It may sound a bit unconventional, but the crowdfunding craze may offer a solution to financing a college education. With the holiday season approaching, Roger Michaud, senior vice president and director of sales for Franklin Templeton’s 529 College Savings Plan, poses the question: Why not ask your family and maybe even friends to chip in for your child’s future? Michaud, chair emeritus of the College Savings Foundation—the leading nonprofit helping American families save for their children’s college education—also offers up some savings strategies that can help your children avoid amassing a mountain of debt along with their diplomas. That sounds like quite a gift indeed!

Crowdfunding for the Holiday Season

Crowdfunding—the concept of raising funds from a pool of outside investors or donors to finance everything from medical costs to new high-tech product launches to potato salad (I kid you not; Google it)—is all the rage these days. Many parents have felt that financing their children’s college education lies firmly on their shoulders—or their child’s in the form of a hefty student loan. The amount of debt many parents and students may have to bear can be staggering. We’ve all read the statistics about our student loan crisis. Americans have amassed a record-high $1.2 trillion in student loan debt,1 and about 60% of students who earned a bachelor’s degree in 2012–2013 from public and private nonprofit institutions graduated with debt averaging $27,300.2 More recent surveys have suggested this number has climbed even higher.

The problem has gotten so extreme that some new grads seem to be considering extreme measures to pay off their debt. According to one poll I saw recently, many such indebted individuals would actually sacrifice an organ to erase their student debt! I think the crowdfunding trend is a brilliant (and more sane) idea to help your children or grandchildren avoid a mountain of student loans. Now, I’m certainly not recommending you go on Kickstarter or GoFundMe or some other popular platform and plead your child’s case as a good potential return on investment—although that very well may be the case since we know individuals with college degrees tend to earn higher lifetime incomes than those without them. Rather, I would suggest that you probably already have a pool of family or friends who would be willing to help finance your child’s college education with a monetary gift this holiday season that could last much longer than the current hottest gadget or game.

The Importance of Saving Early—and Often

Saving for college is similar to the learning process we all go through as children. It cumulates with lots of little steps that take work over a long period of time! The desire to learn can be spurred by parents who read to their young children, and later, read with their older children. Getting them interested in school and stimulating their curiosity are essential steps that fuel a desire to learn—and eventually to become a future scholar. The same rationale that applies to early education applies to saving for college. To a young child, learning to read can seem overwhelming and even impossible at first, but breaking it down into individual letters and sounds is the first of many small steps toward the goal of finishing an entire book. In some ways, saving for college can be a similar exercise. The required sums may seem staggering, but even small contributions over time—maybe including the help of family and friends—can make a huge difference in the final outcome.

In 2014, the College Savings Foundation surveyed American families about how they were saving for future college costs (if at all).3 The survey revealed something very interesting. The families that were considered “successful” when it came to saving for college all used five common and simple strategies. Whether you are just getting started or are already saving, these five strategies can help with your college savings efforts:

1. Start Early

2. Invest Regularly

3. Ask Friends and Family to Help

4. Educate Yourself

5. Work with a Financial Advisor

Planning for the Future and the Power of the 529 Plan

Applying our crowdfunding idea (“Ask Friends and Family to Help” in the list above) can maximize potential educational savings over time. A savings vehicle called a 529 plan can be an ally in this pursuit. A 529 plan is a qualified tuition plan that can be sponsored by states, state agencies or educational institutions. These plans allow parents, grandparents as well as other family members and friends to make contributions for a designated beneficiary’s college costs. Money invested in 529 savings plans grows free of federal income tax when withdrawn for qualified higher education expenses such as tuition, books, and room and board. Depending on where you live, there may also be state tax benefits.4

