Japan’s Demographic Challenges Dampen Growth

Japan’s real gross domestic product (GDP) growth figures turned modestly negative during the second and third quarters of 2015 after strong real GDP growth in the first quarter. Although some market participants may see signs for concern, Michael Hasenstab, CIO of Templeton Global Macro, sees challenges but also much progress in Japan from its ongoing economic policies aimed at stoking inflation and strengthening growth. The Global Macro team has examined some of the long-term factors affecting economic conditions, notably how an aging population and shrinking labor force pose challenges for Japan’s economic aspirations. The team has identified reforms that it believes Japan will need to undertake to exit its multiple decades of deflation.

Read more about Japan and whether Hasenstab believes Prime Minister Shinzo Abe’s stimulus efforts (known as “Abenomics”) are working in Global Macro Shifts: Japan: Igniting Growth and Inflation.

Japan has embarked on an unprecedented economic policy shift to finally break out of nearly two decades of low growth and deflation. Whether or not the new strategy succeeds will have substantial implications for the global economic outlook.

In 2012, the administration of Prime Minister Shinzo Abe launched a comprehensive policy dubbed “Abenomics,” articulated in three “arrows.” Abenomics constitutes a true regime change and has already had a significant impact—but the road to sustainably higher growth and inflation is still long. It’s our view that the government, however, will need to boost efforts across key structural reform areas, notably on the labor market. Meanwhile, we expect the Bank of Japan (BOJ) to maintain an extremely easy monetary stance, possibly boosting quantitative and qualitative easing (QQE) further, resulting in a prolonged period of a weak(er) yen and low interest rates.

Japan’s Lost Decade(s)

After a prolonged period of extremely strong growth, Japan’s economy lost momentum in the 1970s. One reason was that Japan had by then exhausted the easy gains of the catching-up phase of growth, sustained by the quick and successful adaptation of imported technologies. Japan, however, also encountered two major headwinds, one being appreciation of the yen and the other being the acceleration of the elderly dependency ratio.

As the global fixed exchange-rate regime collapsed, the yen experienced two major waves of appreciation, and its value against the US dollar doubled. The currency weakened in the 1980s, but following the 1985 Plaza Accord it resumed a prolonged appreciation phase. Between 1970 and 1995, the yen’s real effective exchange rate appreciated by 150%.

