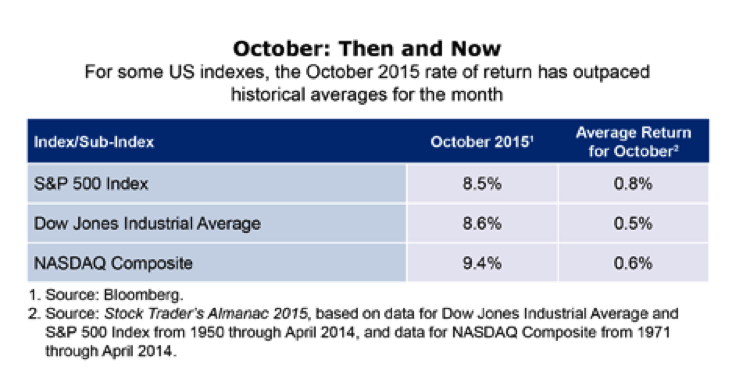

October was a month of ironies. Despite being widely perceived as a bad month for equities, October saw them post strong returns, with both the S&P 500 Index and the Dow Jones Industrial Average gaining nearly 9%. October proved to be the best-performing month for stocks over the past four years—following one of the worst quarters for stocks in the last few years.

Stocks outside of the country have also experienced recent gains, and this positive performance has been widely attributed to accommodative central bank policies. This is particularly so in the US, where earnings certainly haven't helped returns. Recall that October started with a bang in the US on the tail of a lackluster September jobs report that made investors assume a rate hike in the near term was less likely. This was followed by mediocre to disappointing economic data, not to mention a weak earnings season. However, the month ended with the FOMC meeting and announcement, which was perceived to be more hawkish and seems to have cooled interest in stocks.

So what is ahead for US stocks?

We think the possibility of a rate hike in December, despite a still very accommodative Fed, could create a headwind for stocks. This may counter the positive impact of a more functional Congress. Last week, somewhat anticlimactically, Congress passed legislation not just raising the debt ceiling but also approving an increase in both domestic and defense spending. In one fell swoop, the dual threats of a government shutdown and debt default were averted until March 2017. This is extremely important given that the US was closing in on its debt ceiling on November 3. After several years of acrimonious disagreement, Congress appears to be cooperating, which should benefit US stocks.

However, the headwinds for US stocks in the near term are formidable, including the October run-up that suggests valuations are stretched. While improved earnings are needed to power stocks higher, we are unlikely to see that happen until 2016. We also think largely mediocre economic data could apply downward pressure on select stocks, particularly given manufacturing disappointments, as well as some regional weakness.

In short, we don't expect to see the same ebullient returns in November that we saw last month. Instead we expect a more muted environment that could put the "no" in November. This October should, however, remind investors that they need to remain fully invested in stocks—because you never know when you might have another "Rocktober" month. Particularly in an environment where accommodative monetary policy continues to shape risk and reward profiles of asset classes.

Kristina Hooper is the US Investment Strategist and Head of US Capital Markets Research & Strategy for Allianz Global Investors. She has a B.A. from Wellesley College, a J.D. from Pace Law, a master's degree from Cornell University and an M.B.A. in finance from NYU, where she was a teaching fellow in macroeconomics.

Subscribe Today

The Upshot is available as a subscription for financial professionals only. New issues will be delivered via email every Monday. Visit us.allianzgi.com/theupshot to learn more.

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

A Word About Risk: Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

There is no guarantee that an active manager’s investment decisions and techniques will be successful. It is possible to lose some or all of your investment using active management.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

AGI-2015-11-02-13704