Over the past year, Russia has faced a growing number of challenges that have the potential to weaken President Putin’s hold on the reins of power. In this report, we will discuss recent trends in the country, including the economic problems caused by falling oil prices and the military operations occurring in Ukraine and Syria. We will examine the Putin government’s responses to these issues. As always, we will conclude with market ramifications.

The Russian Problem

Let’s begin with the geopolitics of Russia. Russia is essentially a landlocked country with few natural defenses.

This map shows the physical characteristics of Europe and Russia. Note the northern European plain runs from southwestern France to the Ural Mountains. This plain has been key to European wars for centuries. Germany’s war plans for WWI were designed to fight a one-front war on this plain (the plans failed); Hitler signed a non-aggression pact with Stalin to secure a single-front war against France and later turned his sights on the Soviet Union. Napoleon also marched along this plain to Moscow in 1812.

There are three red arrows on the map, denoting Russia’s primary outlets to seas. Two of the outlets, the Baltic Sea and the Black Sea, can either be blocked by European powers or Turkey, respectively. The Russian port of Murmansk is ice-free but, during the Cold War, NATO air bases in Norway and Scotland, along with carrier groups, were capable of bottling up the Soviet navy and blockading sea traffic. Despite the multiple outlets, Russia lacks reliable access to seas, rendering it essentially landlocked.

As the Greek historian Thucydides noted, nations with access to the ocean tend to be cosmopolitan and have stronger economies due to trade, whereas landlocked nations tend to be more insular and poor. Athens, a maritime power, and Sparta, a land-based power, are examples of these differences. Athens was richer but less unified compared to Sparta.

Due to climate conditions, most of Russia’s agriculture is centered in its western region near its borders with Europe. This region is also where its population is most dense.

(Source: University of Texas)

This Soviet-era map shows population density. Note that most of the population was in the west; in fact, what is now Ukraine had relatively high density.

(Source: University of Texas)

This map shows land use; only about 10% of the former Soviet Union was arable, with most agricultural activity occurring in the western regions.

Russia’s geography has created conditions for an insular society. Russia has been destined to be relatively poor due to its restrained foreign trade, and due to its lack of arable land it has mostly been a supplier of natural resources, which it has in abundance. Like Sparta, Russia puts a high value on unity; its society has been inherently suspicious of outside ideas.

As noted above, Russia has few natural barriers from invaders. Throughout its history, it has tried to expand westward to force invaders to march long distances to reach the core of Russia around Moscow. Both Hitler and Napoleon found that the combination of Russian infantry and winter were deadly to invading forces.

However, there is an internal contradiction to Russia’s desire to expand its influence westward. Invading and pacifying regions is expensive and Russia isn’t a rich nation. To maintain control, Russia has historically sold natural resources to provide economic support to annexed regions. In addition, Russia has traditionally deployed extensive internal security agencies to maintain order. Subsidizing the economies of captured areas and paying for security is expensive. Over time, when it becomes too expensive, annexed areas rebel and Russia loses its buffer.

Thus, to survive, Russia has three imperatives. First, it must have strong and loyal security services; these are necessary to quell internal dissent and to maintain order in buffer areas. Second, Russia must keep its elites satisfied. In general, this has been accomplished by giving them a share of natural resource revenue. These elites often include senior members of the security forces, so their loyalty is important. Third, the state must provide a modicum of economic support to the population. Russians are used to having less than their European or American counterparts but the population cannot be taken completely for granted.

If these three imperatives are met, Russia will have reasonable economic growth, internal security, satisfied elites, a pacified population and buffer regions to protect the country from outside powers. If these imperatives are not met, whomever is in charge of Russia is in trouble.

Recent Trends

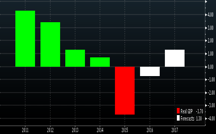

The drop in oil prices is putting pressure on the Russian economy.

(Source: Bloomberg)

This chart shows annual GDP for Russia with two years of forecasts from the IMF. In our experience, it is rare for international organizations to predict recessions but the IMF is projecting a second year of negative growth for Russia.

As oil prices have fallen, the Russian central bank has allowed the ruble to depreciate.