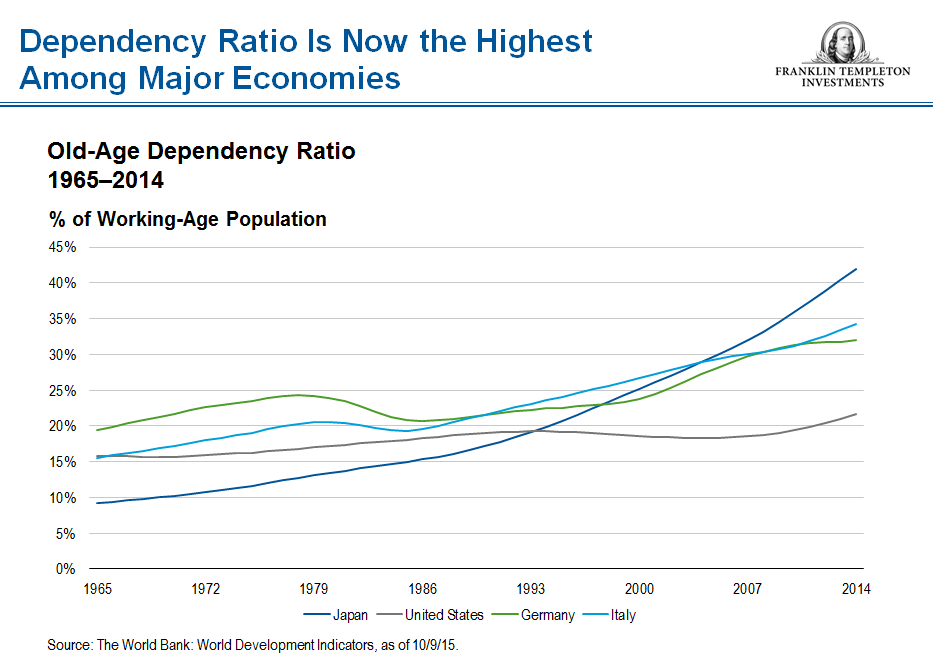

Hard as it is to believe today, in 1980 Japan had the lowest elderly dependency ratio (the ratio of retirement age population to working age population) in the G7.1 The pace of population aging then accelerated dramatically, and by 2005 its elderly dependency ratio had become the highest in the G7 and remained on a steep climbing path.

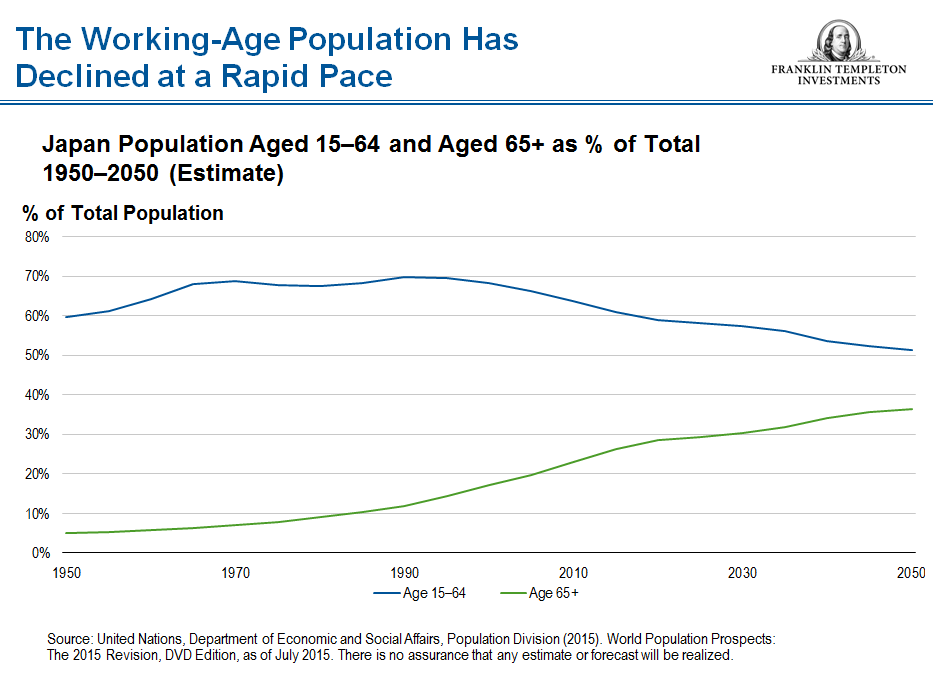

Demographics have played—and continue to play—a key role in holding back Japan’s growth performance. Japan’s population keeps aging at a rapid pace. In 1980, only 9% of Japan’s population was aged 65 or older; today it is over 26%; 20 years from now nearly one in three Japanese will be in this older age bracket. Conversely, the share of the Japanese population in the 15–64 age bracket peaked at nearly 70% two decades ago and has now declined to just over 60%; it will continue to decline until 40 years from now when only one Japanese in two will be of working age.2

Japan’s Shrinking Labor Force

The rapid pace of population aging has important implications for pension and health care expenditure. Most relevant to this part of our discussion, however, is the fact that it reduces the size of the available labor force. The Japanese government projects that in a favorable scenario (stronger growth and a rising participation rate), the labor force would shrink from 66.3 million in 2010 to 62.9 million by 2030, a loss of 3.4 million workers in 20 years. In an adverse scenario, without a pickup in growth or the participation rate, the reduction would amount to 9.5 million workers, lowering the labor force to just 56.8 million over the same period. Under the same adverse scenario, the government estimates that the number of people in employment would decline from 63.0 million in 2010 to just 54.5 million in 2030.3

