Global Economic Perspective: November

Fundamentals Reassert Themselves Ahead of Likely US Rate Rise

Even as the Fed has sought to give much clearer signals about its intentions to raise base rates, the performance of US risk assets has continued to improve, suggesting that markets are comfortable with the prospect of a small rise in base rates in December. Investors in risk assets seem to have renewed their focus on the fundamental strength of the United States and become less worried about the global outlook. In terms of equities, the S&P 500 had its best month in four years in October, while booming corporate bond sales continued to meet high demand, appearing to reflect confidence in the strength of the US corporate sector as well as the persistence of low market interest rates.

In a late-October statement, the Fed dropped prior references to the risks to US growth and inflation stemming from skittish financial markets and a sluggish global economy, and it singled out solid increases in the domestic US economy in areas such as spending and investment, along with further improvement in the housing market. The Fed’s message was seen by the markets as reinforcing the likelihood of an increase in base rates at its next policy meeting in December. The message was driven home further by Fed Chair Janet Yellen, who in a congressional hearing in early November asserted that the downside risks to the US economy from global developments had diminished since September and that there has been a significant fall in labor market slack.

At the same time, several factors have indicated that growth in the US economy remains less than stellar, especially on the corporate side. Industrial production in September was down 0.2% compared with the previous month. Durable goods orders fell by 1.2% in September, while the Institute for Supply Management’s manufacturing purchasing managers’ index (PMI) fell to barely over the 50 mark in October, the level that separates expansion from contraction. Notably, the initial estimate for third-quarter gross domestic product (GDP) growth came in at an annual rate of 1.5%, well down from the second quarter’s 3.9% rate.

But the third-quarter GDP number also revealed that consumption growth remained robust, and many observers expect growth to pick up in the year’s final quarter as the rundown in corporate inventories that impacted the third-quarter data is taken out of the equation. The third-quarter GDP figure showed that household consumption was growing at a robust 3.2% pace. Auto sales increased 13.6% in October over the same month in 2014. On the corporate side, the disappointing manufacturing PMI number has to be considered alongside a much better reading for services, while the US trade deficit narrowed sharply in September due to a rebound in foreign countries’ demand for American goods in spite of a strong US dollar. Additionally, the potential for another “fiscal cliff” that would have sapped sentiment was removed by the striking of a congressional deal in late October to raise the federal government’s debt ceiling. Of particular note is the fact that the budget deal does not contain the kind of spending cap that had been imposed in previous deals.

