On January Barometers and Market Bargains

If market action in the first few weeks of January is a barometer for the year ahead, investors could be in for some stormy weather. (Of course, we all know how accurate weather predictions are—let alone market predictions!) Templeton Global Equity Group views times of market turmoil as opportunities, as it seeks to unlock bargains for the patient investor who knows cycles—and sentiment—can quickly change. Here, the team takes a look at the events driving global equity market action so far this year, and shares their value-oriented investment strategy in light of the conditions they currently see.

As we have written elsewhere, in recent years, traditional “value” stocks have been suffering their worst stretch of underperformance on record in terms of both duration and magnitude. After years of unrelenting pressure on low-multiple stocks, it’s our view that the current environment is rife with opportunity for patient value investors. Though not yet fully recognized as such, this may be a meridian hour for value. It has certainly been a long time in the making. A secular bull market in fixed income assets delivered bond investors equity-like returns with little volatility for the better part of three decades. Then came the global financial crisis, reflexive risk aversion and the entry of state actors with limitless money-printing powers into the bond market via quantitative easing, mopping up whatever value was left in the low-risk bond space. The disappearance of low-risk yield opportunities in fixed income markets has subsequently forced investors out the risk curve and into traditionally defensive equity sectors with reasonable payouts. Meanwhile, the debt deflation purgatory enveloping the world economy since the global financial crisis has afforded a scarcity premium to growth. Consequently, the two types of stocks that embed the greatest expectations—and carry the loftiest valuations—are income-oriented bond proxies (consumer staples, utilities) and self-sustaining growth generators (health care, technology, consumer discretionary). Not surprisingly, these five sectors are also the market’s most “crowded,” as measured by a composite of institutional ownership, sentiment and consensus expectations. This does not suggest that these sectors are devoid of value altogether; however, it comes as no surprise to us that bargains are less abundant in these popular areas.

As the late Sir John Templeton observed in 1979: “If you want to buy the same thing that is popular with your friends or popular with the investment analysts, you can’t get a bargain … If you are going to have superior performance, you’ve got to buy what other people are not buying, or even what they are selling.” The extreme valuation premiums afforded to defensive, high-quality and high-growth stocks means that their inverse corollaries—cyclically geared value stocks—are historically cheap and under-owned. In contrast to the aforementioned sectors, data have shown that energy, materials, financials and industrials were near historical troughs for “crowding” as of year-end. For patient investors, we believe these sectors likely offer some of the best longer-term opportunities in equity markets today. Yet, while valuation has been among the strongest indicators of returns over time, it is historically unreliable as a timing signal. With that limitation in mind, let us walk through some of our main portfolio convictions, discussing valuations, but also industry trends and developments, in an effort to determine where we are in the cycle and what the outlook for 2016 might bring.

