Globally, equity investors faced a number of uncertainties in 2015 as the anticipation of rising US interest rates, weak commodity prices and a growth slowdown in China weighed on sentiment. These headwinds were arguably stronger for emerging markets overall, albeit more damaging to some markets than others. Here, Carlos Hardenberg, senior vice president and director of frontier markets strategies, explores investment opportunities we’re spotting in frontier markets (the less-developed subset of the emerging market universe) with an eye on a few countries we think could best weather the investment climate ahead.

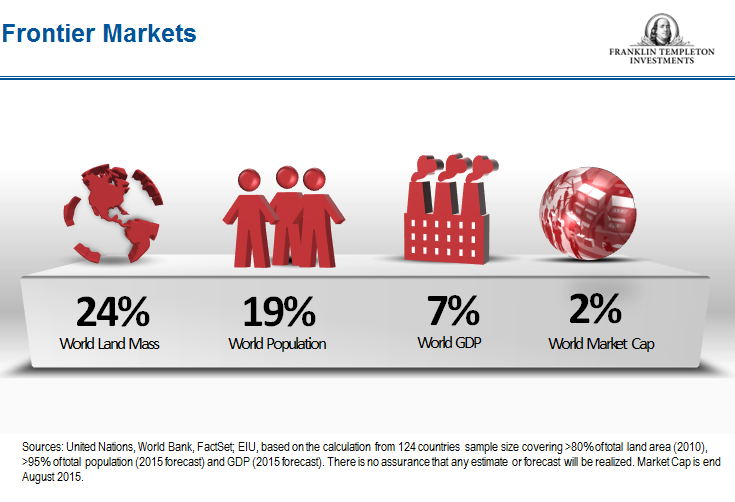

When talking about frontier markets, the first question many people have is how to classify them. One of the more interesting methods of defining a frontier market that I once read was the absence of a Starbucks, the popular coffee chain, in said country—though I’m not sure I’d necessarily agree with that assessment! Benchmarks such as the MSCI Frontier Markets Index1 can provide a guide, wherein the inclusion of and weighting to specific countries is based on economic development, size, liquidity and market accessibility. At Templeton Emerging Markets Group, we don’t adhere to the constraints of any particular benchmark. We view frontier markets more broadly as newer or younger markets in an earlier stage of economic development than larger emerging markets, generally with higher growth rates and a lesser degree of foreign investment and investment research coverage. Frontier markets are located throughout Asia, Africa, Europe and South America.

Investor Caution Dominates 2015

In times of heightened investor caution or uncertainty, the perceived risk of emerging markets overall as an asset class—and frontier markets in particular as a subset—can lead to periods of underperformance versus developed markets. That is something we witnessed in 2015. However, 2015’s market environment highlights to us the importance of taking a bottom-up approach, looking at individual countries and individual companies in them with a critical eye. You can’t paint all emerging markets—or all companies within them—with the same broad brushstroke. For example, some of the world’s best-performing markets in 2015 may come as a surprise to some people—one being Venezuela, which returned more than 200% in 2015,2 as well as Argentina, which returned more than 50%.3 Both countries have been dealing with difficult economic and political environments—yet, there are companies located in them that have been able to prosper. We could point to several other frontier markets across the globe that have outperformed in 2015 despite a challenging environment for emerging markets overall as an asset class.

We regard challenging market environments as opportunities, using downturns to pick up stocks that we deem attractive but unfairly punished. While many investors aren’t investing in frontier markets, we also believe that could change in time. It’s our view that increased familiarity with companies based in these markets among international investors could feed higher valuations.

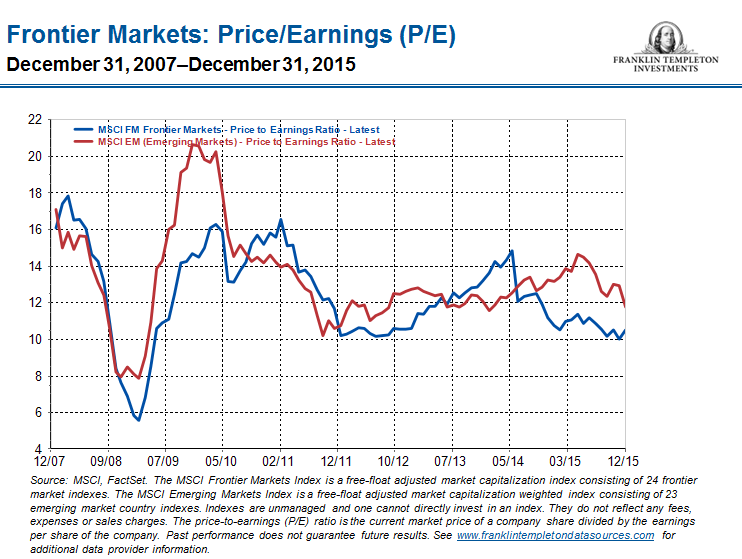

Frontier markets represent exciting long-term investment opportunities for our team. We see favorable fundamentals including strong economic growth, abundant natural and human resources, favorable demographic profiles, the potential for rapid technological progress, and potential benefits from improving infrastructure and improving standards of governance. We believe the opportunity is magnified by market valuations for frontier corporations that often stand below those of their peers in more developed markets. We would note in this regard that recent market fluctuations have increased the gap between the valuation of frontier markets and those of emerging and developed markets, as measured by the relevant MSCI indexes. Additionally, many frontier markets have significant domestic drivers that can reduce their correlation with their emerging and developed market counterparts and provide potential diversification for investors. We’d like to highlight a few frontier markets that we are particularly excited about right now.

