US monetary policy arrives at a pivotal turning point

Higher interest rates on corporate and government bonds loom ahead as the US Federal Reserve (Fed) plans to raise its policy rates gradually in 2016. These long-anticipated increases will be the most visible part of a set of actions intended to unwind the unconventional, ultra-accommodative policies implemented in response to the global financial crisis.

Other actions—to reduce the Fed’s holdings of US Treasury and mortgage-backed securities, for example—will likely be put off until well into 2016, at the earliest, as the US central bank monitors the economic and financial impacts of an increasingly higher federal funds rate target range.

On at least eight occasions in 2015, Fed Chair Janet Yellen stated that the timing and magnitude of the first policy-rate increase matters less than the trajectory—i.e., the magnitude, pace and end point—of subsequent increases. Nonetheless, the first rate increase has great symbolic and material importance in its own right.

The initial move matters symbolically

The first announced rate hike affirms to investors that all five of the preconditions the Federal Open Market Committee (FOMC) set for raising interest rates have been met; in that context, the policy action symbolizes that:

- Regulators have reasonable confidence that the safety and soundness of the banking and financial systems, as well as their ability to provide the credit that fuels economic growth, will not be impaired by the withdrawal of bank reserves and higher interest rates.

- The FOMC is convinced that the toolset used to manage reserves in the banking system has sufficient flexibility and precision to stabilize the federal funds rate within the range set by the FOMC.

- Slack in the US labor market largely has been removed, with the official U-3 unemployment rate approaching its full-employment level, the broader U-6 unemployment rate below its pre-crisis level and increases in real average hourly wages accelerating past 2% at an annual rate.

- The FOMC believes that US core inflation shows clear signs of rising to a 2% annualized rate, with inflation expectations anchoring at that level.

- US interest-rate increases appear unlikely to exacerbate underlying economic stresses elsewhere in the world, especially in emerging markets, to contribute to the disorderliness of international money and capital markets, or to intensify forces causing the US dollar to appreciate much further against both developed and emerging-market currencies.

An interest-rate increase without all of the preconditions in the fold jeopardizes the Fed’s credibility and, by extension, the policymaker’s ability to achieve its goals.

A policy-rate increase also symbolizes that the US economy is strong enough to sustain growth at its potential rate and maintain price stability with less of a push from monetary policy.

Accordingly, the first rate hike signals that policymakers have reached a comfort level with the trend and cyclical performance of a full spectrum of economic and financial data and information, including hundreds of leading, coincident and lagging indicators of economic well-being; the level of real short-term interest rates; liquidity characteristics of critical asset markets; the fiscal condition of localities, states and the federal government; the systemic implications of global geopolitical developments; and the composition and impacts of monetary policies implemented by non-US central banks.

In addition, an increase in US policy rates while central banks in other economies implement quantitative easing and ultra-low interest rate policies symbolizes the “divergent paths” between US and non-US monetary policies.

Anticipation results in asset repricing

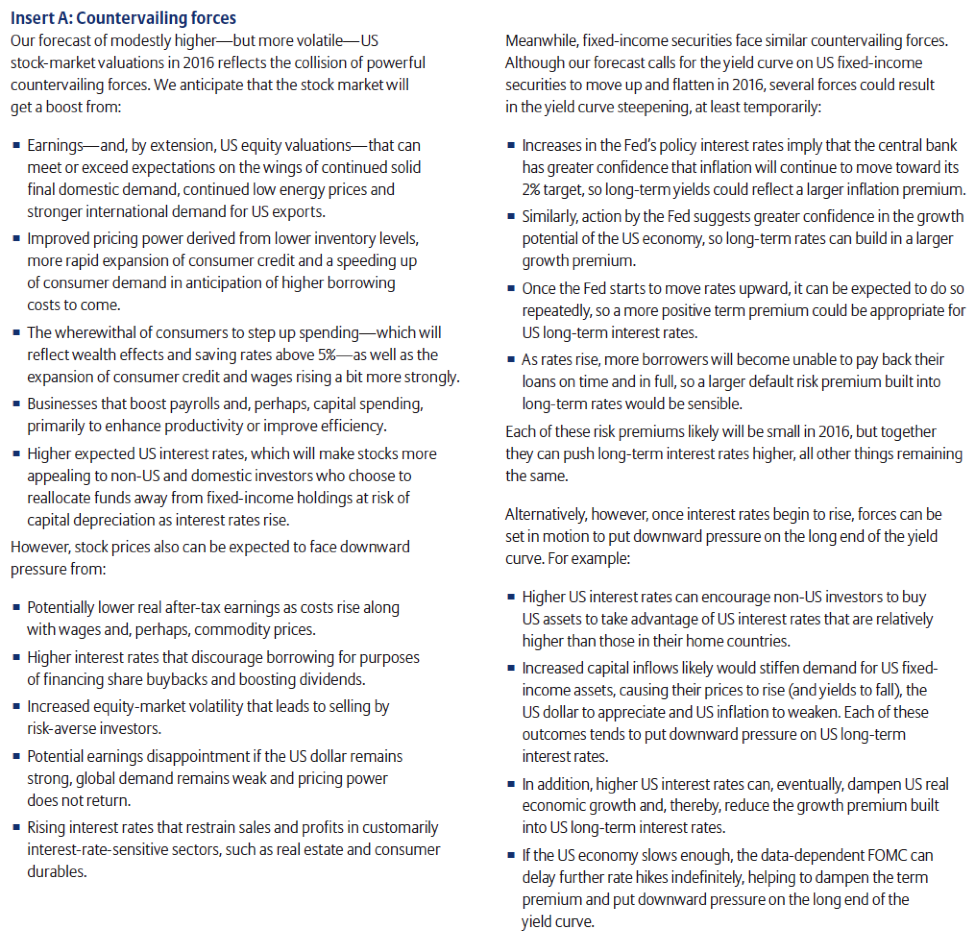

Yet the impacts of the first US interest rate hike go well beyond symbolism. We anticipate that even a token 25-basis-point increase in the federal funds rate target range sets in motion adjustments in the US economy and asset markets enriched until this fall by the expectation that US policy rate-increase will remain at, or near, 0% well into the future. (See Insert A.)