The shrinking of the labor force is compounded by labor market inefficiencies, resulting in a duality between established and temporary workers, and by an apparent skills mismatch. In a recent paper, Ganelli and Miake (2015) note that Japan’s Beveridge curve has shifted to the right, so that the same unemployment rate is now associated with a higher level of job vacancies. The BOJ’s Tankan survey indicates that all companies are suffering from labor shortages, with small- and medium-sized enterprises particularly affected. A recent survey by the ManpowerGroup revealed that 81% of Japanese companies reported difficulties in filling jobs in 2014, by far the highest share among all countries surveyed, and more than twice the global average.4 Job vacancies as a percent of the labor force are also significantly higher than in many other advanced countries.5

The adverse demographics trend has been countered in part by a healthy pace of productivity growth. Growth in multifactor productivity has kept pace with other advanced economies such as the United States and Germany. In fact, following the global financial crisis (and abstracting from the recovery spike of 2010), the average growth rate of multifactor productivity in Japan has been the fourth-highest in the Organisation for Economic Co-operation and Development (OECD), well ahead of the United States and the United Kingdom.

Thanks to this healthy productivity performance, per capita growth in Japan has almost kept pace with other major advanced economies. During the period 1990–2014 (and excluding 1998, when Japan was hit by the Asian financial crisis), per capita gross domestic product (GDP) in local currency terms at constant prices has increased at an average pace of 1.1% in Japan, compared to 1.3% in the United States and 1.4% in Germany.6 Japan’s healthy productivity performance is both good and bad news. On the positive side, it shows that the combination of technological improvements and a well-educated labor force allows Japan’s economy to maintain a good degree of efficiency and competitiveness. On the other hand, however, it tells us that further productivity improvements can play only a limited role in boosting Japan’s overall GDP growth.

Wage Inflation: Making Progress

After nearly two decades of deflation, changing inflation expectations and wage-setting behavior is proving difficult, but Japan has been making progress in this area. In this year’s round of negotiations, companies have raised base salaries by 0.7%, significantly more than the 0.4% granted last year,7 though not enough to materially accelerate a virtuous spiral of higher wages and higher consumption.

Policymakers, including Abe and BOJ Governor Haruhiko Kuroda, have repeatedly called on companies to grant higher wage increases and to increase the share of employees hired on a permanent basis rather than on temporary contracts. As corporate profitability has improved, policymakers will continue to put pressure on the corporate sector to reduce its cash balances in favor of higher employment, wages and investment. Underlying conditions are improving: Labor market conditions have tightened further, with the unemployment rate dropping to 3.4% from 4.1% at the launch of Abenomics as the output gap has been closing. As a consequence, broader wage pressures are gradually increasing.

