Equity Investment Outlook October 2015: Global Growth Scare: Is it Warranted?

During the third quarter, global markets were roiled by heightened investor uncertainty and downright fear that China’s slowing economic growth might tip the global economy into recession. The selling pressure that took hold in mid-August had all the elements of a mini panic. The only assets that held their value or posted gains were cash and investment grade bonds. The further out one looked on the risk spectrum, the worse the decline. Non-investment grade bonds traded off 3-5%. Even the 6% decline in the S&P 500 Index during the quarter was relatively benign compared to smaller cap stocks that pulled back nearly 12% and emerging market equities that tanked nearly 18%. China and the economies that depend most directly on China’s demand were hit hardest: the Chinese market fell 30% and Brazil was down 33%.

The key development precipitating the sell-off was China’s decision to let its currency devalue versus the U.S. dollar. This was read by global markets as tacit acknowledgement by the Chinese authorities that China’s growth was flagging and needed a lift from a weaker currency. Given the leading role that China has played in driving global growth over the past decade, investors ran for the exits, fearful that a recession in China could trigger a global recession. Our response is “not so fast.” In China and the economies dependent on it, concern is completely justified by the facts. The “miracle” hyper growth phase of China’s economic development may very well be over, leaving China to manage a potentially difficult downshift into an extended period of much slower growth (slow growth, not zero growth). This could have serious, lasting implications for many emerging market economies and stock markets. That said, the implications for the U.S. are much more nuanced and the current level of investor concern may be unjustified and overdone. We think a strong case can be made that the U.S. economy can decouple from a Chinese slowdown. Some even argue that the U.S. economy will prove to be a net beneficiary of the cooling-off in Chinese and emerging market growth. This Outlook will look at the growth scenarios for China and China-dependent countries compared to the U.S.

China

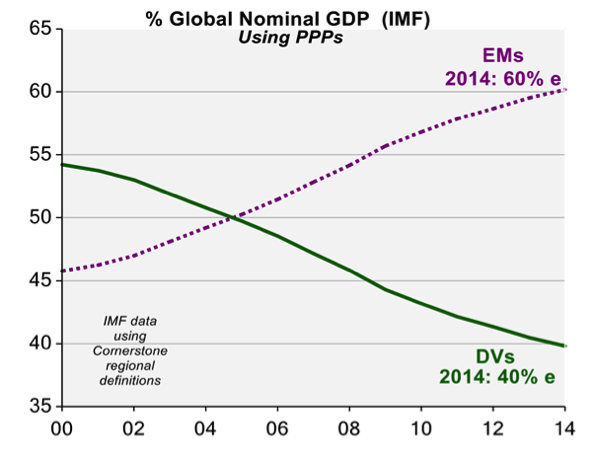

China is experiencing a significant slowdown in its growth rate, a change that is having wide-ranging spillover effects. Year after year of double digit Chinese gross domestic product (GDP) growth helped power global growth over the past 15 years (Figure 1). Since the year 2000, the emerging markets’ share of the global economy has increased from above 45% to 60% now (Figure 2). Investors are rightly concerned about the impact of a Chinese slowdown on global growth, but we think that the brunt of this slowdown will be borne by China and its main suppliers (not the U.S.). China’s voracious appetite for commodities during its go-go days helped lift growth for many commodity and goods producing countries. Now that China’s growth is slowing, demand for these commodities is waning and prices are plummeting. This, of course, is devastating to the profitability of commodity producers and the countries dependent on them (e.g. Brazil, Russia, Indonesia, Malaysia, South Africa and Australia). The big question is: could this commodity deflation be good news for the U.S. consumer? We try to answer this question later in this Outlook.

Figure 1:

Source: Cornerstone Macro, Economic Research, October 11, 2015 (end date: 6/30/15). Year-on-year growth rate.

Figure 2:

Source: Cornerstone Macro, Economic Research, October 11, 2015 (end date: 12/31/14).

PPPs: Purchasing Power Parities; EMs: Emerging Markets; DVs: Developed Markets; e: estimate; IMF: International Monetary Fund.