Official Fed communications helped to foster such enrichment. In the absence of uncommon forecast accuracy, the FOMC could not possibly know in advance how aggressively the rate-increase cycle would proceed. Consequently, the Committee shied away from stating when the first rate increase would take place, how large the increase would be, how frequently future rate increases would occur and how high the federal funds rate target range would be lifted.

By reiterating the data-dependency of its policy decisions, the FOMC affirms that its actions remain contingent upon the strength of economic and financial data at the time each FOMC meeting takes place. This approach, however, reinforces lingering uncertainty about the path of monetary policy and its expected implications for valuations within and among asset classes.

Nonetheless, widespread anticipation of the first rate hike led in November 2015 to the repricing of fixed-income securities and equities, and to additional appreciation of the foreign-exchange value of the US dollar. Major stock indexes rose about 1% for the month, while yields on the US Treasury 2-year and 10-year notes climbed 20 basis points and 7 basis points, respectively, though the 10-year was up as much as 21 basis points by November 9.

Anticipation of an imminent policy rate hike intensified following the November 18 release of the minutes of the October FOMC meeting. According to the minutes, Committee members generally agreed that a December rate hike would “be appropriate” and that the pace of future rate increases would be “gradual.”

Further, a stream of stronger inflation and labor-market reports, as well as renewed calm in China’s financial markets, brought the five rate-hike preconditions closer to fulfillment and boosted investor confidence. In response, the probability of a December announcement of a policy-rate increase—implied from the federal funds futures market—rose to roughly 65%–75%.

Conditions were usually strong at the start of rate-hike cycles

During the first half of 2016, economic and financial markets likely will continue to be buffeted by countervailing forces, some tending to push securities prices lower, others working in the opposite direction. In that context, Allianz Global Investors anticipates that major US stock indexes will experience only a small increase in valuations in 2016 compared with year-end 2015. We also expect US short-term interest rates to move upward in lock-step with the federal funds target range, with long-term interest rates up by less.

As the Fed embarks on an anticipated series of interest-rate increases over the next year or so, attention turns naturally to comparisons with, and lessons learned from, previous rate-hike cycles. This time around, the Fed’s task will be complicated by extreme conditions, even bubbles, in some markets; by the most open and internationally integrated markets ever; and by a general lack of global and US economic momentum. Since no two rate-hike cycles have the same characteristics, however, comparisons can only suggest, without being predictive, what may lie ahead.

The economic precursors

The forthcoming cycle will take place during the slowest, but longest, US cyclical recovery and expansion in more than 40 years—one that has lasted approximately 26 quarters. It took 14 of those quarters for the US economy just to recover all of the output lost in the Great Recession, compared with the typical post-World War II recovery period of 5 to 8 quarters.

Yet growth in US real domestic final demand in 2014 and year-to-date 2015 has been reasonably strong, averaging more than 3% at an annual rate. Furthermore, the current U-3 unemployment rate of approximately 5% is lower than it was at the start of five of the last six rate-hike cycles, with the exception being 1998—the midst of the telecom-media-technology bubble. (See Exhibit 1.)

Inflation is also lower than it was at the start of each of the previous six cycles; during this time, the low for US core inflation occurred, on average, roughly two months after the Fed’s first move. (See Exhibit 2.)

This time around, real economic growth in the euro zone is moderately slower than it was before the Fed’s 2004 and 1994 rate increases. Japan’s economy is weaker than it was in 2004, but healthier than it was in 1994. China continues to grow at a moderate—albeit much slower—pace, dampening growth in other emerging-market economies, particularly commodity-exporting countries. However, conditions in some emerging economies before earlier Fed rate increases, like those in Mexico in the early 1980s and mid-1990s, were considerably weaker than they are now.

Presently, the foreign-exchange value of the US dollar is trending upward against a basket of major non-US currencies. US dollar strength, as well as that of the early 1980s, contrasts with trend weakness in the currency prior to most other rate-hike cycles. Unlike periods preceding prior Fed rate increases, the strength of the US dollar in 2015 has been fueled partially by expectations that the Fed would hike rates while the ECB, Bank of Japan and several other central banks continue quantitative easing or push interest rates even lower.

Financial market precursors

Never before has the policy disparity between the Fed and non-US developed-market central banks been as extreme as it is today.

Gradually higher expected US policy rates in 2016 and 2017 shine a spotlight on the six interest-rate reductions in 2015 by the People’s Bank of China; on extensive quantitative easing by the European Central Bank and the Bank of Japan; on the negative policy interest rates in the euro zone, Denmark, Sweden and Switzerland; and on anti-austerity movements in Portugal, Greece and elsewhere.

