Last week took investors on a wild roller-coaster ride. Stocks and oil sold off earlier in the week, with the S&P 500 Index plunging dangerously close to the 1800 level and oil falling below $30 a barrel. It was an alarming experience for many investors, with some market pundits arguing that 2016 is going to be another 2008.

By mid-week, stocks started to bounce back and were further helped by comments from European Central Bank (ECB) head Mario Draghi on Thursday. His commitment to extremely accommodative monetary policy fueled a stock market rally for the first time in weeks, which makes sense given markets have arguably been spooked by the start of the Fed's normalization of monetary policy. By the time we reached Friday, stocks were in recovery mode and actually posted gains for the week, while oil finished above $30.

Where to from here?

So where do we go from here—is this the correction we have been waiting for? Is it already over? Is this it for capitulation? It's difficult to tell right now. Much of it will depend on the forces that have moved markets thus far in 2016: China, oil prices, geopolitical crises, the US economy and, perhaps most importantly, what investors think the Fed will do for the remainder of 2016. Some are arguing that financial conditions have tightened enough that the Fed does not need to raise rates this year, while others believe the FOMC members' policy prescription of four rate hikes will come to fruition.

There seems to be so much uncertainty right now in so many ways. We can't know where this year will take us—so instead we need to focus on what we do know, which is that investor psychology and short-term perspectives can hurt investors' ability to realize their financial goals.

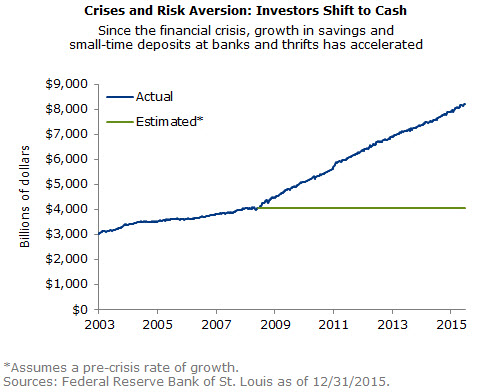

When smart money is irrational

The recent market sell-off reminds us of the dangers of investor psychology—as did the market sell-off of 2008—when we saw money move out of equities and into cash. Unfortunately, investors have come to believe key tenets of modern portfolio theory that are constantly being regurgitated to them—that investors are rational and markets are efficient. Many investors believe that when stocks experience a major drop like the one that just happened, there's something "the market knows" that the Main Street investor doesn't—which in turn results in herding behavior, as investors follow what they perceive to be "smart money."

The reality is that market moves are often dictated, or at least greatly exacerbated, by program trading where algorithms are created by humans prone to the same investor psychology mistakes. Individual investors with a long enough time horizon should be cautioned against joining this large computer-driven herd.

Stay invested

Investors need to remember, especially during sell-offs, that in the short term investors can be anything but rational and markets can be anything but efficient. To put it another way, Benjamin Graham once said that in the long run, the stock market is a weighing machine but in the short run, the stock market is a voting machine. And it is for this very reason that we tell investors to take a long-term approach to investing. They can get burned over the shorter term because the stock market is inefficient and investors are not rational. But as history and market performance shows, all is smoothed out over the longer term—if investors stay invested.

The reality is that it's very hard for human beings to time the market. Despite the kind of turbulence and losses we just experienced, it is better to remain invested. The caveat is that investors need to be prepared for substantial volatility in the months to come. For those who can't stomach that, they should consider an actively-managed, multi-asset solution where an investment professional tactically allocates among asset classes in order to dodge risks and embrace opportunities. In an environment of higher volatility, we believe both agility and skilled, active investing may enhance returns and better position investors to meet long-term goals.

Kristina Hooper is the US Investment Strategist and Head of US Capital Markets Research & Strategy for Allianz Global Investors. She has a B.A. from Wellesley College, a J.D. from Pace Law, a master's degree from Cornell University and an M.B.A. in finance from NYU, where she was a teaching fellow in macroeconomics.

Subscribe Today

The Upshot is available as a subscription for financial professionals only. New issues will be delivered via email every Monday. Visit us.allianzgi.com/theupshot to learn more.

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

A Word About Risk: Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

There is no guarantee that an active manager’s investment decisions and techniques will be successful. It is possible to lose some or all of your investment using active management.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

AGI-2016-01-25-14371