To some extent, China’s slowdown has some self-reinforcing elements. As China tries to wean itself off of an investment, export and real estate-driven growth model, it needs to stimulate consumer demand to take up the slack. But that is easier said than done. The problem is, as China attempts to downsize its bloated, inefficient, unprofitable, and often state-owned enterprises, it runs the risk of pushing up unemployment. Many vested interests may be unwilling to swallow the painful medicine required to reorient the economy away from what worked so well for so many years. Vested interests run the gamut from Communist party leaders who do not want the unrest that might come from rising unemployment, to municipal politicians and trade unionists who want to protect local enterprises and local jobs, to the owners of enterprises who are receiving subsidies. Economists will argue that the faster China can accomplish this “rebalancing” of its economy, the sooner sustainable growth will return. One only needs to look at Japan and its two lost decades of growth to appreciate the cost of protecting vested interests and deferring swallowing the medicine. Our guess is that China’s adjustment process is likely to be quite protracted and may be punctuated by considerable social unrest.

The Chinese slowdown is having a spillover effect on numerous other countries dependent on exports to China. This includes commodity producers such as Australia, Brazil and Indonesia, as well as goods producers such as Korea and Japan. In other words, China is now exporting deflation to large parts of the emerging and developed worlds. Commodity prices are now near 25 year lows and it is hard to see them turning around any time soon (Figure 3).

Figure 3:

Source: Bloomberg (end date: 9/9/15).

U.S. companies that depend on exports to China or are manufacturing and selling within China are clearly going to experience lower earnings during this adjustment period. On the other hand, U.S. companies with a domestic U.S. focus could experience growing earnings for reasons we discuss in the following section.

U.S.

Ever since the U.S. economy emerged from the financial crisis of 2008, we have consistently, and it turns out correctly, argued that the ensuing recovery would likely be less robust than the typical post-war rebound. First and foremost, housing could not be the engine it traditionally was to pull the economy out of recession. This is because housing was over-built in the years preceding 2008 and inventories of unsold homes and unoccupied homes were high. In addition, banks and other mortgage lenders were reluctant to extend credit. It was clear that lenders in general were more focused on cleaning up their portfolios than on aggressively making new loans. This deleveraging process has kept the housing recovery far more muted than in past cycles.

More broadly, the entire banking system needed to de-lever coming out of the financial crisis. Not only could it not finance a robust housing recovery, but it was unable to extend the usual amount of credit to small and mid-sized businesses, traditionally the largest generators of new jobs in this country. As a result, overall job growth has proven to be somewhat anemic.

Adding to the sub-par recovery was a reluctance on the part of businesses to invest in new capacity given how slow the growth outlook was from 2009-2014. The result was less robust capital spending than normal. Additionally, periods of government sequester and limits on spending meant that government’s contribution to growth was lower than normal. All of this combined to keep overall economic growth sub-par compared to “normal” recoveries. On the other hand, corporate profit margins expanded to record levels and profits recovered far more sharply than expected from recessionary lows. Whether margins can remain high at this point in the economic cycle is a key question we will discuss in the remainder of this Outlook.

One of the side effects of a slow economic recovery in the U.S. and Europe has been the absence of inflationary pressure. This partly reflects plenty of spare labor and productive capacity (at least up to this point) and partly reflects the collapse in commodity pricing over the past 12-18 months – a lot of which stems from the slowdown in China’s economy and a waning of its voracious appetite for commodities. The following chart illustrates just how significantly commodity prices have fallen:

|

Peak |

Current |

% Decline |

|

|

Steel (hot rolled coil $/ton) |

$690 |

$430 |

-38% |

|

3-Month Copper ($/tonne) |

$7,175 |

$5,160 |

-28% |

|

Oil ($/barrel) |

$108 |

$45 |

-58% |

Source: Bloomberg (current prices: 9/30/15).

While all commodity prices have dropped in the past year, it is worth zeroing-in on the declines in oil and natural gas prices which are the result of more than just a drop in Chinese demand. These declines also reflect the stunning increase in U.S. shale oil and gas production over the past several years, and the decision on the part of Middle Eastern oil producers and Russia to push new supplies into an already over supplied market. There is much speculation as to the motivation behind the new supplies coming out of certain Organization of the Petroleum Exporting Countries (OPEC) and Russian producers. We suspect that they miscalculated and thought that they could take market share from higher-cost U.S. producers and that their incremental volumes sold would offset a somewhat lower price. Instead, the oil prices have collapsed by more than 50% leaving all producers, high cost and low cost, struggling with sharply lower oil revenues and earnings. Part of the reason is that U.S. oil production has proven to be much more resilient than anyone expected, even at far lower prices. The old saying that “necessity is the mother of invention” certainly applies to the U.S. oil patch where producers have succeeded in reducing their per well drilling and completion costs by a stunning 30-40% in just the past year. This has dramatically lowered the breakeven cost of producing oil in the U.S. So while U.S. oil production is finally beginning to drop and will probably continue to drop in response to sub $50 prices, longer term we think abundant new, low cost shale oil supplies will prevent oil prices from getting back to the $100 level any time soon. This should prove to be bullish for larger oil consuming economies around the world.