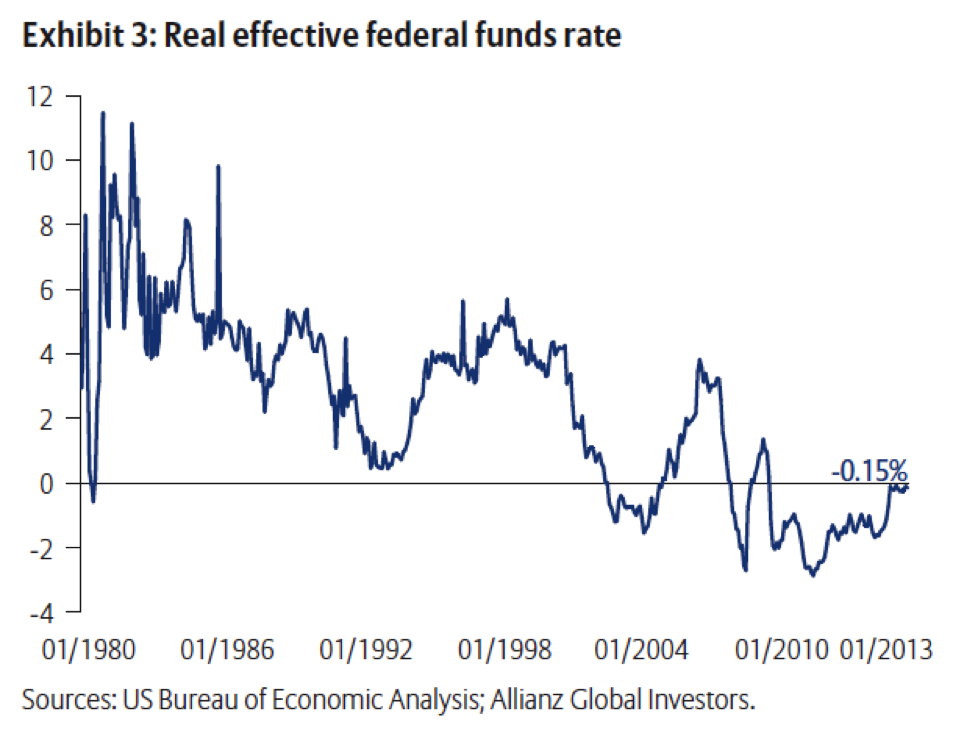

The first move by the Fed comes about under mixed financial-market conditions. Monetary-policy accommodation remains extreme, with the real federal funds rate negative and the Fed’s asset holdings exceeding $4 trillion. Meanwhile, equity market indexes are up modestly over the past year, though a bit less robustly with a one-year look-back than at the start of previous rate-hike cycles. (See Exhibit 3.)

However, growth in the revenues and earnings of companies in the S&P 500 Index remains weak. Indeed, earnings from production, as measured by the National Income and Product Accounts, are even weaker than the more inclusive earnings reported on an accounting basis. Revenues declined year-over-year throughout 2015—by 2.9% in the first quarter, 3.4% in the second and an estimated 3.9% in the third. The last time year-over-year revenues declined in two consecutive quarters—let alone three—was 2009.

Given this pattern, US corporate earnings growth, on an accounting basis, dropped in 2015—by 0.7% in the second quarter and 1.6% in the third. Companies in non-US countries struggled, too—despite both the strong US dollar and relative weakness in their respective currencies— as global deflationary pressures and generally lackluster consumer demand put stress on revenue growth. In 2015, the MSCI World Index dropped two quarters in a row—the second and third quarters—for the first time since 1993 in a non-recession period.

Rate-hike cycles typically have not crimped growth and valuations

The six rate-hike cycles launched by the Fed since 1983 lasted an average of 414 days and raised policy rates by an average of 281 basis points. During each of these cycles, the domestic supply of money and availability of credit remained abundant. (See Exhibit 4.)

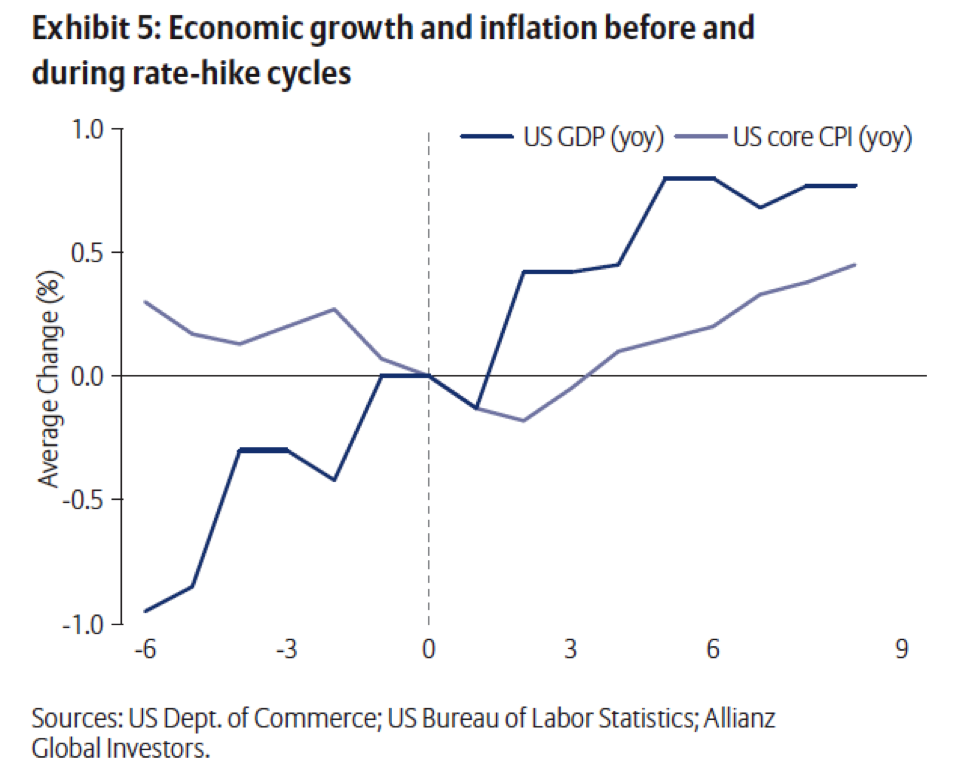

Only when policy-rate increases and excessive monetary tightening resulted in tight money and credit conditions—as was the case in 1989, 2000 and 2006—has the economy suffered; growth remained healthy following the 1983–1984 and 1994 rate increases. (See Exhibits 5 and 6.)