(Source: Bloomberg)

The previous chart shows the normalized value for oil prices and the ruble, beginning in 2010. A rising ruble line shows a weaker currency, in that it takes more of the local currency to buy a dollar. Since mid-2014, as oil prices began to fall, the Russian central bank has allowed the ruble to decline. Allowing the currency to depreciate protects the oil companies, who earn dollars on sales but pay their local expenses in rubles. Unfortunately, a weaker currency boosts import prices and reduces the purchasing power of Russian households.

This chart shows Russia’s yearly change in CPI with the effective exchange rate. Note that inflation jumped as the currency declined.

Real incomes fell sharply with the decline in oil prices. In fact, the last time real incomes fell this hard was in 1998, another period of low oil prices that coincided with the Russian debt default.

Russians tend to be stoic. However, as real incomes decline and inflation rises, there are signs of growing disenchantment with the regime. Recent polls suggest that Russians are worried that another 2008 is in the offing. There have been protests by Russian truck drivers against the implementation of tolls on Russian highways. Polls indicate that 63% of Russians support the truckers and see the tolls as further gouging by the nation’s elites. It is worth noting that during the last major series of protests in 2011-12, the highest level of support for Moscow protestors was around 40%.

Other protests have been steadily rising. Social commentators note that an average of 250 protests occur each year in Russia. Last year, that number was exceeded by summer. Actions against unpaid salaries are increasing. Interestingly, protests have also shifted out of the industrial sector and to the service sector, which hasn’t traditionally seen job actions. In the past, service workers tended to move to other work if conditions deteriorated. Apparently now there is nowhere else to go. So far, the protestors have been isolated and there isn’t any evidence to suggest they are becoming organized; however, if they do, Putin could face rising pressure in an age of austerity.

Along with the drop in oil prices, Russia is engaged militarily in Ukraine and Syria. Ukraine has been under Russian control numerous times in the past and has traditionally been part of Russia’s buffer zone. When the 2013-14 Euromaidan Revolution ousted former Ukrainian Prime Minister Yanukovych, Russian President Putin seized the Crimea and surreptitiously invaded areas of eastern Ukraine. Russia essentially controls the Donetsk and Luhansk regions in Ukraine, along with the Crimea. Unfortunately, the Russian military does not have the capacity to expand further and the areas under Russian control have become a major expense for the Putin regime, costing almost €950 mm per year, or about 0.6% of Russia’s fiscal budget; this does not include payments in kind.1 In addition, Europe and the U.S. implemented sanctions against Russia after Russia attacked Ukraine. Combined with falling oil prices, the sanctions have further weakened the Russian economy.

Russia has also expanded its air forces in Syria and is conducting air operations against rebel forces aligned against Syria’s President Assad. These operations have targeted groups trying to oust the regime and have mostly avoided Islamic State positions. Russia’s actions have not been welcomed by the U.S. or the Gulf States. Although Putin’s move was initially lauded by the Russian public, which viewed the expansion of support as raising Russia’s global prestige, its popularity appears to be waning as the conflict stalls.

Putin’s Response

These conditions are major problems for Putin. Although there is no evidence his position is threatened, he faces the delicate task of fulfilling Russia’s three imperatives. In the short term, Putin has to do three things; first, he must take steps to improve the economy. Accomplishing this will allow him to keep the elites satisfied and have enough funds to improve living conditions for Russians. Second, he must address the deteriorating fiscal situation. Third, he must expand the buffer zone to protect the Russian core from invasion and outside influences. Putin has taken recent steps in an attempt to meet these goals:

Ending the Assad regime: Last December, Putin sent Igor Sergun,2 the director of military intelligence (GRU), to Damascus to inform Syrian President Assad that it was time for him to step aside. Assad refused the directive and remains in power. However, by sending Sergun, Putin has tipped his hand and indicated that he is not wedded to supporting Assad. Why would Putin press Assad to resign? We suspect Putin would like to trade Assad’s “retirement” for sanctions relief. We would expect Putin to try other tactics to lever his cooperation in the Middle East for sanctions relief and greater influence in Ukraine. Building influence in Ukraine is part of rebuilding Russia’s buffer zone.