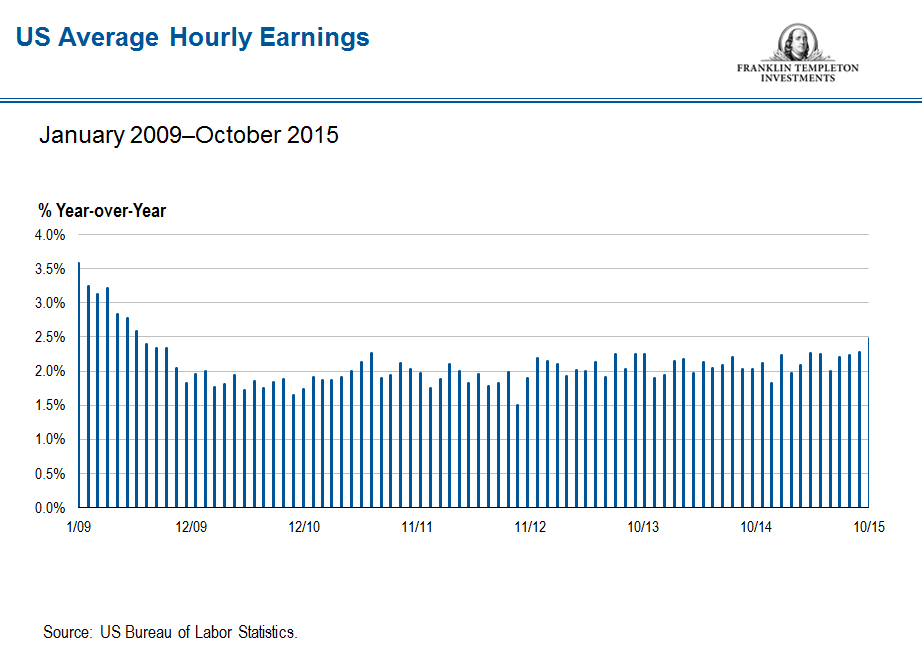

But the most important measure of the robustness of the US economy remains jobs growth. The October nonfarm payroll figure came in at 271,000, the highest number this year and comfortably above consensus expectations of 180,000. With the unemployment rate falling to 5.0% and wages rising at their fastest rate since 2009, the unambiguously strong report sparked a rise in the US dollar and Treasury yields as markets factored in increased expectations for a December rate rise.

While the latest jobs data may be decisive in convincing Fed policymakers to begin normalizing monetary policy, lingering softness in some parts of the US economy means that policy tightening should, as Janet Yellen put it, proceed at a “gradual and measured pace.” This softness is most marked in overall inflation numbers. Overall inflation remains remarkably tame: The Fed’s preferred measure, the price index for core personal consumer expenditure, which excludes volatile food and energy prices, rose 1.3% in September, which was still below the annual rate of 2% that the Fed believes is most consistent over the longer run with its mandate for price stability and maximum employment.

However, we believe that things may soon start to change on the inflation front. Core consumer price inflation rose 1.9% in the 12 months to the end of September—and we fully expect a tightening labor market and robust consumer spending to progressively push it higher—one more reason for the Fed to commence policy normalization.

Upturn in Sentiment Buoys Some Emerging-Market Risk Assets

There has been a welcome stabilization in global financial markets in recent weeks. A major catalyst, especially in emerging markets, was the conviction that the Fed was not going to hike base rates in the immediate future against a backdrop of low inflation, weakening job gains and global economic uncertainties. The Fed subsequently changed its tone and gave its clearest sign yet that it might raise rates in December, but investors seemed to have become relatively more relaxed about the prospect of higher US rates than they were throughout the middle part of this year. The upturn in sentiment has been most evident in some emerging markets, where equity prices have risen and credit spreads have tightened. Some currencies have also begun to reverse their recent declines, with the South Korean won rising almost 4% against the US dollar in October and the Indonesian ringgit climbing over 7%. Risk assets have also been helped by indications from the ECB that it stood ready to expand its QE program, the possibility that the BOJ might do the same, and a decision by the PBOC to further cut interest rates and relax reserve requirements. Further helping risk assets has been the realization that the Chinese have not embarked on a full-scale competitive devaluation of their currency, notwithstanding a relatively small cut in the value of the yuan in early August.