Average asset-market performance over these six previous rate-hike cycles was mixed, though generally positive, with commodities and emerging-market equities—which are typically highly correlated with each other—leading the way:

- Commodities over 5 cycles: +25.2%

- Emerging-market equities over 4 cycles: +18.9%

- US equities over 6 cycles: +9.9%

- US money-market mutual funds over 6 cycles: +7.0%

- US TIPS over 2 cycles: +6.6%

- US high yield over 6 cycles: +6.6%

- US Treasuries over 6 cycles: +5.1%

- US investment-grade corporate bonds over 6 cycles: +1.9%

- Global government bonds over 5 cycles: +1.9%

(See Exhibit 7. Time periods shown are based on the inception of each asset class’s underlying benchmark index.)

Financial-market performance over the 1994–1995 rate-hike cycle proved to be extremely challenging. Both the timing and magnitude of the Fed’s actions at the time surprised the financial markets and triggered negative responses in almost all asset classes. During the 1994-1995 time period, only US money-market instruments recorded gains (+4.6%), with US high-yield bonds down 1.2%, commodities down 1.4%, US equities down 2.1%, global equities down 6.6% and emerging-market equities down 20.6%. At one point, US equities were down about 9%.

This time around, much improved and greatly expanded communications from the Fed likely will promote more orderly performance across markets.

Equity market performance

During most rate-hike cycles since 1983, US stock markets moved up and down, ending either roughly unchanged or up—holding onto most, if not all, of their pre-rate increase gains. (See Exhibit 8.)

International stock trends were a bit more mixed. Developed nations’ stock markets were flat or rose during every Fed rate-increase cycle since 1983. The exception was 1994, when modest declines followed significant gains in the prior year.

Japan’s stock market rose sharply during all rate-hike cycles since 1983 except in 1994, when economic stagnation, threats of deflation and a largely insolvent banking system contributed to an 8.3% decline in the Nikkei, a one-half retracement of its rise in the prior year.

European stocks were more mixed during these cycles, increasing during 1983–1984 and 2004-2006, moving up and down for no gain during 1987–1989, and falling 6.7% during 1994, a fraction of their robust 29.7% rise in the prior year.

Most emerging nations’ stock markets also rose during recent rate-hike cycles. Emerging-market stocks tended to soar during the 1987-1989 and 2004–2006 cycles. The sharp decline in emerging-market stocks during 1994 largely reflected crises in Mexico and Brazil.

Fixed-income market performance

The starting points and trajectories of interest-rate movements varied during the monetary tightening cycles that have occurred since 1983. However, as the Fed begins the latest round of rate increases— kicking off another rate-hike cycle—the real federal funds rate will be deeply negative, a reflection of uncommonly accommodative US monetary conditions.

When the Fed began raising rates in 2004 and 1994, the real federal funds rate was negative or very low; inflation-adjusted yields on 10-year Treasury notes were around 3%. At the start of the 1987 and 1999 cycles, the real federal funds rate was close to average, at 2.3% and 2.6%, respectively, and it was very high, at 5.1%, in spring 1983. (See Exhibit 9.)

Inflation-adjusted bond yields exceeded 3% at the beginning of every Fed rate-increase cycle since 1983 (they were 7% in spring 1983). However, US bond yields rose to varying degrees during every cycle— but by less than short-term rates, generating flatter yield curves. The yield curve was inverted at the end of the cycles of 2004–2006, 1999– 2000 and 1987–1989. A recession followed each of these yield-curve inversions. During periods when rates increased sharply and rapidly, longer-duration indexes underperformed more noticeably, as higher yields could not offset the steeper interest-rate-driven declines in market prices.

However, when rates rose over a longer period of time and in a more measured fashion—as in the June 2003 to June 2006 period—the greater interest income earned over a longer period of time offset the negative price movements. Higher-yielding strategies tended to outperform lower-yielding strategies with comparable maturities.

Currency market performance

Generally, Fed rate-increase cycles did not tend to interrupt the longer trends in the US dollar versus major currencies—except in 1994, when the Fed’s rate increases were a catalyst for the ensuing US dollar strength.

In fact, during the six rate-hike cycles since 1983, the dollar depreciated versus major currencies about as frequently as it appreciated. Except for the 2004–2006 cycle, the US dollar appreciated versus most emerging-market currencies—in some instances significantly when troubled nations faced crises.

The US dollar’s mixed performance over past rate-hike cycles reminds us not to assume automatically that it will appreciate versus all currencies. Since the early 1980s, the dollar has tended to move in long, high-amplitude waves against major currency indexes that, at times, defied the expected outcome following policy-rate increases. Keep in mind, as well, that appreciation of the dollar does not necessarily hurt the US economy. US exports remained strong during all prior rate-increase cycles, even during the strong dollar appreciation of the early 1980s. That outcome reflected the healthy fiscal policy fundamentals and the robust US and world economies that overcame the impacts of the dollar’s upward adjustment.

Critics of the Fed seek to curtail its independence

The unwinding of the current ultra-accommodative monetary conditions and unprecedented low interest rates likely will result in greater financial-market volatility and uncertainty. In this environment, critics of the Fed’s unconventional responses to the global financial crisis and the Great Recession—and, more importantly, their outcomes and consequences—can be expected to push for changes in monetary policy formulation, implementation and communication. (See Exhibit 10.)

