Since the financial crisis in 2008, global regulators have been working hard to strengthen the banking system and forestall a similar calamity. A torrent of new regulatory requirements for financial institutions, for instance, aims to create global minimum requirements for liquidity and capital, increase transparency and decrease systemic leverage. The transactional intermediation that occurs between borrowers and lenders without governmental oversight – a vital piece of the world’s financial and funding mechanisms – has come under particular scrutiny. Balance sheets have contracted and liquidity premiums have been structurally altered – just one of several market consequences that should provide opportunities for active portfolios to be both more defensively scaled and opportunistically positioned.

Basel III may be the best known among the systemic regulations that have driven banks globally to review their balance sheet usage. One guideline stemming from Basel III is the Supplemental Leverage Ratio (SLR) regulation. It imposed a minimum 5% capital requirement on larger U.S. banks to constrain leverage and forced banks to begin looking at their assets on a non-risk-weighted basis. It has prompted banks to recalibrate hurdles for return on equity and to reconsider their commitments to lower-margin business lines.

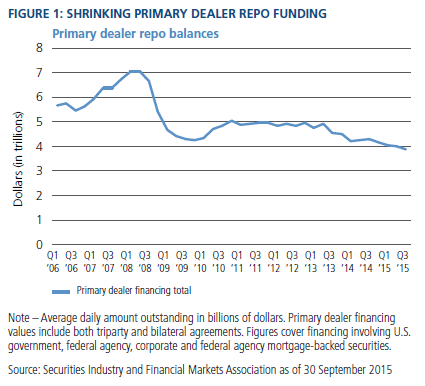

For many institutions, the repo business – which facilitates proprietary and client-funding activities related to Treasuries and other securities – was an obvious target for restructuring due to its low margins and large balance sheet usage. Not surprisingly, repo transactions have become more expensive. And primary dealer balance sheets have contracted (see Figure 1).

Repo repositioning

Repo markets are the plumbing of our financial system, helping to ensure proper market functioning. They are a medium for participants to borrow and lend fixed income securities. They facilitate access to collateral used to cover short positions, providing an essential source of liquidity in bond and derivatives markets. More broadly, repo markets will be a key conduit in the transmission of monetary policy as the Fed normalizes rates via its reverse repo facility.

As an example of why costs have risen, consider that banks no longer have the ability to report a netted amount of repo activity; new regulations require reporting of short-term wholesale funding on a gross basis, greatly reducing balance sheet efficiencies. The ability to “net” still exists, but only for qualified activities between banks/dealers. A bifurcated market has emerged as it costs more for banks to execute these repo trades with clients (asset managers, money market funds, etc.) than it does with qualified dealers. As a result, bid-offer spreads have increased dramatically, reflecting the new normal for liquidity and transaction costs.

Higher financing costs are not entirely attributable to the increased costs associated with these regulations. While smaller balance sheets are one factor, nominal funding costs also have risen in funding markets in anticipation of future Fed rate hikes.

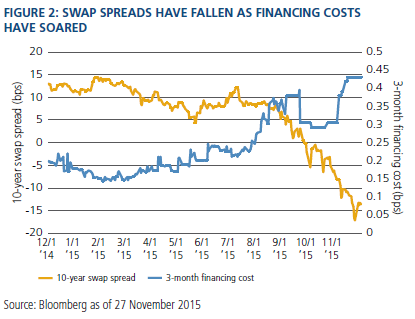

As to broad market impact, higher repo rates have influenced movements in swap spreads – the spread between a risk-free rate (usually Treasuries) and interest rate swaps of the same maturity. Balance sheets are one of the main resources market participants use to articulate views on swap spreads.

Until recently, swap spreads had traded at a positive level because a U.S. government-backed security is considered a safer credit. However, swap spreads have experienced a massive correction: 10-year swap spreads went from a local high of 12 basis points (bps) in July to -16 bps as of 19 November (see Figure 2). This tightening was precipitated by heavy selling by foreign central banks of U.S. Treasuries to fend off the devaluation of their currencies. This bloated primary dealer balance sheets, leading many to redouble efforts to reduce them.

Before recent regulations became a consideration, intermediaries would happily take the other side of these cash or swap trades because financing costs had been below Libor. However, with dealer balance sheets shrinking and financing costs increasing, there has been more of an onus to increase profits and returns on balance sheet capital, intensifying the tightening of swap spreads (see Figure 2). In the past, key market participants would see this as an arbitrage opportunity and take the other side of the trade, but balance sheet scarcity has made it increasingly difficult for these investors to counter such tightening trends. Thus, we believe this trend of constrained dealer market-making will likely continue in the foreseeable future. Furthermore, this situation will become more volatile and exacerbated around sensitive reporting dates (regulatory reporting dates, etc.).

Central clearing

Regulators, including the Federal Reserve and the Treasury Borrowing Advisory Committee (TBAC), are exploring several options to rehabilitate the marketplace. One idea is central clearing. It would seek to expand repo netting capacity outside the dealer community, providing much-needed balance sheet relief and reduction of financing costs.

However, the implementation of central clearing is still in its infancy. Moreover, a number of open issues obscure its potential benefits: How will trades be guaranteed? What is the operational and transactional (scope) workflow? Who will capitalize the entity?

In the end, we believe regulators will engineer favorable outcomes for the market. However we should caution that this is an evolutionary process that will take time; all interests – from dealers to end investors – must be considered equally to achieve an equitable and viable solution.

New pricing regime

What are viewed as funding strains today are in fact noteworthy structural changes, and will likely persist secularly for two reasons. First, bank leverage ratio limits and liquidity rules, especially the SLR, make it expensive for banks to offer repo financing. Second, the pressure on dealers’ Treasury inventories will likely continue to push GC (general collateral) repo rates higher relative to Libor.

The financial system is functioning smoothly but is clearly recalibrating to higher transactional costs for the first time in more than 20 years. The increased costs of “plumbing” coupled with banks’ rationalization of the true costs of their balance sheets will require all investors to become acutely aware of these altered conditions. In this new financial paradigm, repo levels and funding costs are a real-time barometer of the cost of capital for both investors and banks that must not only be monitored, but actively adjusted and scaled to account for in positioning.

The active opportunity

The bottom line is that continued balance sheet contraction should not be feared but monitored to understand how the cost of capital will continue to evolve. Wider liquidity premiums will provide opportunities for active portfolios to be more defensive while capitalizing on opportunistic situations – buying assets at more attractive levels with more potential for excess return. Moreover, active strategies could benefit from surveying the landscape for attractively priced assets that are backed by strong credits and collateral. On the other hand, passive strategies that seek to mimic indexes may be forced to pay market liquidity premiums as they seek to replicate benchmark exposures, regardless of price or attractiveness on a relative basis.

For PIMCO’s clients, our active management template provides additional degrees of freedom, which seek to mitigate some of these increased transaction costs while working to capture appropriately priced and attractive liquidity premiums.