Vietnam

We have been investing in Vietnam for many years, but it’s a market that many investors are just now casting an eye on. Nearly a decade ago, we came to the conclusion that Vietnam presented a unique investment opportunity within the frontier space because it was under-owned and under-researched; at that time, there was virtually no English-language research on Vietnamese companies. Vietnam seemed largely ignored compared to its neighbors in the region, and there was almost no foreign company ownership either. We spent a lot of time traveling throughout the country, meeting local managers and getting to know the business and political environment before we decided to open an office there. Vietnam operates with a one-party political system, with enormous state control and ownership similar to China. However, we noticed that the mindset of the people we encountered was overwhelmingly pro-business and pro-capital.

When we started investing in Vietnam in 2008, the economy was facing some challenges, including a chronic current account deficit. Although Vietnam possessed oil and natural gas, it couldn’t be refined domestically, so the government needed to send it out and buy back the end products (the country has been working to change this in recent years with the construction of domestic refineries). As we learned more about the investment environment in Vietnam, we also noticed a rapid increase in the level of foreign direct investment, and the quality of it was very high—brands known around the world were setting up manufacturing operations in Vietnam and hiring tens of thousands of people. Today there is a long list of international companies that manufacture goods including electronics, textiles and furniture in Vietnam. We expect more multinational companies in a number of industries could set up shop in Vietnam, taking advantage of its low-cost labor and well-educated workforce.

In addition, the business owners and managers we have spoken to over the years have conveyed that it was relatively easy to do business in the country compared with some others in the region. The World Bank’s report on the ease of doing business ranks Vietnam 90th among 189 countries surveyed in 2016, an improvement from 99th in 2013 and higher than India, for example, ranking 130th.4

Vietnam has a number of positives in its favor, in our view. Gross domestic product (GDP) growth has been strong, forecast at 6.5% in 2015.5 Vietnam has many seaports and possesses one of the most important trade routes on the planet, with access to neighboring China’s very large consumer market. Vietnam has been building its export market and also a large domestic consumer market. Tapping into the domestic consumer market is a theme we’ve been exploring for potential investment opportunities. One example is the dairy industry, which has been a rural and unorganized market in Vietnam. Typically people would purchase their milk from a neighbor or nearby farmer with a cow, not at a supermarket. In a short time span, we’ve seen a regulatory framework developed, and industrial producers have come into the market and have built brands with more formal distribution channels.

In addition to a recent trade agreement inked with the European Union, we think Vietnam could see significant benefits from the proposed Trans-Pacific Partnership (TPP), as the reduction or elimination of tariffs could be a boon to its export market, particularly to large-destination markets that look to be part of the TPP—namely the United States and Japan. Vietnam has a vibrant but underutilized fishing industry, and more of its seafood could land on plates of diners in these countries and others.

While foreign ownership has been rising, Vietnam’s government doesn’t want to lose control of its assets, so we expect foreign ownership limits will remain a subject of debate. Nevertheless, we think Vietnam is a market that should continue to attract investor interest in the coming years.

Bangladesh

Elsewhere in Asia, Bangladesh has a significant domestic market with a population of more than 169 million.6 Many people may remember when Bangladesh’s formidable textile industry made headlines in 2013, after an eight-story building in the Rana Plaza complex collapsed in a fire. Virtually all the big global textile companies were producing in Bangladesh—which is still the case today. The fire was a terrible tragedy, but it brought attention to the need for better regulation and oversight, including safety rules for producers. There is still work to be done, but we are seeing some progress and improvements being made. Bangladesh has developed a strong niche, one where it is world-class. In textile production, Bangladesh is extremely efficient, with the knowledge and skills to integrate into the global trading network. And, the industry has fairly high barriers to entry, so we expect Bangladesh to retain its leadership position. We have been investing in the country and continue to look for compelling opportunities there, not only in the textile area but in other industries that can take advantage of the growth taking place there.