Recently, several proposals have gained traction to restrict the monetary policy independence of the Fed. Such proposals are not new: Throughout the past half century, individual members of Congress have sponsored or co-sponsored bills intended to gain fuller disclosure of the Fed’s monetary policy decision-making process and the daily implementation of the FOMC’s policy directive by the New York Fed.

Other proposals have attempted to redefine the FOMC’s dual mandate or hold FOMC members personally accountable for economic outcomes.

Whether from Democrats or Republicans—from Representatives Wright Patman in the 1960s and 1970s, Henry Gonzalez in the 1980s and 1990s, and Rand Paul and others today—all such efforts have failed to become law. Typical proposals to reform the Fed would subject the policymakers to political pressure and blur the line between monetary and fiscal policy. Yet theory and evidence from all over the world suggest that more independent central banks tend to produce superior outcomes, such as warding off inflationary biases that could result from political pressure to boost output in the short run—for example, before an election.

Nonetheless, in November 2015, the House of Representatives passed legislation labeled the “Audit the Fed Act” that would subject the Fed to unlimited Congressional policy audits while also requiring the monetary authority to adopt a rules-based approach to monetary policy implementation.5 Such legislation aims to restrict the Fed’s instrument independence, departing from the modern governance structure that characterizes leading central banks around the world.

In so doing, the bill would roll back a cornerstone of US Federal Reserve independence in place since the Full Employment and Balanced Growth Act of 1978 (the “Humphrey-Hawkins Act”) exempted monetary-policy implementation from review by the General Accounting Office (GAO), now the Government Accountability Office. (For decades, the GAO has conducted financial audits of the operations of the Reserve Banks—and it continues to do so.) Humphrey-Hawkins granted independence to the Fed to use whichever instruments it deemed necessary to achieve its goals.

By also requiring the Board of Governors and the FOMC to report their plans directly to Congress at least semi-annually, Humphrey-Hawkins put in place a mechanism for holding the Fed accountable for meeting its statutory mandate. As transparency expanded, monetary-policy effectiveness also improved, as enhanced communication helped to clarify the Committee’s policy intentions and guided the public’s expectations. (See Insert B.)

Like other central banks, the Fed does retain some matters for private discussions. These discussions often contain market-sensitive information and may, by necessity, involve frank assessments of market- or even firm-specific conditions as well as unconventional ideas for dealing with evolving economic situations.

The low-inflation challenge to central-bank independence

The Fed’s basic governance structure, which was set up in the late 1970s, strove to monitor and encourage the central bank’s pursuit of its legislated monetary-policy mandates. An aggressive and successful campaign to bring down inflation followed.

The current rate of consumer price inflation remains below the FOMC’s objective of 2% annualized, forcing the central bank to consider the impacts of deflationary, rather than inflationary, forces. Although low inflation makes the more typical inflationary bias less of an immediate concern, the effects of political interference in monetary policy remains as valid when inflation is too low as it does when inflation is too high. That’s because politicians with relatively frequent election cycles seek more immediate economic outcomes than the FOMC pursues when it makes monetary-policy decisions.

The anchoring of inflation expectations has been a hard-fought product of the disinflation of the 1980s and subsequent Fed policies. Today, even with low inflation, the balance of evidence suggests that survey-based measures of longer-term inflation expectations remain fairly steady and consistent with the Fed’s objective.

Unconventional policy responses and the threat to independence

The existing governance framework under which the Fed operates has allowed the FOMC to respond to dramatic changes in the economic environment over the past 20 years.

In particular, during the Great Recession, instrument independence afforded the FOMC the flexibility needed to develop new strategies, tactics and tools to address the extraordinary challenges it faced in pursuing its dual mandate. However, legislative proposals like the Audit the Fed Act appear to be motivated by the belief that the Fed’s response during the crisis was somehow ineffective or even counter-productive.

It is impossible to know with certainty how the US economy and financial system might have weathered the global financial crisis in the absence of unconventional actions by the Fed. What is clear is that Fed’s response was a carefully considered exercise of instrument independence put forth in light of the Congressional mandate to which it is held accountable.

What is debatable, however, is the longevity of interest rates kept at, or near, their zero bound even as the economy and financial system strengthened; the benefits and costs of holding nearly $4.5 trillion in US Treasury and mortgage-backed securities on the Fed’s balance sheet; and the implications of sustained monetary accommodation on asset values, income distribution and investor risk preferences.

Financial stability

In the post-global-financial-crisis period, central banks typically are tasked with responsibilities that go well beyond a single inflation mandate or a dual mandate of price stability and full employment. Modern central banks also must preserve or contribute to financial stability. These responsibilities have received far more emphasis following the financial crisis and are at the heart of the proposals to challenge central-bank independence.

That’s because in the face of an incipient bubble growing in, for example, the housing sector, central bankers turn first to macroprudential instruments—such as constraints on the loan-to-value ratio or the debt-service-to-income ratio of borrowers—to bring markets back in line with fundamentals.6 However, doing so affects particular sectors of the population that are politically important, such as homeowners. Consequently, political authorities can be expected to continue to push for a larger role in setting and implementing monetary policy.

Presidents have growing market influence

As the presidential nominating process continues, some investors will point increasingly to so-called “presidential election cycles”—the observation that stock prices tend to rise as a presidential election approaches and fall the first year after Inauguration Day. Strong proponents of this observation even try to time stock sales and purchases to take advantage of this seemingly recurrent pattern. Upon careful analysis of our own, however, we have concluded that election cycles are more coincidental than predictive. Like other attempts to time the market, investing based on proximity to Election Day results in returns inferior to those achieved by long-term investors. In the end, asset allocation and diversification matter much more than calendars.

However, it would be a mistake to conclude that presidents don’t matter to economic and financial markets simply because presidential-election cycles have little statistical validity. These election cycles may be more coincidental than actual, but presidential leadership is not.