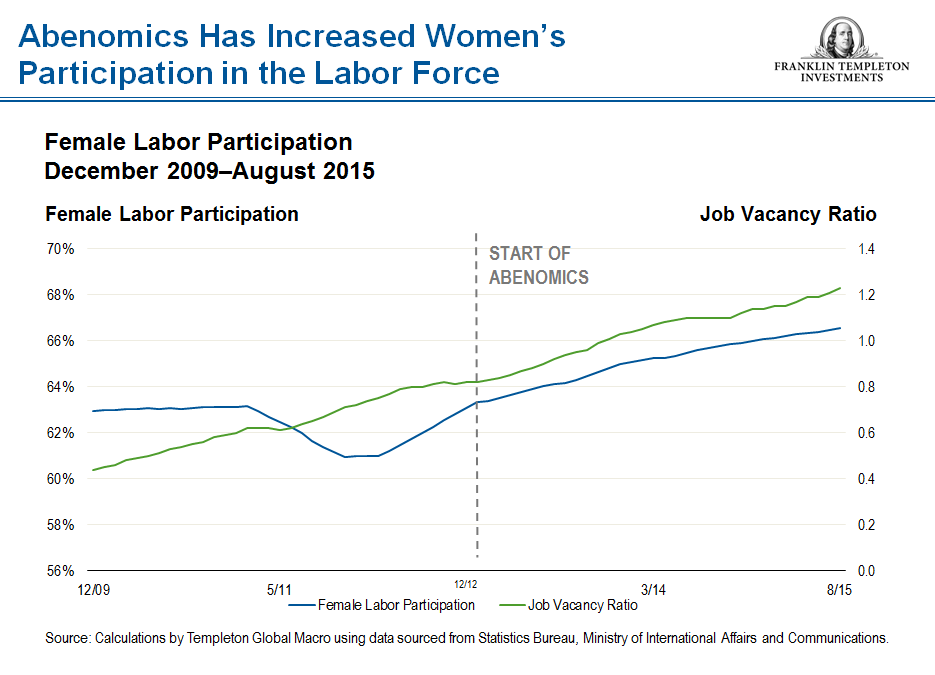

As discussed, Japan’s total factor productivity growth is already relatively high; while it could be boosted further, an acceleration in overall GDP growth will need to rely primarily on a boost to both labor and capital. Given the projected decline in the size of the labor force, the government’s first priority on the labor front has been to raise the female participation rate. The government has increased the number of available childcare facilities and the amount of cash transfers to families with children. The female labor force participation rate, which had increased from about 59% in 1994 to about 63% at the launch of Abenomics, has since climbed further to over 66%.

This constitutes important progress, but further steps are needed. The government could encourage a continued increase in female participation by deregulating childcare facilities, thus boosting their availability, and reviewing tax and social security benefits for households with full-time housewives. In addition, the government could take steps to make it more attractive for older workers to remain in employment. Given the projected aging of the population, raising the share of people who remain actively employed in the older age cohorts would have a positive impact on the overall size of the labor force, and it might contribute to reducing the pressure on the health care system. A third step to boost the labor force would be to relax current restrictions on immigration—although this remains one of the most politically controversial areas.

Finally, the government could consider further labor market reform measures to reduce the current duality between permanent and temporary contracts. Currently over 40% of the employed labor force has temporary contracts, with significantly lower salaries than workers with permanent contracts. Permanent contracts also come with far greater job security, with long-term employment essentially guaranteed. The ratio of temporary contracts has been steadily increasing to its current levels since 1985, when it stood at about 16%.8 Reducing this duality would increase labor market flexibility and mobility, and could therefore lead to a better allocation of human capital and raise labor productivity growth.

In our view, Japan’s policymakers have the right strategy in place and seem fully committed to carrying it out. While results so far have been mixed—partly due to adverse external circumstances—wage dynamics, inflation expectations and growth have been moving in the right direction. Both policies and economic indicators signal a break from the past, though the break so far is stronger for the latter than for the former.

Given the healthy productivity growth and the global competitiveness of Japanese corporates, further boosted by a weaker yen, we believe additional progress on both inflation and growth is likely as the global backdrop improves in 2016.

Michael Hasenstab’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties.

_____________________________________________________________________________

1 The Group of Seven (G7) refers to a forum of seven industrialized countries: France, Germany, Italy, Japan, the United States, the United Kingdom and Canada.

2 Source: United Nations Population Division, World Population Prospects: The 2015 Revision.

3 Source: Giovanni Ganelli and Naoko Miake, “Foreign Help Wanted: Easing Japan’s Labor Shortages,” IMF Working Paper, July 2015. There is no assurance that any estimate or forecast will be realized.

4 Source: ManpowerGroup, 2015 Talent Shortage Survey.

5 Source: Giovanni Ganelli and Naoko Miake, “Foreign Help Wanted: Easing Japan’s Labor Shortages,” IMF Working Paper, July 2015.

6 Source: Calculations by Templeton Global Macro using data sourced from International Monetary Fund, World Economic Outlook.

7 Source: As reported in The Wall Street Journal.

8 Source: Ministry of Internal Affairs and Communications, Labour Force Survey.

© Franklin Templeton Investments

© Franklin Templeton Investments