Nigeria (and Across Africa)

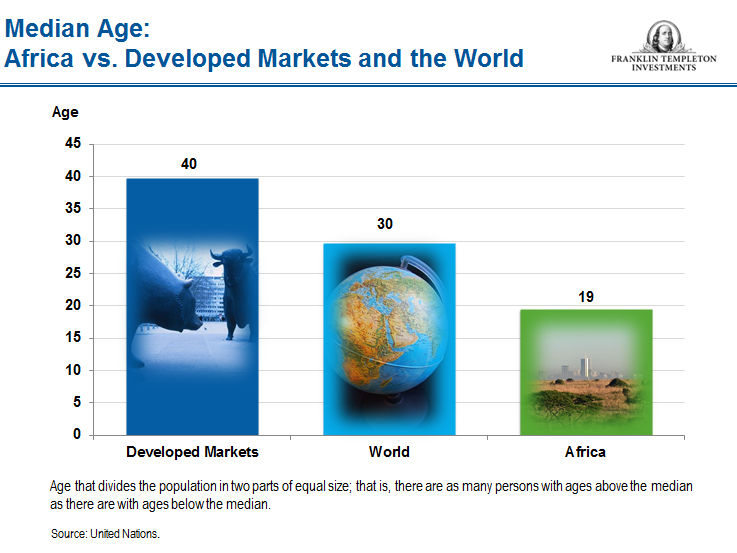

With the exception of South Africa, all of the countries on the African continent are considered to be frontier markets. The largest market by population is Nigeria, which is an important market for us in terms of the range of potential opportunities. There’s no question that Nigeria has faced a number of challenges, with virtually no power grid and poor infrastructure. The power production of the entire country is probably similar to one street in New York City. However, the ability of the Nigerian people to operate under the most difficult circumstances is astonishing. What has really surprised me in my travels there is how people not only in Nigeria but throughout Africa have been embracing mobile telecommunication and the Internet. Many people with hardly any food or a roof over their heads have smartphones and use mobile payments for various goods and services.

Mobile banking is quite sophisticated in Africa due to the unavailability of physical banks or ATMs to a vast population. Traveling in Africa (whether in Nigeria, the Ivory Coast, Senegal, Ethiopia or Kenya) one can’t help but notice the Chinese influence on the continent, building roads, ports, airports and tunnels, and becoming local partners with African businesses. While Africa’s commodities are of interest to the Chinese, many are staying in Africa and setting up their own retail businesses there. It’s a symbiotic relationship.

The fall in commodity prices in the past couple of years has been a challenge for African countries, particularly those dependent on oil revenue. However, it could also be viewed as an opportunity for these countries to reform and diversify their economies. It forces governments to become more disciplined, to improve income collections and find ways to expand the economy and its coffers through more diverse ventures, not only through the sale of a single commodity. We are seeing a number of large multinational companies establish a presence in Africa for the first time—particularly in countries with improving infrastructure and ease of doing business—to access its large, vibrant and youthful populations.

We think Africa is probably the most exciting story of the future when talking about frontier markets, but investors may need to be patient and to understand some of the unique aspects of doing business there as well as the risks.

Divergences—and Debt

These are just a few of the countries we’re exploring as we look ahead to 2016. We expect 2016 is likely to be another year marked by market divergences—and also, likely global monetary policy divergences. We would note that while investors may remain a bit risk-adverse in early 2016 amid potentially rising interest rates in the United States, other central banks—including those in China, Japan and Europe—are in easing mode and providing market liquidity. Some emerging and frontier markets will weather a potential US rate hike better than others, but we don’t expect it to diminish our case for investing in them. We would note that one thing many frontier markets have in their favor is low levels of debt both in the private and public sectors, something that should help them navigate potential shocks in the year ahead.

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Important Legal Information

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

______________________________________________________________

1 Source: MSCI. The MSCI Frontier Markets Index is a free-float adjusted market capitalization index that is designed to measure equity market performance of frontier markets. Constituents include large- and mid-cap representation across 24 countries: Argentina, Bahrain, Bangladesh, Bulgaria, Croatia, Estonia, Jordan, Kenya, Kuwait, Lebanon, Lithuania, Kazakhstan, Mauritius, Morocco, Nigeria, Oman, Pakistan, Romania, Serbia, Slovenia, Sri Lanka, Tunisia Ukraine and Vietnam.

2 Source: Bloomberg LP, 2015. The IBC Index from the Caracas Stock Exchange (Venezuela), also known as the General Index, is a capitalization-weighted index of the 15 most liquid and highest-capitalized stocks traded on the Caracas Stock Exchange (Bolsa de Valores de Caracas). As of December 30, 2015, year-to-date the index was up 281%. Indexes are unmanaged, and one cannot directly invest in an index. They do not reflect any fees, expenses or sales charges. Past performance is no guarantee of future results.

3 Source: Bloomberg LP. The Argentina Merval Index, a basket-weighted index, is the market value of a stock portfolio selected according to participation in the Buenos Aires Stock Exchange, number of transactions of the past six months and trading value. As of December 30, 2015, year-to-date the Merval Index was up 60%. Indexes are unmanaged, and one cannot directly invest in an index. They do not reflect any feeds, expenses or sales charges. Past performance is no guarantee of future results.

4 Source: World Bank, “Doing Business 2016.”

5 Source: IMF World Economic Outlook database, October 2015. There is no assurance that any estimate or forecast will be realized.

6 Source: CIA The World Factbook, July 2015 estimate. There is no assurance that any estimate or forecast will be realized.

© Franklin Templeton Investments

© Franklin Templeton Investments