For that reason, major-party candidates this year have taken stands on headline issues they believe play to their political philosophies and partisan strengths. Headline issues set the candidates apart from one another in opinion polls and keep the respective campaigns “on message.”

Yet presidential influence on the economy and financial markets goes well beyond headline issues. Evolution of presidential powers over many decades has stretched the impact of the White House well beyond narrow Constitutional mandates. Exercise of these powers has created reliance on the vice president, cabinet members, advisors, councils and a sizeable staff in ways unforeseen only decades ago. As a result, elections bring to power an administration rather than just a candidate.

This year, Republican presidential candidates, especially, have offered competing tax-reform plans that go well beyond their party’s previous platforms—and all but ensure that the issue will play a central role in the November 2016 general election.

Each of these plans has at least one bold reform proposal that would mark a dramatic departure from the way in which the United States has collected taxes since 1954. These proposals seek to produce big economic gains by increasing the tax advantages for saving and investing.

Proposals by Democratic candidates mainly address adjustments of marginal tax rates and the reduction or elimination of the capital gains tax preference in order to raise the effective average tax rate on upper-income taxpayers and reduce it for others. Other Democratic proposals back additional taxes on upper-income taxpayers to shore up the Social Security system, and favor a tax credit to help individuals pay out-of-pocket health care costs. (See Insert C.)

Focusing on taxes typically resonates well with US voters. Each of the last three presidents ran, in part, on a tax plan, and each got much of it implemented by the end of his first term. Beyond tax reform, how else then does a president influence the economy and markets? Below are 15 ways that lead to one logical conclusion: From a wealth-management and financial-planning perspective, the selection of a president can have far-reaching effects.

The president serves as the nation’s principal fiscal agent

Each February, the president submits to Congress the next fiscal year’s budget proposal. This detailed document outlines the administration’s priorities and details all of the federal government’s proposed expenditures and revenues. Although little of the president’s proposal makes its way through Congress as submitted, it does set the tone for debate and action among the legislators. A key sentence that has appeared in every year’s proposal for about half a century sums up the budget’s significance: “The economy affects the budget and the budget affects the economy.”

The president sets the direction for discretionary fiscal policy

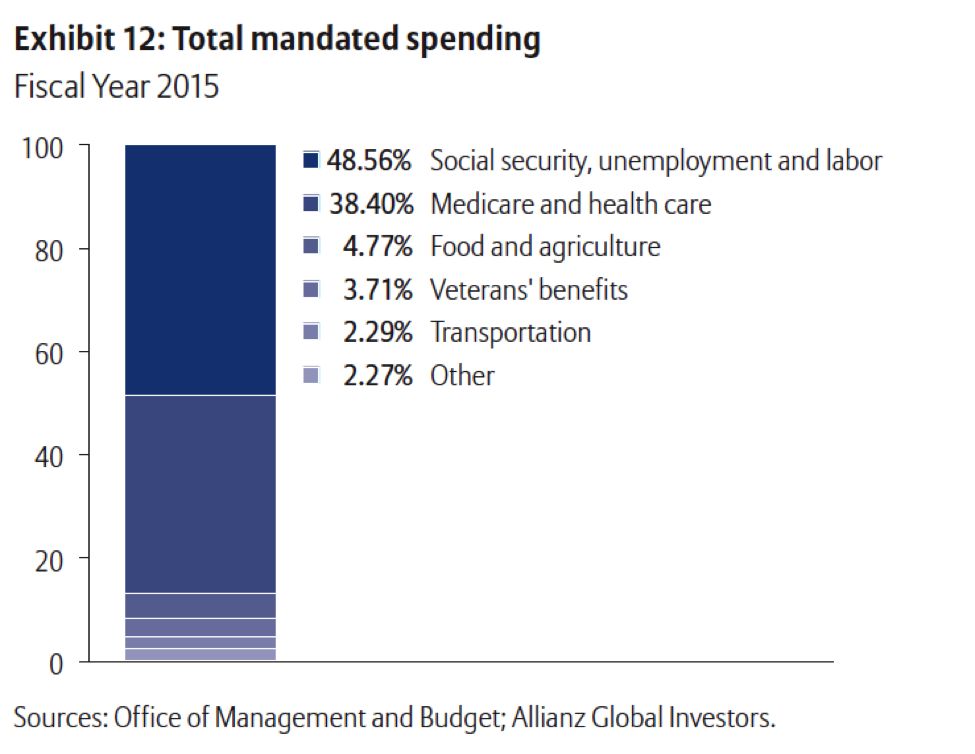

To carry out its policies, the president can propose changes in government spending and taxes that either affect the whole economy or target individual groups and industries. These actions, at the “discretion” of the administration, can focus on either a temporary, or cyclical, issue (like a stimulus package) or a long-term issue not addressed directly in the federal budget (such as health care reform). (See Exhibits 11, 12 and 13.)

The president forges compromises among legislators, leading to passage of key legislation

As chief executive, the president alternately twists arms and mildly cajoles legislators in order to break stalemates and move legislation along toward passage. Without White House leadership, key economic and financial legislation only infrequently works its way through Congress.

The president appoints officials to key government positions

The people the president selects for key positions in the Executive Branch have a profound influence on the direction and implementation of fiscal, monetary, trade, regulatory, anti-trust and other policies. Not only do these appointees help to shape and implement policy, but they also direct sizeable departments with wide-ranging responsibilities and significant budgets.

The president nominates Supreme Court justices and members of the Federal Reserve Board of Governors

The president has a Constitutional requirement to nominate justices to the Supreme Court, subject to confirmation by the US Senate. Decisions rendered by the Supreme Court can affect commerce, industry and finance for decades to come. Similarly, the president nominates Fed governors whose monetary-policy decisions and financial institution supervision set conditions that help to shape the US economic and financial environment.