Value Signals in Energy and Financials

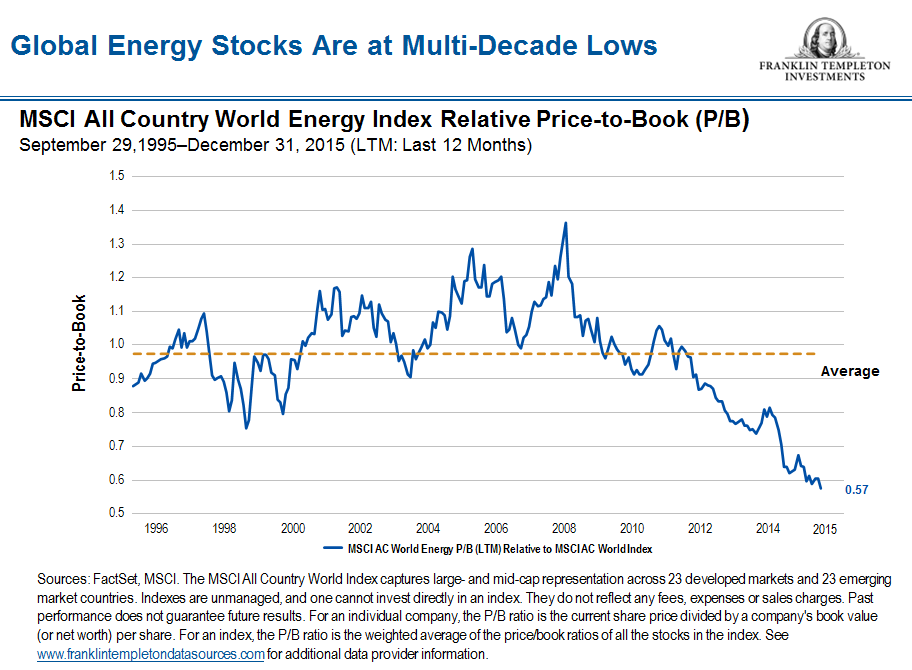

The energy sector dominated headlines in 2015 as oil capped its biggest two-year loss ever amid a widening supply glut and intensifying fight for global market share. From a valuation standpoint, the buy signal for energy stocks is increasingly interesting to us. Based on 20 years of global data and nearly 90 years of US data, the energy sector has never been cheaper on price-to-book multiples than it was at the end of 2015.1 The skeptics’ response to these compelling headline valuations tends to be suspicion of book values, which indeed are likely overstated in some instances and vulnerable to further impairment. However, in the first half of 2015 alone, oil companies took more write-downs than any other full year on record. While there may yet be further attrition in the energy space, a great deal of pain has already been felt.

As we assess the energy sector outlook, we first recognize that global oil demand in 2015 was the highest in five years,2 suggesting that the recent price collapse is mostly a supply issue. Saudi Arabia’s decision to push volume into an oversupplied market is largely responsible for keeping prices lower for longer. It is a strategy rooted in both economics (oversupply forces high-cost producers out of business and preserves Saudi’s market share) and geopolitics (low prices inflict immense pain on petro-state adversaries like Russia and Iran). Increased output from elsewhere in the Middle East, as well as resilient supply from US shale fields and production successes in Russia and the Gulf of Mexico, all compounded the supply glut and prolonged rebalancing in 2015. Yet in our view, this situation is likely transitory. Major sovereign producers do not have the financial wherewithal to tolerate low oil prices indefinitely. Saudi Arabia, Russia, Brazil and Venezuela are all experiencing significant budgetary shortfalls attributable to cheap oil. Keep in mind that oil is a finite resource with a natural decline rate of 4%–5% per annum on average, a number that only increases as companies cut back on sustaining capital to weather the weak price environment. As the industry retreats deeper into preservation mode, we think the consequent underinvestment in production bodes well for an eventual oil price recovery.

Risks to a timely recovery include any unexpected production increases (Iran, North Africa and a highly elastic US shale industry all come to mind) or demand hiccups due to an economic slowdown. Benign credit conditions and rapid service cost deflation have also prolonged the adjustment, though these buffers are largely exhausted. Within the sector we continue to favor firms with the balance sheet strength to withstand any protracted price weakness as the market finds its way back into balance.

Financials is another sector we see sending convincing value signals, particularly in Europe. In general, historically low interest rates and a muted business cycle have kept pressure on financial stocks by constricting net interest margins and stifling credit activity. While the banks can’t magically conjure up a turn in the business or credit cycles, it is hard to imagine rates heading much lower from here. Indeed, with the US Federal Reserve finally beginning to hike interest rates and half of all European government bonds of less than five-year maturity paying negative yields, it would appear to us that the rate cycle is bottoming. More to the point, we are encouraged by the progress apparent in the measures that these companies can control. The US banking sector underwent intensive reforms following the global financial crisis, cutting costs, shedding risk and divesting or restructuring underperforming assets. Regulations were tightened and penalties imposed for infractions of varying severity. Today, despite a still-difficult macro and regulatory environment, the industry appears to have largely righted its ship. Bargains remain selective in the US banking sector, and concentrated among firms with sustainable competitive advantages or underappreciated international franchises.