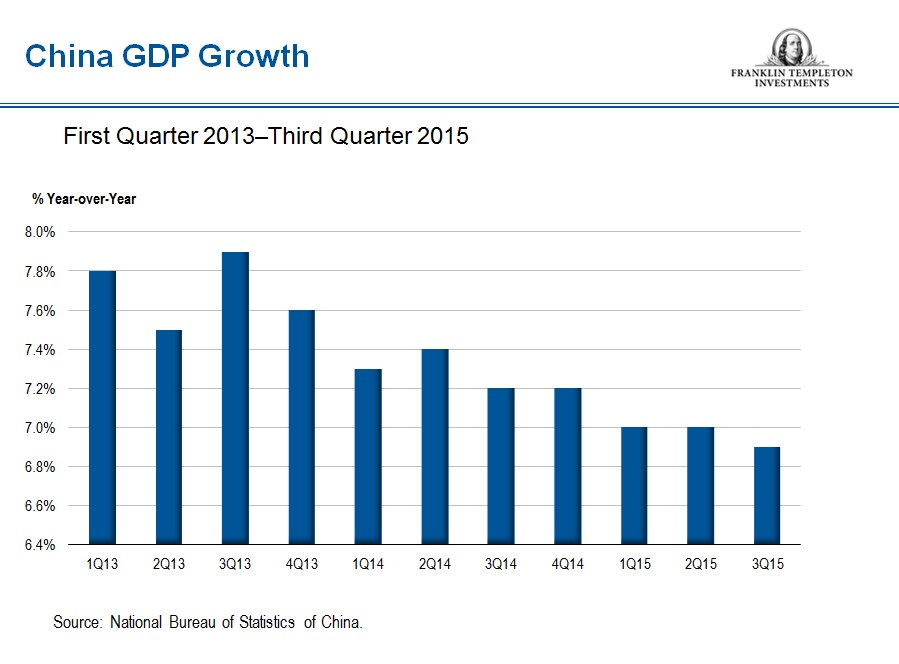

The question now is how long the relative improvements of recent weeks can last. Without a substantial pickup in growth prospects, it is difficult for us to get too excited. In this regard, it is worth remembering that central bank dovishness has been largely inspired by relatively subdued global growth, with the International Monetary Fund pruning its global growth forecasts to 3.1% in 2015—which, aside from the financial crisis period, would be the lowest rate since 2002—and to 3.6% in 2016.1 China reported annual GDP growth of 6.9% in the third quarter—much better than any other large economy but weak by Chinese standards. Suspicions are rife about the reliability of such GDP figures, with indicators such as steel consumption and electricity use suggesting substantial weakness in heavy industry and manufacturing, while the official manufacturing PMI stood below 50 for the third consecutive month in October. There remains substantial overcapacity throughout China’s heavy industry, which, together with a large build-up in private-sector borrowing, may make the Chinese authorities reticent about over-generous amounts of stimulus to boost growth again.

Aside from manufacturing, however, Chinese consumer spending has remained brisk, with retail sales rising almost 11% in the year to end-September, according to the National Bureau of Statistics of China, with growth actually accelerating in the past few months. The growth in domestic consumption is being fed by rising wages and a rising services sector. Such trends are in keeping with the Communist Party’s latest five-year plan to restructure the Chinese economy to make it less reliant on investment in heavy industry and other capital-intensive sectors and more driven by innovation and consumption. Nevertheless, even in manufacturing, monetary loosening, extra infrastructure spending and increased pressures on banks to boost lending offer the prospect of stabilization at least in the short term.

In sum, while China’s manufacturing sector—which drove China’s rise to its place as the world’s second-largest economy—has been losing steam, it is being supplanted by a domestic, consumer-led economy propelled by a rising middle class with growing income. Other Asian countries are on a similar trajectory. In late October, South Korea announced that its economy grew at an annual rate of 2.6% in the third quarter, the fastest pace in five years, aided by a stimulus-driven rebound in domestic demand that outweighed the negative effect of slowing Chinese and global demand.

However, Asian markets do not appear to be out of the woods just yet: Export-dependent Taiwan reported a 1% year-on-year GDP decrease in the third quarter, and the BOJ made a late-October announcement of reduced growth and inflation forecasts for Japan. Serious questions also remain about the state of the overall Chinese economy and of commodity-dependent economies in Asia and throughout the emerging-market universe. A quarter-point hike in the US federal funds rate might provide a welcome dose of clarity to Asian markets and emerging markets more generally, but any indication that the path of further increases will be other than short and shallow could yet have a further disruptive effect.

European Economic Improvement Poses Dilemma for Monetary Policy

Europe finds itself in a relatively unusual situation in which the overall economic environment continues to improve, but the ECB has given definite hints it intends to ease monetary policy even further, possibly in December. Some of the most dramatic improvements in economic performance are being seen in the countries most hurt by the financial and sovereign debt crises that started in 2008. Ireland has reclaimed its position as Europe’s star performer, with the European Commission forecasting the country’s GDP growth to exceed 6% this year. Spain is not far behind, registering annual growth of 3.4% in the third quarter, and even Italy has been showing signs of life. Manufacturing PMI surveys for all three countries in October showed that momentum has continued to build.