The president serves as Commander-in-Chief

Decisions related to military operations far transcend the size and composition of the defense budget. Enormous amounts of human, physical and financial resources go into planning, implementing and recovering from military operations. Operations related to national defense and homeland security go hand-in-hand with foreign relations in setting the terms under which business and financial institutions function domestically and abroad. In addition, the scale of defense outlays, veterans’ benefits and military pensions forces the president to make difficult judgments about national priorities.

Military spending can have profound regional economic impact depending on the composition of procurement, the location of bases and ports, and the private-sector services purchased. Regional economic development and expansion often depends on critical links between academic institutions, traditional manufacturing and high-tech companies, as well as the Departments of Defense and Homeland Security.

The president links economic policy to foreign policy

Administrations increasingly use a wide range of economic, trade, regulatory and other policies as part of a broader effort to achieve foreign policy goals. For example, sanctions imposed on Syria, North Korea, Russia and Iran—which were intended to damage their economies in response to military threats or human rights violations—curtailed the import and export of goods and services, affected capital flows between financial institutions and markets, and reduced the flow of oil and other critical commodities.

The president establishes bilateral or multilateral trade relations with other countries

Trade relations help to establish markets that US companies can export to, and they open the United States to imports of goods, services and resources from abroad. Agreements such as the recent Trans-Pacific Partnership and the North America Free Trade Agreement epitomize the kind of multilateral agreements that presidents can establish in an attempt to stimulate freer trade. Alternatively, the president’s administration can set up or reduce tariffs and other trade barriers, and impose or lift trade sanctions against other countries. These policies, along with the administration’s broader economic policies, may also have a temporary impact on the US dollar exchange rate.

The president implements a national energy policy

Since the Carter administration, especially, each presidential administration has taken a different stance on key energy issues. These include deregulation and pricing, exploration and production, green energy initiatives, hydraulic fracking, the granting of offshore drilling leases and standards for the use of clean coal.

Proposals for energy tax credits and other incentives to reduce the use of fossil fuels or convert to green energy alternatives typically emanate from the White House. Through the Department of Energy, the administration also sets standards for expected miles per gallon performance by fleets of cars and the potential location and construction of pipelines. In addition, the president determines the conditions under which gasoline stored in the Strategic Petroleum Reserve will be put on the market for sale.

The president makes and enforces environmental policies

Compliance with environmental regulations affects the cost of doing business and, in some cases, where businesses choose to locate. Such compliance also affects the quality and availability of certain goods, services and resources and, thus, their prices. In addition, environmental policies also tend to favor certain industries or companies over others and thereby influence the allocation of resources and the composition of output. Indirectly, these policies help improve public health and safety, with positive implications for worker performance, worker productivity and the cost of medical care.

The president sets the tone for immigration policy

The scope and scale of immigration policy affects the quantity, availability and quality of labor across numerous industries among a range of occupations. In addition, immigration policy affects the economic and fiscal well-being of target-marketing and, by extension, ways to culturally complement growing discretionary and nondiscretionary consumer demand.

The president launches big-idea initiatives that shape entrepreneurship, research & development, and regional economic development

Establishing infrastructure to handle the demands created by big-idea initiatives helps create targeted economic stimulus and shifts resources, research & development, and the mix of innovations. For example, in 1961, when President Kennedy set a goal to land an astronaut on the moon before 1970, he set in motion many forces that reshaped the US economy for decades. Similarly, the pledge by several presidents to make the United States energy self-sufficient has redirected exploration and production companies, and led to workers migrating to the locations where drilling takes place.

The president influences the size of federal agencies

Each federal agency has a budget that covers not only goods, services and resources, but the number of government employees, the compensation they receive and the size of their pensions. In the 2010–2012 period, for example, federal government job cuts played a major role in raising the US unemployment rate. Government agencies also buy about 20% of all goods and services produced in the United States each year.

The president determines the scale and scope of services provided at the federal level

To the extent permitted by law, the administration may shift some of its responsibilities onto the states and localities. Historically, this has resulted in a smaller federal role in the provision of public assistance. Alternatively, the federal government may assume certain roles customarily played by the states and localities—such as maintaining local highways and other critical infrastructure.

The president provides marketplace oversight and enforcement through government regulatory agencies

Each administration has discretion over the scope of activities it will regulate vigorously and the magnitude of its enforcement actions. An action—such as the merger of two companies—that is approved by regulators during one administration may not be approved during a different administration.

The president issues declarations of disaster relief

During and after catastrophic events, certain geographic areas may be granted emergency relief in the form of technical assistance, direct funding, low-interest loans and other measures to help with cleanup and recovery. The magnitude and scope of such relief come at the discretion of the administration.

Presidents and asset allocations

In light of all the ways that presidents matter to markets, some investors may decide to adjust the holdings in their portfolios. We do not favor such a step. Instead, we believe that asset allocations based on the individual goals, time horizons and circumstances of investors, not the occupant of the Oval Office, provide the best chance of earning targeted rates of return. In fact, we know of no better way to protect the totality of the financial interests of investors than to take a comprehensive, coordinated, long-term approach to financial planning and individualized wealth management. Such an approach is the hallmark of our philosophy.