Europe’s banking crisis reached its apex three years after the United States, and its own industry restructuring has followed a similar path. Last year, there was significant progress in Europe as high-profile leadership changes at a number of major banks suggested the end of crisis-era restructuring and a potential new dawn of growth and stability, including the prospect of improving dividends and capital returns. Bank capital and liquidity in Europe have become much more robust and loan-loss provisions have scope to decline further as macro conditions stabilize. While Europe’s business cycle remained admittedly muted at year-end, lead indicators of loan growth, including credit demand, money supply growth and loan officer surveys, were distinctly positive. Likewise, Europe’s onerous regulatory regime showed some signs of abatement as the year progressed, with UK Chancellor George Osborne easing the tax burden on banks, while European Union Financial Services Commissioner Lord Hill suggested publicly that the post-crisis regulatory push may have been excessive.

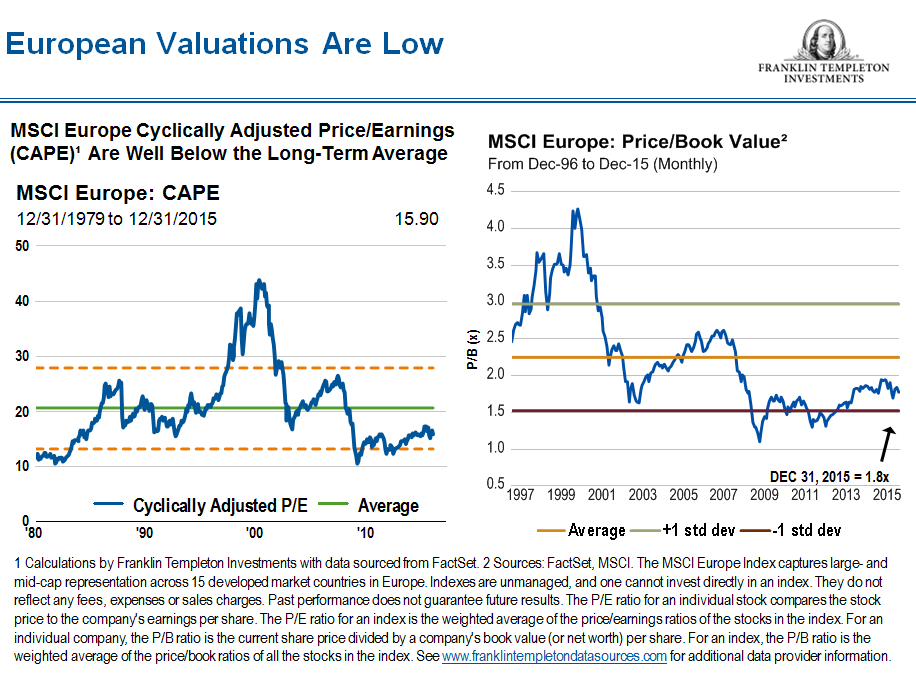

Elsewhere on the policy front, monetary accommodation remained extreme and the recently tabled proposal for a capital markets union raised hopes of a more dynamic, liquid and integrated industry. Finally, looking at valuation, European banks traded at a material discount to tangible book value, one standard deviation3 below their historic forward price-earnings multiple, and near a 20-year low relative to global banking peers as the year came to a close.4 We are also finding select financial sector values in Asia, in both mature, under-earning banking markets like South Korea and Singapore, as well as underpenetrated, growth-oriented markets like China (particularly in insurance) and India (particularly in banking).

China’s Knock-on Effects

The turmoil in mainland Chinese equities and subsequent knock-on effects in markets around the world have understandably put investors on edge in the first weeks of 2016, which warrants closer examination. China’s market rout has various explanations: hedge funds are becoming forced sellers, a lock-up period for major shareholders was due to expire (that has since been extended), and currency maneuvers are sparking fears of competitive devaluation. The circuit breakers initiated recently to stem such a panic have had the opposite effect, amplifying a rush for the exits before the market shuts down (these have since been suspended in light of their deleterious effect). Setting aside the discussion of these technical and short-term factors, China faces significant economic and financial headwinds, and a series of policy missteps have raised concerns about its ability to successfully manage these challenges. However, it is important to keep in mind that China’s current transition from a manufacturing-driven industrial economy to a service-driven consumer economy represents a normal step in the maturity and evolution of any economy, and we have consistently expected this transition would be a multi-year process.

