Global trend GDP growth continues to decline and, based on our estimates, is currently at around 5% only in USD terms. After years of extreme monetary policy stimulus around the world, including 600 rate cuts since the beginning of the Global Financial Crisis (GFC) and massive liquidity injections and quant easing measures, central bank options may not have totally exhausted their ammunition yet. However, there are not too many options left: interest rates are already around zero globally, in some countries (Eurozone, Switzerland, Denmark, Sweden) they are even negative and central banks’ balance sheets have ballooned. Base money as a share of Gross Domestic Product (GDP) has roughly tripled since 2008 in the US, Eurozone, UK and Japan. Interest rates could go down further – the zero lower bound is clearly below zero – and more rounds of Quantitative Easing (QE) are possible. However, current monetary policy already takes central banks into uncharted territory. Also, the marginal impact of monetary policy on growth is declining already. In addition, increasing the massive monetary stimulus or merely maintaining it for too long comes at a cost as well: it raises the risk of misallocation of resources, higher inflation down the road, or the creation of asset and credit bubbles and, hence, of financial instability. Also, in a zero interest rate environment, central banks lack the opportunity to cut interest rates by at least 2 percent in real terms, as historically required, if and when their economies fall into recession again in the future. Hence, voices calling for alternative policy options, i.e. for fiscal stimulus, as for instance expressed by the International Monetary Fund (IMF), come as no big surprise. Actually, fiscal easing has recently been used as a policy tool in several countries, notably in China as well as in the Eurozone periphery (Spain). Fiscal policy will also be a key topic in the upcoming US presidential campaign.

Nevertheless, is fiscal stimulus really the easy way out from a structural point of view? We discuss the topic in this paper by attempting to answer three interrelated questions. First, are high government debt levels and debt sustainability considerations per se a constraint on fiscal policy? Second, how would bond markets react if government debt levels were to rise because of expansionary fiscal policy? Third, to what extent are legal and political considerations a restriction for more fiscal stimulus?

Government debt levels in the developed world have risen substantially since the beginning of the Global Financial Crisis. In 2007, government debt / GDP was 80%. Eight years on, leverage is almost 50% higher (116% in 2015) and has reached levels similar to those last time seen after the second world war. Excluding Japan, which may be seen as a special case and was not directly impacted by the GFC, does not alter the picture: leverage has increased from 64% to 97% during the same period for major developed economies. This sharp increase in sovereign debt is fully in line with historical experience: as Reinhart and Rogoff have shown, government debt tends to rise, on average, by even more than 80% once a debt financed real estate bubble bursts.

On the other hand, current government leverage ratios in emerging markets are much lower – around 45% relative to GDP – and only around half the level we saw there in the late 1980s and early 1990s. However, this number is definitely understated and also likely to increase significantly in the coming years: firstly, many bonds issued by state-owned enterprises (SOE) in emerging markets enjoy explicit or implicit government backing, which does not show up in official sovereign debt numbers. Secondly, as explained in our paper “Is easy monetary policy fuelling new economic imbalances and credit bubbles?”, many emerging markets, especially China, Brazil, Turkey, Thailand and Russia, have gone through a major private sector re-leveraging, leaving private sector debt significantly above the long-term trend. Too much private debt has already been weighing on growth for a couple of years (e.g. China’s nominal GDP growth has come down from around 20% in 2011 to 6% in 2015) and growth will likely remain low for longer. As economic history shows, public sector debt typically tends to rise in response to a slowdown in economic activity once the credit boom has come to an end. Thirdly, low commodity prices are putting enormous pressure on public finances in emerging markets, which are net commodity, especially oil, exporters.

Why do we care about public debt levels anyway? Because they are likely to be relevant for the growth outlook as well as for debt sustainability considerations.

