Clearly, this year has been challenging for investors in emerging markets, which have generally underperformed developed markets. However, we have seen recent data showing the trend of asset outflows may be reversing as more investors are putting their money back to work in emerging markets. This is encouraging to us, but even if the type of volatility we saw this summer flares up again, by no means do we feel it’s time to abandon the asset class. We consider many of the factors driving recent volatility in emerging markets to be temporary and compounded by typically low summer liquidity—thus we believe we have grounds to be optimistic longer term.

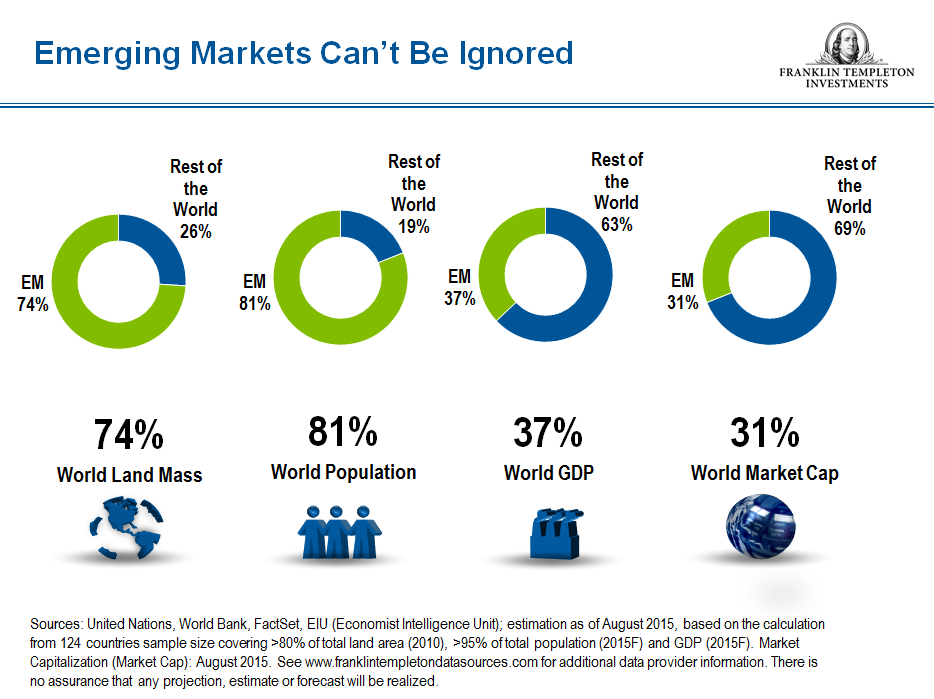

Emerging Markets Can’t Be Ignored

In our view, regardless of short-term investor shifts in sentiment, emerging markets simply can’t be ignored. They are a significant part of the global economy today in terms of world land mass, population, gross domestic product (GDP) and equity market capitalization.

It is true that emerging markets’ economic growth in general has been slower this year than perhaps it was in the past, but we don’t see systemic risk present in emerging markets. There are pockets of vulnerability in some countries, but by and large, we don’t see an asset-class-wide doomsday situation. Foreign reserves and public debt as a percentage of GDP generally appear to be at healthy levels, and GDP growth overall remains more robust than for developed markets. Broadly speaking, we aren’t seeing an emerging market equity crisis brewing. Most investors globally remain underinvested in emerging markets so in our view the question is not whether to invest in emerging markets—the question is which companies in which markets to invest in? We believe emerging markets remain growth drivers of the world.

Two Main Factors Impacting Emerging Markets: The Fed and China

In our view, there have been two main factors contributing to emerging markets’ performance this year: possible monetary policy tightening ahead from the US Federal Reserve (Fed) and concern about slowing economic growth in China. We think the markets have overreacted to potential US rate increases ahead. It is interesting to note that a number of central banks in emerging markets have actually called on the Fed to raise rates to end the uncertainty.