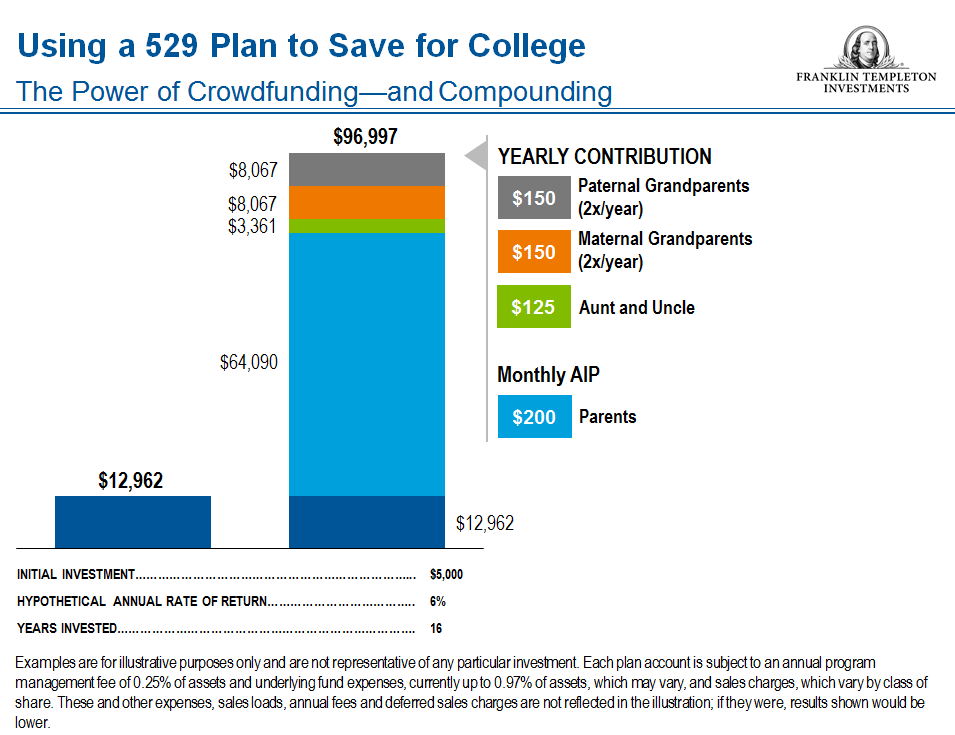

Let’s see how this approach works using a 529 college savings plan as our savings vehicle. As an example, parents set up a Franklin Templeton 529 College Savings Plan5 for their three-year-old son with an initial contribution of $5,000. Assuming a 6% hypothetical annual rate of return, after 16 years they could expect to see the account grow to $12,962 before fees, expenses and taxes.

Now consider the same situation, but the parents contribute $200 per month through an automatic investment plan (AIP). The beneficiary’s two sets of grandparents contribute $150 each birthday and $150 each holiday season. Finally, the beneficiary’s aunt and uncle commit to giving $125 each year for his birthday. After the same 16-year period, the amount in the account would balloon to $96,997, resulting in more than an $84,000 increase in the amount saved!

Saving for college may seem like an impossible task—the good news is you don’t have to do it alone.

Happy holidays—and good luck with your own college crowdfunding efforts!

Want to Learn More?

Watch our short video, “5 Strategies of College Savings Success,” to see more strategies that can help in the quest. Whether you are just getting started or have been saving for years, these are proven steps that can work for you.

Learn about 529 College Savings Plans at Franklin Templeton and talk to an advisor for savings ideas and strategies that are best for you and your family.

How are you saving for college? Join the discussion on our Facebook page.

What Are the Risks?

All investments involve risks, including potential loss of principal.

Investors should carefully consider college savings plan investment goals, risks, charges and expenses before investing. To obtain a disclosure document, which contains this and other information, talk to your financial advisor or call Franklin Templeton Distributors, Inc., the manager and underwriter for a 529 plan at (800) DIAL BEN®/(800) 342-5236 or visit franklintempleton.com. You should read the disclosure document carefully before investing and consider whether your, or the beneficiary’s, home state offers any state tax or other benefits that are only available for investments in its qualified tuition program.

_________________________________________

1 Source: New York Federal Reserve, data as of June 2015.

2 Source: The College Board, Trends in Higher Education.

3 Source: College Savings Foundation, “State of College Savings.”

4 It’s important to remember that, as with any investment, principal value may be lost, and investing in the plan does not guarantee admission to college or sufficient funds for college. There is no federal or state guarantee of investments in the plan.

5 Offered and administered by the New Jersey Higher Education Student Assistance Authority (HESAA); managed and distributed by Franklin Templeton Distributors, Inc. an affiliate of Franklin Resources, Inc., which operates as Franklin Templeton Investments. No federal or state guarantee. Principal value may be lost and investing in the plan does not guarantee admission to college or sufficient funds for college. Please refer to the Investor Handbook for more complete information. Examples are for illustrative purposes only and are not representative of any particular investment. Each plan account is subject to an annual program management fee of 0.25% of assets and underlying fund expenses, currently up to 0.97% of assets, which may vary, and sales charges, which vary by class of share. These and other expenses, sales loads, annual fees and deferred sales charges are not reflected in the illustration; if they were, results shown would be lower.

© Franklin Templeton Investments

© Franklin Templeton Investments