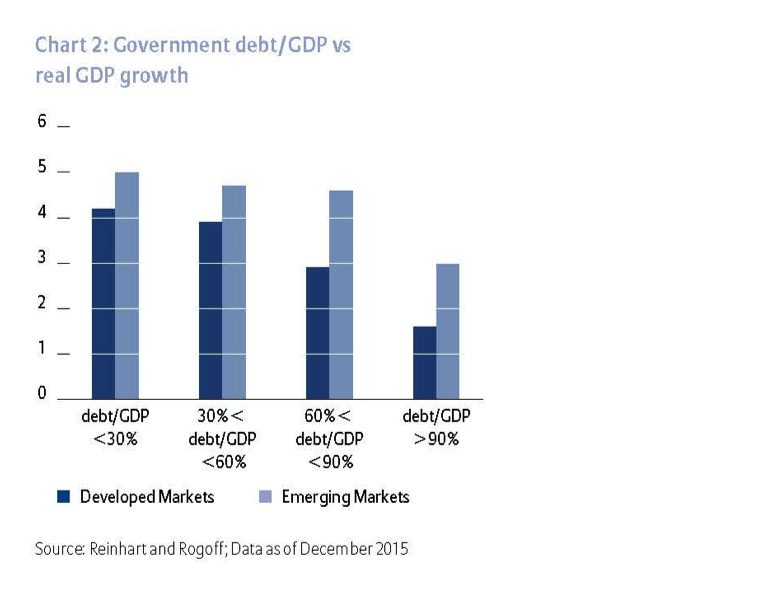

There is a vast body of research showing that countries with high government debt/GDP ratios tend to have lower economic growth rates, both in the developed as well as in the emerging market world. A leverage ratio of around 90% seems to be the critical threshold.

It is an unresolved debate as to whether the causality runs from high leverage to lower GDP growth rates, a view Reinhart and Rogoff are leaning at, or the other way round, i.e. that high public leverage ratios merely reflect weak economic activity. There is evidence for both. In any case, countries in which governments manage to reduce their leverage ratios tend to grow more strongly than countries where government leverage is rising. Hence, a debt financed fiscal stimulus is probably a bad idea from an economic growth perspective in the developed world, given the existing high debt levels and, in particular, if leverage ratios continue to rise as a consequence of a debt-financed fiscal stimulus.

Which stimulus measures are likely to improve growth the most and increase leverage the least? Among the various options available to governments, public investment, rather than tax cuts, transfers, or government consumption, tends to have the biggest impact on growth. Still, on a one year or two years horizon, the incremental increase in GDP is unlikely to exceed the initial investment, i.e. the growth multiplier of public investment is smaller than one, as empirical work by academics shows. In other words, leverage is likely to rise initially, if the investment spending is debt financed. Over a multi-year horizon, though, the multiplier may indeed exceed one and GDP could indeed outgrow the initial investment. Intuitively, this makes sense, as public investment not only increases demand, but, ideally, also the supply conditions in an economy. However, this positive development is not a given. If bond yields increase by too much in response to the stimulus, private demand may actually be crowded out. In addition, there is always a risk that public investments are not carried out in an effective way. The risk of building “roads to nowhere” is particularly high in emerging markets, but certainly exists in the developed world, too.

Still, there are clearly limits to what public investment can achieve. Just have a look at Japan, where public investment has been running in excess of 5% in the second half of the 1990s and above 4% ever since – significantly higher than in other developed economies. In spite of this, growth has continued to slow. For sure, the Japanese growth trajectory could have been weaker without public investment – we don’t know the counterfactual – but even a massive fiscal stimulus over two decades has not prevented the economy from sliding in nominal terms, as the economy went through a balance-sheet recession. A similar pattern can be observed in emerging markets: government-led investment spending has been rising for ten years or so already, without preventing trend growth from coming off sharply since the beginning of this decade.

In conclusion, public investment is the preferred option to stimulate growth fiscally, notably in the developed world, where public investment has been on a declining trend for decades, down from around 4% of GDP on average to 2.8% currently. However, there is no guarantee that growth picks up in response to public investment in the medium term, if structural headwinds are too strong, and that public sector leverage falls.

In any case, fiscal stimulus measures are easier to carry out, both from a political as well as economic point of view, when public finances are in good shape, i.e. when public leverage is sustainable and not on an explosive path. Debt sustainability actually depends on three factors: a) the initial debt level as a share of GDP, which is high in the developed world currently, b) actual government funding costs – low at this juncture – and c) nominal GDP growth, as this is the key driver for tax income and government spending. GDP growth is low globally.

When carrying out a debt sustainability analysis under various scenarios, we come to the conclusion that, with the exception of Germany, essentially none of the major developed economies would be in a position to implement debt financed fiscal stimulus measures without increasing already high leverage ratios, despite the currently very low sovereign funding costs. For instance, the US would need an almost balanced primary budget just to stabilize its debt/GDP ratio, which is currently slightly above 100% of GDP, under the assumption that trend growth remains unchanged at the average rate of the last ten years, which is around 3.4%, and that the Treasury’s funding costs stay at current levels (around 3.5%). A balanced primary budget does not sound too ambitious, however, and it would require the US government to cut spending or increase taxes by around 1% of GDP compared to what is currently planned for 2016. Even assuming a more generous growth outlook, taking the OECD estimate for nominal trend growth of 4.4%, the picture is almost the same: sovereign debt is likely to stabilize under the current budget plans, while further fiscal stimulus would lift the government leverage ratio again.