As a result of low commodity prices and low inflation, the Federal Reserve (the Fed) has been able to keep interest rates low for an extended period even with signs that the U.S. economy is finally on the mend. By not raising rates in September, however, the Fed spooked the markets which began to think that the Fed should begin the long journey toward a more neutral rate, in line with inflation of 1.5-2.0%. After all, unemployment levels are now hovering around 5%, credit markets and banks are extending credit, the consumer is in good shape and housing markets are in a clear recovery mode. One has to wonder, “if not now, when?” So when the Fed elected not to raise rates in September, investors had to ask if the Fed might actually be concerned about slowing growth. Did the Fed perceive a weaker economy than the rest of us? We believe one reason the Fed may have delayed raising rates was its concern that higher rates would cause the already strong U.S. dollar to strengthen even further. This would hurt U.S. exports, help imports to take share from U.S. manufacturers and maybe lead to a somewhat less robust economic expansion. We do not think that weaker growth from China on its own is the issue. Direct exports from the U.S. to China represent less than 1% of total U.S. GDP. Exports from the U.S. to the rest of the Pacific Rim countries as well as to Russia and Brazil collectively represent only 1.3% of U.S. GDP. We understand that some of our larger trade partners such as Canada, Japan and the European Union are more exposed to China and other emerging markets, but we still think the benefits to the U.S. consumer of lower energy prices and a stronger dollar will offset negative trade flows.

The question of when the Fed will start to raise interest rates is in our opinion less interesting than the question of how rapidly rates will rise once they begin. Again, we have consistently argued that any rate rise will be gradual, reflecting both relatively slow economic growth and persistent low inflation. In other words, despite an eventual upward bias to interest rates, Fed monetary policy should remain accommodative for some time. This would be a favorable environment for stocks.

Other potential tailwinds for the market would include gradually rising employment levels and perhaps a modest acceleration in wage gains. Since the consumer represents nearly 70% of the U.S. economy, rising employment and wages should foster improving economic growth via rising consumer spending. Additionally, housing now appears to be expanding, thus contributing to prospects for steady, if not better, economic growth. Finally, if investors eventually believe that low inflation and low interest rates are likely to persist, equity valuations could improve.

Offsetting these potential tailwinds, however, are a number of headwinds both to the economy and to the stock market. Our chief concern would be slower growth and the potential for weaker corporate profits. We have already discussed the ramifications of the China slowdown, its ripple effects through the emerging markets and its implication for U.S. corporate earnings. Second, the deflation we have seen in commodities could have a spillover effect in numerous ways. Third, the bond super cycle is over. Interest rates have declined steadily since the early 1980s, causing a blossoming of the stock market. A reversal in the long-term trend of interest rates could have a negative effect on equity valuations. Finally, U.S. productivity growth appears to have stagnated. Couple lower productivity growth with rising wages, and corporate profits could come under pressure. We believe that a significant portion of lower productivity gains are a problem of measurement and definition rather than reality, but one cannot dismiss the issue.

In sum, we remain optimistic on the economy and ultimately on the stock market. What we experienced in the third quarter was a fairly normal 10% correction and not, in our view, the beginning of a long-term bear market. Nonetheless we continually test our assumptions as new data emerge, and as our long-term clients hear us repeat over and over, we are very focused on finding investments in companies that are experiencing growth independent of the economic outlook.

As always when we go through difficult periods, we want to thank you for your patience and your confidence in our ability to navigate choppy seas. Please call us if you have specific questions.

Sincerely,

John Osterweis

Matt Berler

____________________

Past performance is no guarantee of future results.

This commentary contains the current opinions of the author as of the date above, which are subject to change at any time. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but is not guaranteed.

The S&P 500 Index is an unmanaged index that is widely regarded as the standard for measuring large-cap U.S. stock market performance.

The Bloomberg Commodity Index is made up of 22 exchange-traded futures on physical commodities. The index currently represents 20 commodities which are weighted to account for economic significance and market liquidity, subject to index-weighting restrictions.

These indices reflect the reinvestment of dividends and/or interest income and are not available for investment.

All return and currency figures are shown in USD.

One cannot invest directly in an index. [17179]

© Osterweis Capital Management

© Osterweis Capital Management