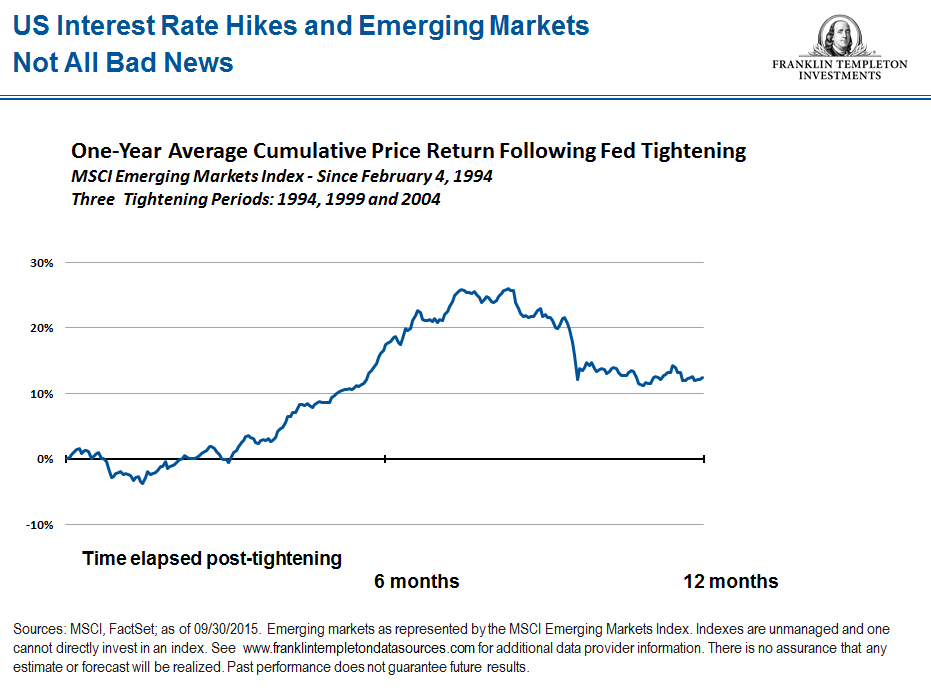

Historically, we have seen similar sharp market gyrations (typically downward) in both emerging-market currencies and equities in advance of Fed tightening. However, during the actual implementation of previous US rate-rising cycles, equities have been able to rebound—illustrating our belief that markets tend to price in a worst-case scenario prior to the event. Looking at the MSCI Emerging Markets Index, the average one-year performance following a Fed interest rate increase was 12.4%.1 You can see in the chart below that following the initiation of the last three periods of Fed tightening in 1994, 1999 and 2004, the market did not collapse.

If the Fed aggressively raises rates in a series of moves, we do see that as bearish for emerging markets, but that scenario doesn’t seem likely to us. US multinational companies (and thus the broader US economy) depend vastly more upon emerging market countries (most notably Asia) for growth than they did during previous rate rise cycles. Hence, a greater feedback mechanism exists now, whereby declines in emerging market growth and currencies have a far larger direct impact upon US economic growth and, in turn, influence the freedom of the Fed to raise rates. We also must not forget that other central banks outside the United States have been adding liquidity via quantitative easing or interest rate cuts, including in Europe, Japan and China.

In terms of the impact of slowing growth in China, again we feel there has been unwarranted investor panic. While China’s equity market volatility and the government’s ineffectual attempt to intervene directly to support prices have dominated headlines this past summer, we remain confident that the government’s efforts to effect a broad economic rebalancing will succeed. While news of China’s market ups and downs makes for splashy headlines, we expect the impact of recent declines in mainland share indexes to have limited impact on the broader economy due to the low level of household wealth allocated to equities in China (less than 20%, according to our research). As household exposure to local equities is very low, we believe there would not be a profound wealth effect even if we saw a market crash in China.