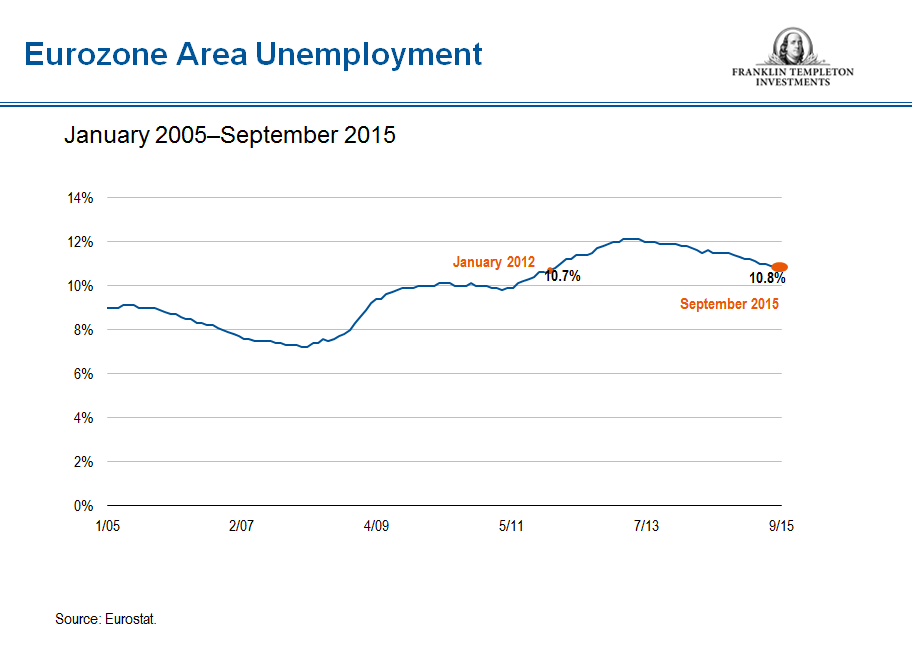

Surveys have also underlined the progressive improvement in the eurozone’s fortunes overall. Eurozone unemployment hit an almost four-year low of 10.8% in September 2015. The eurozone composite PMI compiled by Markit hit 53.9 in October, one of the strongest readings over the past four years and well above the dividing line between expansion and contraction.

Moreover, the ECB’s own data have shown credit conditions to be improving. The narrow M1 measure of cash and checking accounts—sometimes considered as heralding short-term spending—rose at a hefty annual rate of 11.7% in September. The ECB’s decision to start buying €60 billion per month of mostly government bonds in March as part of a €1.1 trillion QE package has helped ease credit by lowering interest rates, although the rate of improvement might seem disappointing in the short term. The ECB has also helped trim countries’ borrowing costs, with yields on government bonds down to record lows. Indeed, by the end of October, yields on two-year debt stood below zero for almost every member of the eurozone, which means investors were effectively paying to own it.

Still, an unemployment rate of 10.8% remains high, and the PMI data merely confirm the region’s “steady but still somewhat lackluster” growth. The European Commission struck a similar note in forecasting eurozone growth of 1.6% this year, rising slightly to 1.8% in 2016. That being said, German new manufacturing orders dropped unexpectedly by 1.7% in September due mainly to weaker foreign demand. This was the third consecutive decrease in the monthly number.

Additionally, inflation is still noticeable by its absence. Prices in the eurozone were unchanged in the year to October, according to Eurostat, marking a slight improvement from September when they dropped to an annual rate of -0.1%. Core inflation (excluding food and energy) stood at 1% in October, up from 0.9% in September. This level was still far from the ECB’s target of just under 2%. Low inflation, together with low inflation expectations and a still-large degree of economic slack explain why the ECB is still widely believed to be preparing another monetary stimulus package.

But the improvement in the eurozone’s fortunes does pose a dilemma for the ECB in our view, all the more so given that renewed expectations for the Fed to raise rates soon have been helping to depress the euro. After strengthening during the summer’s market volatility, the single currency fell against the US dollar in October, providing a useful tailwind for eurozone exporters. Nevertheless, we think the weaker overall outlook for global economic growth could prove the decisive factor in persuading the ECB to further ease monetary policy in a concerted effort to stop the eurozone’s recovery from stalling.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity.

_________________________________________________________________

1 Source: IMF World Economic Outlook, October 2015.

© Franklin Templeton Investments

© Franklin Templeton Investments