Expected outcomes of the policy mix feel tepid

Allianz Global Investors projects real gross domestic product (GDP) to grow in 2016 at around a 2.5% annual rate—approximately the same rate as 2015. Continued softness in energy prices—accompanied by increased employment and a bit more wage growth—likely will contribute to solid gains in domestic demand. Export weakness— reflecting strength in the US dollar and cyclical malaise among major trading partners—may partially offset the expected domestic demand strength. We will continue to monitor quarterly changes in inventories, as these changes will disproportionately reflect and affect the pace of economic activities. We also anticipate that the real federal funds rate will remain negative during initial policy-rate increases, maintaining extreme monetary accommodation. With US banks well-capitalized and credit availability ample at still-favorable interest rates, household and business credit can be expected to expand further. Even when the real federal funds rate becomes positive, perhaps by mid-year 2016, it will remain below its natural rate and appears unlikely to curtail growth materially. Inflation likely will drift up over the course of 2016. We expect annualized increases in the overall personal consumption expenditure (PCE) deflator to inch up by early 2016 as temporary effects of very low oil prices begin to dissipate; the core PCE deflator will drift up slowly as well.

At the same time, the core consumer price index, with different weightings than the PCE deflator, can be expected to rise slowly, but persistently, before the end of 2016. Inflation will remain relatively modest until nominal GDP accelerates above its recent 3.75%–4.00% range and creates an environment conducive to higher wages and product prices.

We anticipate an initially slow rise in bond yields. Yields will be constrained by persistently low inflation expectations; by market expectations, which will be reinforced by official FOMC communications, that the Fed will raise rates only gradually; and by capital inflows from non-US countries as investors pursue the relatively higher inflation-adjusted yields on US bonds. Eventually, bond yields can be expected to rise, with the 10-year Treasury note exceeding 3% by year-end 2016.

With valuations of US equities somewhat stretched as the end of 2015 approaches, we will monitor corporate profits closely, since profits will be a key to 2016 stock-market performance. Over prior Fed rate-hike cycles, rising profits supported healthy stock markets as rising rates pushed down price-to-earnings multiples.

Today’s profits are strong both in absolute terms and relative to GDP, but they stopped growing in 2014. Higher operating costs and the negative impact of the stronger dollar on US multinational firms struck the bottom line. Accordingly, renewed acceleration in real economic growth may be needed to spur profit gains and a healthy stock market. Given our forecast of renewed real GDP growth in 2016 at roughly this year’s pace, we anticipate that the S&P 500 Index will rise slightly, or even fail to record a gain, in 2016.

Various countervailing forces can be expected to impact the 2016 outlook for the US dollar. We expect the US dollar to appreciate when the Fed first raises rates and to strengthen further subsequently. Perhaps in the second half of 2016, the US dollar may start to depreciate slowly, as Europe’s economy, especially, picks up steam. Favoring the US dollar, the Fed’s policy-rate increases will highlight its diverging monetary policy versus the European Central Bank and the Bank of Japan. With US inflation-adjusted bond yields much higher than those in Germany and Japan in particular, US assets can be expected to be in demand, generating capital flows to the United States and solid demand for the US dollar.

However, the euro and yen’s already significant depreciation has improved their alignment with economic fundamentals. In addition, euro-zone economies are strengthening and have a combined current-account surplus that exceeds 3% of GDP. Japan’s current-account surplus also exceeds 3% of GDP and domestic creditors fund nearly all of Japan’s large debt—which measures approximately 210% of GDP. Emerging-market currencies may be vulnerable when the Fed raises rates, particularly those with poor economic or financial fundamentals, unfavorable international imbalances or misguided policies that precipitate capital flight.

Allianz Global Investors believes that rising interest rates and normalizing monetary policy will stimulate businesses and individuals to make financial adjustments. Quantitative easing and several years’ worth of forward guidance—which collectively focused on repressing bond yields—led to excessive risk-taking, the mispricing of risk and financial-market distortions.

Nevertheless, US financial markets are functioning efficiently and the economy has mid-cycle expansion characteristics. We will continue to monitor the liquidity characteristics of short- and long-term fixed-income markets for signs of deterioration. Nonetheless, we believe that worries about raising rates from zero toward “normal” are vastly overstated, even if normal is lower than before. Historical experiences suggest these concerns are unwarranted.

Additional information

For additional information about this article, including endnotes and bibilography, click here.

About the author

Steven R. Malin, Ph.D., is an investment strategist and a director with Allianz Global Investors, which he joined in 2013. As a member of the US Capital Markets Research & Strategy team, he is responsible for making weekly US and global asset-allocation recommendations. Mr. Malin’s responsibilities also include analyzing global economic, financial, political and regulatory developments; and briefing institutional, retail and retirement clients. He has 25 years of financial-markets, central-bank and investment-industry experience. Before joining the firm, he was the director of research at Wealthstream Advisors, a private wealth management firm; and an advisor to Aronson Johnson & Ortiz, a quant-based institutional equity manager. Earlier, Mr. Malin was a senior portfolio manager at AllianceBernstein, serving institutional, sub-advisory, Taft-Hartley and private clients throughout North America. He also worked at the Federal Reserve Bank of New York for more than 16 years, and during this time he was an officer who held several senior positions, including senior economist, media relations officer, vice president in the communications group and corporate secretary. Before that, Mr. Malin was the senior economist, founder and director of the regional economics center at The Conference Board. He also taught graduate and undergraduate macroeconomics and risk-management courses at Barnard College-Columbia University and the City University of New York. Mr. Malin has a B.A. in economics from Queens College and a Ph.D. in economics from the Graduate Center of the City University of New York.

Investing involves risk. The value of an investment and the income from it will fluctuate and investors may not get back the principal invested. Past performance is not indicative of future performance. This is a marketing communication. It is for informational purposes only.

This document does not constitute investment advice or a recommendation to buy, sell or hold any security and shall not be deemed an offer to sell or a solicitation of an offer to buy any security. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer or its affiliated companies at the time of publication. Certain data used are derived from various sources believedto be reliable, but the accuracy or completeness of the data is not guaranteed and no liability is assumed for any direct or consequential losses arising from their use. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted.

© Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

AGI-2015-12-10-13918