The government is also systematically addressing the structural weaknesses in the economy—most notably concerning debt—with the mandated transfer of banks’ bad loans to asset management companies, higher non-performing loan (NPL) provisioning at banks, and the development of local government debt markets. Furthermore, while aggregate levels of debt are relatively high, given China’s level of economic development, the country also has a uniquely vast level of state assets, including foreign exchange reserves and state-owned enterprises that provide balance. Continued rapid rises in wages and dramatic increases in the number of service jobs (typically in the private sector) in our view also help counter the housing slowdown and manufacturing job losses. The increased flexibility in the renminbi represents another welcome move towards financial market liberalization.

Asian Economies Appear in Good Shape Overall

On a host of measures, from current account deficits to foreign exchange reserves to the proportion of debt that has been issued in local currency versus in US dollars, many Asian economies appear to us to be more resilient than they have been historically.

A particular example is India, which illustrates the disassociation of sentiment from economic fundamentals. Its currency has declined about 5% versus the US dollar,2 but while this decline may parallel the decline and volatility in 2013 that was associated with the announcement of Fed tapering, India today is far stronger from a macroeconomic perspective. India’s commercial debt of US$185 billion3 is very manageable in our view, and historically, even during turbulent periods, refinancing has not been a major problem. More importantly, since late 2013, India’s current account deficit has improved from US$88 billion to below US$20 billion,4 foreign exchange reserves now cover 10 months of imports compared to seven previously,5 and the outlook on foreign direct investment improved with the election of Prime Minister Narendra Modi.

We believe Southeast Asia as a whole has particularly good growth potential, with countries such as Myanmar, Laos, Cambodia and Vietnam starting to embrace market economics, making available substantial underused and undervalued resources—both natural and human—that can be utilized by entrepreneurs from more developed regional economies to the benefit of both. Vietnam in particular has been booming, with GDP growth forecast by the International Monetary Fund (IMF )at 6.5% this year,6 a figure that outpaces emerging markets as a whole. Recent trade agreements should also prove beneficial for Vietnam, including a deal inked with the EU and its inclusion as part of the proposed Trans-Pacific Partnership, which would further open up its export markets.

Even the more mature economies in the region such as Indonesia, Thailand and Malaysia still have substantial growth potential in our view, with favorable demographics, ongoing urbanization and structural reforms conferring the possibility of ongoing strong economic progress.

There are of course some near-term challenges in the region. Indonesia’s currency has fallen about 9% against the US dollar so far this year,7 but the macro economy overall has improved since the Asian financial crisis in 1997 and we think Indonesia appears to be in better shape to handle tighter US monetary policy than it had been in the past. Additionally, a recent reshuffle of the president’s economic team may mark a renewed focus on pushing through pro-growth and anti-corruption reforms. A number of key projects are planned or have launched, including a trans-Sumatra toll road, plans to build over 20 ports, and an ambitious power investment program.

In Thailand, an important contributor to disappointing economic growth in the past few years was the government’s poor implementation of its planned infrastructure investments. During 2014, political turmoil resulted in a large number of fiscal funds not being disbursed, and similarly throughout 2015, the government has failed to fully disburse the funds available (the infrastructure budget in particular has suffered from the lack of disbursement). Observers expect GDP growth to accelerate in 20168 as the government ramps up near-term fiscal stimulus (primarily directed at rural areas in the form of loans and infrastructure), paired with substantial longer-term infrastructure projects ranging from metro lines in Bangkok, to long-distance road and rail links. Importantly, both China and Japan have signaled interest in co-investing in a number of projects that would provide additional capital. In aggregate, these infrastructure plans alone should help provide a boost to GDP growth over the next four years. There are also extensive plans to encourage private sector and foreign direct investment, which when paired with recently improving export data, may result in a meaningful boost to growth in Thailand. We believe banks in Thailand should be well-placed to potentially benefit from these macro improvements.