Supporting a recovery in oil prices: Russia has a spotty history with OPEC. In the 1998 agreement that ended the market share war, Russia promised to make production cuts. There is no evidence that the Russian oil industry reduced output. Saudi Arabia, who triggered the downturn in oil prices that began in the summer of 2014, insists that Russia must be willing to participate in production cuts before the kingdom will even consider reducing output.

For the past 18 months, Russia has indicated it isn’t prepared to make output reductions. However, in late January, Nikolai Tokarev, the head of Transneft, the Russian state pipeline company, suggested that Russia and OPEC should talk about joint production cuts to boost prices. This is a significant change in attitude from Russia.

The response from OPEC has been mixed. Venezuela, in desperate economic straits, has been enthusiastically supporting Russia’s offer. Iran, just emerging from sanctions, has no interest in cutting output as it is trying to recover lost market share. The Saudis have no interest in cutting production if it only allows other producers to take market share. Within Russia, the heads of the oil producers, Alexey Miller at Gazprom (GAZP, RUB 131.01) and Igor Sechin at Rosneft (ROSN, RUB 273.10), oppose production cuts.

We suspect that Putin is floating a trial balloon to gauge the reaction from oil producers. We doubt Tokarev would have made his comments without clearing them with Putin first. Thus, we believe Russia may be open to a deal that will boost prices. Of course, that may require Putin to change the minds of some powerful people.

Shoring up fiscal balances: The Russian budget was based on oil prices at $50 per barrel; with prices well below that level, Putin is trying to find ways to boost revenues and cut costs. The estimated budget gap for 2016 is $37.5 bn. He is investigating a number of methods to improve the fiscal situation. These include:

- Asset sales: Putin is floating the idea of selling off parts of the major state-owned industries, hoping to raise around $12.5 bn. However, there are major obstacles to selling state-controlled firms. First, these firms are controlled by members of the elite who don’t want to see their power diminished by new owners. Second, to maximize the value of these firms, foreign buyers will be necessary. Putin has “flip-flopped” on the foreign ownership issue, initially indicating that only Russians will be allowed to buy into these strategic assets, then suggesting that foreigners might be allowed to participate. Under current conditions, it would take a brave foreign investor to participate in such sales and thus it would be a surprise to see these shares sold at anything but fire sale prices.

- Foreign loan cuts: Russia’s Deputy Finance Minister Sergei Storchak said in mid-January that Russia may discontinue foreign lending programs. During the high oil price years, Russia has lent money to nations for diplomatic reasons. The loans are rather inexpensive ways to boost Russia’s global influence and the signal being sent is that economic conditions have deteriorated significantly.

- Return of Alexei Kudrin: Kudrin was finance minister from 2000 to 2011. He was known for his prudent financial management but was not well liked by the elites from the security services. Even though he was forced out of government in 2011 for opposing increases to military spending, Putin still consults with Kudrin on a regular basis. At the end of 2015, reports began to circulate that Putin was negotiating with Kudrin to return to government. Kudrin would bring a degree of orthodoxy to Russia’s fiscal situation, which would be opposed by most of the elites currently in the Kremlin. Thus, bringing him into government would signal that Putin is serious about reforming the Kremlin and improving the fiscal situation.

Ramifications

These actions all suggest that Russia is in serious economic trouble and Putin is struggling to contain the damage. We expect Putin to survive but he will need to take dramatic steps to improve conditions. Although the Obama administration is often criticized for its policies with Russia, time is actually on the side of the U.S. In fact, the administration should promote policies designed to keep oil prices lower for longer. No one should forget that low oil prices and foreign military adventures combined to bring about the dissolution of the Soviet Union.

On the other hand, we expect that Putin will move more decisively than Obama and so we would anticipate that, one way or another, Putin will manufacture a rise in oil prices. This may come through an OPEC deal or a geopolitical event in the Middle East. Although oil prices face seasonal pressure into early spring, we would not be surprised to see prices recover later this year and Russia will probably have a hand in their recovery. Simply put, the best way to address the weakness in the economy and deteriorating fiscal situation would be through higher oil prices.

Bill O’Grady

February 8, 2016

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

Confluence Investment Management LLC

|

1 http://www.bild.de/politik/ausland/ukraine-konflikt/russia-finances-donbass-44151166.bild.html

2 Sergun passed away on Jan. 3 under suspicious circumstances.

© Confluence Investment Management