The situation is only marginally better in the UK and France. Germany, on the other hand, could afford to spend an extra 1.5% of GDP p. a., around 50 bn Euro, and still be in a position to stabilize its government debt/GDP ratio, which is below 70%. As it happens, the strong influx of around 1 million refugees in 2015, which continues in 2016, is likely to lead to an extra and unplanned government spending of up to 20 bn per year. Japan is the other extreme case: even though the government can finance itself in the market at yields below 1%, its debt levels are on an explosive path. This is the result of its huge leverage of around 2.5 times GDP and of an economy which has been declining in Yen terms for years. Japan is still running a primary deficit of above 3% in the coming years, but would require a surplus just to prevent its debt ratio from rising further. Alternatively, it would take nominal GDP growth to rise to more than 2% for leverage to at least stabilize. Luckily, the government can rely on a buyer of last resort of its JGB issuances: the Bank of Japan. The BoJ is already swallowing around 100% of its new net issuances and its stock of sovereign debt will rise in 2016 to around 40% of all outstanding government debt. We expect the BoJ will need to provide more government debt financing in the future. In other words, Japanese monetary policy is characterized by fiscal dominance. Italy is a special case: it has a long tradition of generating a primary surplus and, hence, should be in a position to achieve a stabilization of its government debt ratio. However, it would take a significant improvement in the medium term growth outlook – nominal GDP growth to rise from currently just above 1% to 2.5% nominal – for the debt ratio to decline. Possible, but surely not easy to achieve.

Among the largest former programme countries in the Eurozone periphery, Spain, Ireland and Portugal will need to keep their budgets under control if sovereign debt ratios are to stabilize – or see trend nominal GDP growth rise significantly from here (by 2 to 2.5% points). There is clearly little to no leeway for further stimulus unless the three countries accept higher sovereign leverage ratios. Greece is the odd one out: with government leverage close to 200% and despite enjoying funding costs just north of 2% thanks to subsidized life-lines from the EU, ECB, ESM and IMF and despite a primary surplus in the region of 4%, even halting the rise in sovereign debt/GDP ratios is still very difficult for the country. Based on our estimates, Greece would have to generate a primary surplus of around 6% p. a., not just the 4% estimated for 2016. Historically, hardly any country has managed to achieve this in Europe over a multi-year period, with Belgium in the years 1997 to 2002 being the exception. Greece will, hence, either continue to rely on external support, or borrowers will have to accept a haircut. The Greek debt crisis obviously has not been solved, only postponed, when a deal was reached in July of last year. While an extension of the current Greek financial support is definitely possible, it is not a done deal: the renegotiations may start at a time when European governments have to deal with other, more pressing topics with potentially huge fiscal and political consequences, i.e. the refugee crisis.

In sum, from a debt sustainability point of view, we find little scope to ease fiscal policy for most governments in the developed world.

This brings us to the second aspect: how would bond markets react to an eventual rise in government leverage ratios as a consequence of fiscal easing? For developed economies, the answer is quite simple: as long as a government issues debt in its “own currency”, bond markets can live with higher government debt ratios. That is to say, sovereign debt needs to be denominated in its domestic unit of exchange and the domestic central bank needs to act, de facto or expected by markets, as a buyer of last resort of sovereign paper if necessary. This has clearly been the case in the US, the UK and Japan since the Global Financial Crisis. Bond yields for UST, Gilts and JGBs have fallen even though government debt ratios have increased substantially since 2008 in all three countries. In the Eurozone, the situation has been more complex. While basically all sovereign bonds are issued in Euros, no government can rely on its “own” central bank: the ECB is a central bank, which pursues monetary policy for a country, which “does not exist”, as it carries out monetary policy for the median or average member of the currency union, rather than targeting individual countries. Hence, markets could not rely on the ECB as a back-stop in the early years post the GFC. Consequently, until mid-2012, there was a clear positive correlation in the Eurozone between changes in sovereign debt/GDP ratios and bond yields. Draghi’s “whatever it takes” pledge changed things, as markets could then anticipate that the ECB would step in via its OMT programme (Outright Monetary Transactions), once a country formally received financial assistance via the ESM (European Stability Mechanism). The ECB has de facto become the back-stop for sovereigns. Consequently, yields have fallen in the periphery over the last more than three years. Will this mechanism remain in place going forward? For US, UK, and Japan, there is no reason to believe anything would change any time soon. For the Eurozone, too, we have no indication for the ECB to change policy. However, there is no guarantee that the current boundaries between monetary and fiscal policy will forever remain as fluid as they are currently.

Even if governments can rely on central banks buying their sovereign debt, it does not imply that financial markets would not at all be affected. A combination of both loose monetary and fiscal policy would trigger a weaker currency and, as a consequence, better exports and also higher inflation numbers. As Japan experienced over the last two years, however, this strategy does not necessarily lead to higher final domestic demand, as higher import prices may simply be akin to a tax hike for consumers and companies. In addition, such a beggar-thy-neighbour policy is likely to lead to currency wars.