Emerging Market Values

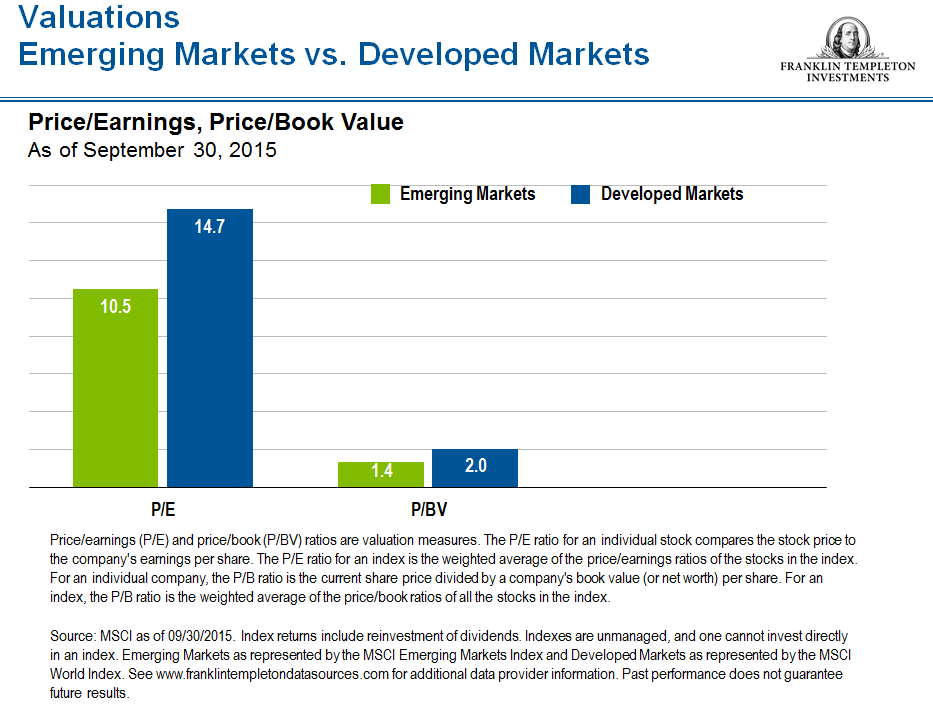

As investors in emerging markets, our primary focus is on the underlying business models and fundamentals of the individual companies we invest in, more so than broader macro views. We have been cautiously looking to increase our exposure to companies in which we continue to see strong long-term upside potential, but which we believe have nonetheless been unduly sold off. As we look forward, it is important to note that times of stress in financial markets can offer the largest upside potential in the medium term. Currently, emerging markets appear undervalued versus developed markets, based on price-earnings and price-book ratios. While heightened market volatility can be unsettling, our investment process looks beyond the short term, and aims to find and invest in well-managed growth leaders at attractive valuations across the emerging markets space. Clearly, many emerging markets are facing headwinds, but we believe there are always opportunities to be found for the next market turn.

Mark Mobius’s comments, opinions and analyses are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding any country, region market or investment.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FTI affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including possible loss of principal. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Smaller-company stocks have historically had more price volatility than large-company stocks, particularly over the short term.

______________________________

1 Sources: FactSet, MSCI. See www.franklintempletondatasources.com for additional data provider information. Past performance is no guarantee of future results. Indexes are unmanaged, and one cannot directly invest in an index.

2 Source: Bloomberg, as of November 9, 2015.

3 Source: CLSA Research, August 2015.

4 Source: Reserve Bank of India, as of June 2015.

5 Ibid.

6 Source: IMF World Economic Outlook database, October 2015. There is no assurance that any estimate or forecast will be realized.

7 Source: Bloomberg, as of November 9, 2015.

8 The IMF projects Thailand’s GDP to grow at 2.5% in 2015 and 3.2% in 2016. Source: IMF World Economic Outlook database, October 2015. There is no assurance that any estimate or forecast will be realized.

© Franklin Templeton Investments

© Franklin Templeton Investments