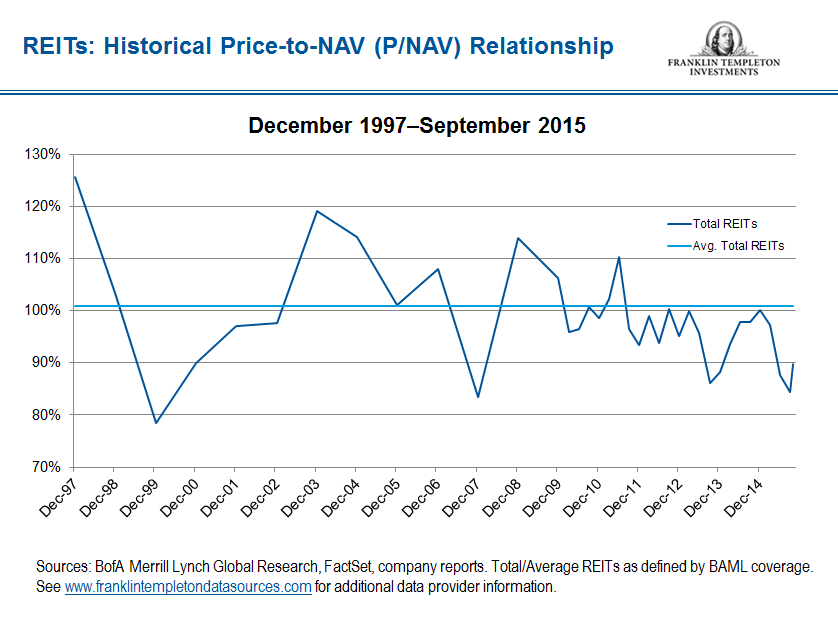

The ratio of the stock price of REITs to the net asset value (NAV) of their underlying real estate assets (price-to-NAV or P/NAV) is an indicator of the relative value of similar assets when comparing the values of listed REITs to the underlying property market values. At times, REIT stock prices may be higher or lower than the values suggested by property market transactions. The relationship of P/NAV suggested by transactional evidence is an important indicator of the “intrinsic” value of a REIT. Also worth noting by investors is the fact that this intrinsic value is an estimate of value of the properties in REIT portfolios and ascribes no value to management, which in most cases adds value for the investor. Recently, US REITs have offered investors an attractive value proposition in terms of this intrinsic value estimate, in our view. At the end of the third quarter, US REITs were trading at meaningful discounts to underlying property values when considering their historical relationship to NAV.

The current average P/NAV for the US REIT market indicates a 10% discount to NAV,2 which means that commercial real estate properties can be purchased through REITs at a substantial discount to their intrinsic value. Looking at their long-term average, US REITs have tended to trade at a 1% premium to NAV,3 which we think makes the current discount even more remarkable.

While a substantial discount would potentially be warranted if either underlying property values were declining or rents and property net operating income were declining, this is not presently the case. In fact, rents are currently increasing in most property sectors and in many US property markets. Fundamental operating performance for REIT portfolios, as represented by same-store net operating income (same-store NOI) growth, a commonly used measure of portfolio income growth for US REITs, appears strong across almost all property sectors and on average, has been improving for over five years.

Recent same-store NOI growth trends have continued to be well above longer-term historical trends and may lead to continued strong shareholder returns if positive earnings and dividend growth are reflected in share prices. We believe these positive same-store NOI growth trends should contribute positively to underlying properties’ NAVs.

Why We Think REITs Are Currently Priced Below Intrinsic Value

The current level of REIT NAV estimates is supported by US real estate market transaction data and public disclosures related to several recent high-profile transactions in which investors purchased partial interests in properties held by US REITs at values that are above the valuation implied by the REIT’s share price. Here are three examples:

- AustralianSuper’s purchase of a 25% stake in the Ala Moana Center in Hawaii, one of the largest shopping malls in the world, from General Growth Properties.4

- Norway’s sovereign wealth fund’s purchase of three prime US office buildings from Boston Properties Inc.5

- A joint venture between the Government Investment Corporation of Singapore and Heitman purchased a 49% stake in eight regional malls for approximately $2.6 billion from Macerich.6

As further evidence of REITs trading at below intrinsic property values, several privatizations of REITs have occurred in 2015, with most of the buyers being private equity funds that typically have stated return expectations that are relatively high when compared to the property investment market as a whole.

Our analysis of these transactions in the context of REIT property portfolios causes us to conclude that the current price discount to NAV available in the US REIT market is something that investors interested in gaining exposure to high-quality commercial real estate should take note of.

In addition, while the transaction examples all involved the purchase of US assets, it’s interesting to note that the buyers include both US firms as well as offshore, global investors. Our analysis further indicates similar opportunities for investors to potentially benefit from historically attractive REIT pricing versus private real estate pricing may present themselves in other listed real estate markets our team is exploring around the globe.

Want to learn more? Read “REITs in Rising Interest-Rate Environment.”

The comments, opinions and analyses are the personal views expressed by the investment manager and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice, and it is not intended as a complete analysis of every material fact regarding any country, region, market or investment.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal.

Investors should carefully consider a fund’s investment goals, risks, charges and expenses before investing. To obtain a summary prospectus and/or prospectus, which contains this and other information, talk to your financial advisor, call us at (800) DIAL BEN®/342-5236, or visit franklintempleton.com. Please carefully read a prospectus before you invest or send money.

_____________________________________________________________

1 Past performance is no guarantee of future results.

2 Source: BofA Merrill Lynch (BAML) Global Research, FactSet, company reports, as of 9/30/15. See www.franklintempletondatasources.com for additional data provider information.

3 Ibid.

4 General Growth Properties represented 2.85% of total net assets of Franklin Real Estate Securities Fund and 1.33% of total net assets of Franklin Global Real Estate Fund as of 9/30/15. Holdings subject to change.

5 Boston Properties Inc. represented 3.67% of total net assets of Franklin Real Estate Securities Fund and 1.96% of total net assets of Franklin Global Real Estate Fund as of 9/30/15. Holdings subject to change.

6 Macerich Co. represented 2.07% of total net assets of Franklin Real Estate Securities Fund and 1.03% of total net assets of Franklin Global Real Estate Fund as of 9/30/15. Holdings subject to change.

© Franklin Templeton Investments

© Franklin Templeton Investments