In emerging market bonds, sovereign debt levels are of secondary importance only. What really matters at this juncture is the medium-term growth outlook and, in that respect, the outlook on commodity prices, the USD as well as the level of private sector leverage. As outlined above, government debts are expected to rise as a consequence of structural growth issues.

What about legal constraints for fiscal policy, notably for a debt financed fiscal stimulus? De jure constraints are, by their very nature, also political constraints that reflect the views of the majority within a society: new laws can be passed, existing ones amended, exceptions to adhere to existing rules granted. The discussions on the US debt ceiling in October 2015 and the ultimate last-minute agreement in the Congress are a classic example.

The set-up is more complex in the Eurozone, though. Rules governing fiscal policy need to be and actually are stricter in the monetary union as opposed to, for instance, the US, a country with an “own” central bank. The Stability and Growth Pact sets maximum government debt levels (60% of GDP as well as the adjustment path if a country exceeds this level), budget deficits (3%) as well as an upper limit for the medium-term target for the structural, i.e. cyclically adjusted, budget deficit (0.5%). Several more rules are governing fiscal policy within the Eurozone. Not all countries are in compliance with existing rules, though. On paper, this leaves little room for maneuver to carry out major fiscal stimulus measures in the Eurozone currently.

What are the chances of individual countries circumventing current rules? France, for instance, is already pushing for permission not to meet the deficit constraints (again), arguing that the increased terrorist threat following the atrocities in Paris on November 13 2015 requires increased fiscal spending to bolster national security. The refugee crisis may also be used as an argument going forward by some countries to deviate from existing deficit or debt limits. In a currency union, with conflicting political interests, however, it will be much more difficult to achieve an agreement on changes to the existing legal framework as governments of fiscally sound countries may not be inclined to accept a softer stance on fiscal discipline, in particular as they already felt the political heat domestically in mid-2015 when agreeing on a debt deal for Greece. Hence, we would argue that, politically, major fiscal stimulus measures will be difficult to implement in the Eurozone at this juncture.

What are our conclusions? Fiscal policy may continue to be used by policymakers to stimulate growth in the current environment of nominal growth. However, we think fiscal policy is no panacea either. The positive impact on growth is far from sure, if governments are highly leveraged as is the case in the developed world right now. The government leverage ratio may even rise further from current levels in response to a debt financed stimulus measure. While bond markets may not be overly shocked by that, as long as central banks stand ready to be a lender of last resort to governments, currencies are likely to respond. Hence, we think structural reforms are the more promising alternative to stimulate growth in the medium to longer term. This is especially true in the Eurozone, where calls for fiscal stimulus measures would surely make current political discussions even more complicated and would face difficulties in getting broad based acceptance. They may, in a worst case scenario, put further pressure on the political cohesion in Europe at a time when it is badly needed.

References

Batini N., Eyraud L., Weber A. “A Simple Method to Compute Fiscal Multipliers”; IMF Working Paper WP / 14 / 93, June 2014

ECB, “The Role of Fiscal Multipliers in the Current Consolidation Debate”, Monthly Bulletin 12/ 2012

EU Commission, European Economic Forecast – Autumn 2015, Statistical Annex

Financial Times, “Alarm raised over $800 bn of camouflaged sovereign debt”, 6 January 2016

Hofrichter, S., “Is easy monetary policy fuelling new economic imbalances”, Allianz Global Investors, 10/2015

IMF World Economic Outlook, October 2014, Chapter 3: “Is It Time for an Infrastructure Push? The Macroeconomic Effects of Public Investment”

IMF World Economic Outlook, October 2014, Statistical Annex

Leandro A., Bruegel Institute, “France and Italy: The ABCs of the European Fiscal Framework, 2015

Pescatori A., Sandri D., Simon J., “Debt and Growth: Is There a Magic Threshold”, IMF Working Paper WP/14/34, February 2014

Reinhart C., Reinhart V., Rogoff K., “Debt Overhangs: Past and Present”, NBER Working Paper 18015, April 2012

Reinhart C., Rogoff K., “This Time Is Different”, 2011

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

About the Author

Stefan Hofrichter, CFA, is the Global Head of Strategy and Economic Research for Allianz Global Investors. He has a degree in business administration from the University of Applied Sciences of the Deutsche Bundesbank, Hachenburg, and a degree in economics from the University of Konstanz.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

A Word About Risk

Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

There is no guarantee that an active manager’s investment decisions and techniques will be successful. It is possible to lose some or all of your investment using active management.

AGI-2016-03-08-14690