What complicates and adds risk to the process for China is the country’s elevated debt levels, the true extent and proliferation of which is unknown. Another major headline risk in the near term is China’s management of the renminbi. On the one hand, Beijing welcomes the easier financial conditions and improved export competitiveness associated with a somewhat weaker currency. On the other hand, China has significant external liabilities and growing capital outflows, and cannot afford to have its gradually managed currency decline spin out of control, such that its foreign reserve buffer is compromised. The People’s Bank of China has been selling US dollar reserves at an alarming rate to maintain an orderly devaluation, and there is a more-than-trivial risk that it loses control should pressures continue to intensify. Yet, for those waiting for the China-led emerging market “blowup,” it is important to recognize that major emerging economies ranging from Russia to China to South Africa to Brazil have already experienced crises of considerable magnitude in the past couple of years alone. Investor sentiment in emerging markets was at a 20-year low at year-end, and an index of emerging market stocks was the cheapest ever on trend-earnings multiples, suggesting that, in at least some instances, concerns may be adequately discounted. While we have maintained a cautious and highly selective approach to these volatile markets, valuations are broadly becoming interesting.

Ultimately, once the dust settles (either via an abrupt “hard landing” adjustment or a prolonged “soft landing” evolution), China should be left with an economy that, while slower growing, is more balanced, dynamic and market driven. Finally, investors should not confuse China’s financial markets with its economy. The market still represents only a modest percentage of the country’s gross domestic product, and its impact on household wealth is limited (equity ownership is not widespread among Chinese, who tend to have more of their wealth in real estate). Events in China are a reminder that equity markets are volatile. As we saw during the global financial crisis, even the United States—considered the world’s deepest, fairest, most liquid, best-regulated market—is prone to extreme price swings far exceeding any lasting changes in underlying business value. A market like China’s, where investment and regulatory experience is limited and liberal aspirations are fundamentally at odds with the reigning political ideology, is bound to be volatile. Admittedly, the growth of such a market adds an element of instability to the global financial system, but it also increases opportunities over the long term for bargain hunters to take advantage of volatility.

A critical lesson that we have learned through six decades of investing in global equity markets is that returns accrue to value intermittently. When the value cycle turns, it tends to do so swiftly and abruptly. Being properly positioned for these turns is key to capturing the long-term benefits of the value investment discipline. We are now witnessing historic extremes in the discount afforded to value relative to growth, quality and safety. While this environment has been (and may remain) painful for some time, the eventual normalization of these extremes represents the most compelling opportunity in equity markets today and our portfolios are positioned accordingly.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Value securities may not increase in price as anticipated, or may decline further in value. To the extent a portfolio focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a portfolio that invests in a wider variety of countries, regions, industries, sectors or investments. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments; investments in emerging markets involve heightened risks related to the same factors.

_______________________________________________________________________

1 Sources: FactSet, MSCI. Past performance does not guarantee future results. For an individual company, the price-to-book (P/B) ratio is the current share price divided by a company’s book value (or net worth) per share. For an index, the P/B ratio is the weighted average of the price/book ratios of all the stocks in the index. See www.franklintempletondatasources.com for additional data provider information.

2 Source: International Energy Agency, “Oil Market Report,” December 11, 2015.

3. Standard deviation is considered a measure of volatility, representing deviation of a set of data from a mean.

4 Sources: FactSet, MSCI. Past performance does not guarantee future results. The P/E ratio for an individual stock compares the stock price to the company’s earnings per share. The P/E ratio for an index is the weighted average of the price/earnings ratios of the stocks in the index. Seewww.franklintempletondatasources.com for additional data provider information.

© Franklin Templeton Investments

© Franklin Templeton Investments