Consumers confound

Beset by a slow recovery, the prospects and spending patterns of the US consumer have been anything but certain since the global financial crisis. Wage growth, which has seen solid recent gains, seems poised to increase further as the labor market tightens and oil prices remain relatively low.

Still, there are vexing factors, including a geopolitical crisis, another stock market tumble or political uncertainty, that have the potential to derail consumer sentiment. While the outcome of the US presidential election is far from predictable, Super Tuesday should help to narrow the political field and provide some clarity on which candidates may become the nominees. We will need to follow the situation closely given the vital role that the consumer plays in the US and global economy.

I've talked and written a lot lately about the impact of the US consumer and the somewhat slow and uneven spending recovery. Bolstered by low unemployment and solid wage gains, consumers have been less like a tightly coiled spring and more like a Slinky—the popular children's toy that could travel down stairs at a relatively moderate speed but slow at each step to compress and then uncoil once again.

This is similar to the uneven and hesitant recovery we've seen for the consumer during the past few years, where spending has picked up only to slow. But after a lackluster fourth quarter, we’re seeing tentative signs that the consumer may be on an upswing yet again.

Wages up, confidence down

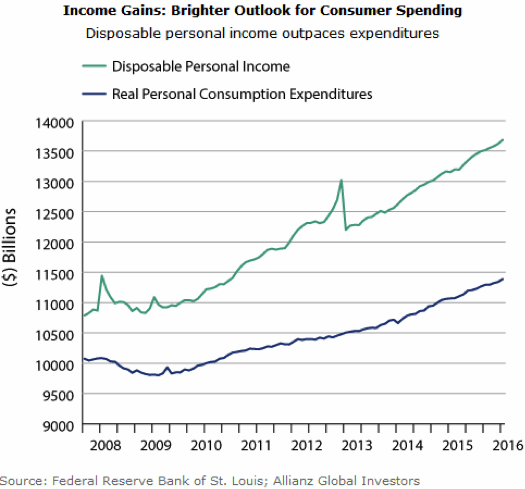

Pointing to a healthier consumer environment are January’s income and spending figures. Real consumption rose 0.4%, with spending for durable goods rising 1.2%. In particular, there was a substantial increase in motor vehicle purchases. So there is good evidence consumers are spending—it’s just that they are spending differently and more selectively than they did before the global financial crisis.

What’s more, the savings rate remained a solid 5.2%, suggesting that consumers are still bolstering their personal balance sheets rather than using that money to finance spending. Instead it seems consumers are capable of increased spending because, in addition to benefiting from lower oil prices, they are being paid more. Wages and salaries actually rose 0.6% in January—continuing a trend of solid gains that we’ve seen in the past few months.

Some would argue that all is not well with the consumer given that, according to the Conference Board, consumer confidence in February has fallen to an eight-month low. However consumer confidence has historically fluctuated, influenced by recent news flow, and could have been knocked lower by the stock market sell-off in January. If the current stock market pickup continues, we will probably see sentiment move higher.

Income and asset inequality

While US consumers in general are experiencing a recovery of sorts, there are admittedly significant flaws. There is a growing level of both income and asset inequality in the US, which is evidenced by the widespread popularity of Bernie Sanders and Donald Trump. This speaks to the growing feeling of disenfranchisement on the part of many Americans who express that they have been “left behind,” making them less likely to spend. However, that does not change what we’re seeing in general, which is improvement in incomes, spending and saving.

The bottom line is that consumer spending has the potential to drive GDP growth higher this year. In an environment where it is difficult to sell US goods abroad because of the strong dollar, a robust American consumer is even more important. Already we have seen the Atlanta Fed’s forecast for first quarter real consumer spending growth increase from 3.1% to 3.5% (annualized) just based on January personal income and outlays.

And on a recent earnings call, a major US transportation/delivery company, whose business is looked upon as a bellwether for growth, explained that it expects higher US GDP growth in 2016, led by “gains in consumer spending in the near term.” Continued growth in consumer spending could become a powerful engine—if it continues through the year.

Moreover, a resolute US consumer and a better overall economic outlook would suggest that the Fed will be on track to raise rates again. However, that means investors may soon return to guessing interest rate trajectories between the market and various “Fed dots,” which look to bring only more uncertainty in very eventful 2016.

Subscribe Today

The Upshot is available as a subscription for financial professionals only. New issues will be delivered via email every Monday. Visit us.allianzgi.com/theupshot to learn more.

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

About the Author

Kristina Hooper is the US Investment Strategist and Head of US Capital Markets Research & Strategy for Allianz Global Investors. She has a B.A. from Wellesley College, a J.D. from Pace Law, a master's degree from Cornell University and an M.B.A. in finance from NYU, where she was a teaching fellow in macroeconomics.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

A Word About Risk

Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

There is no guarantee that an active manager’s investment decisions and techniques will be successful. It is possible to lose some or all of your investment using active management.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

AGI-2016-02-29-14636

© Allianz Global Investors Distributors LLC