Last week saw terrorism strike two more cities with the tragic attacks in Brussels and Lahore. Our hearts go out to the victims, their families and all the people of Belgium and Pakistan. Sadly, in the past few months we’ve seen terrorism deliver multiple blows to humanity. And the reality is that there have been far more terrorist attacks than just the ones that have received significant media attention. In the past few months we’ve seen some incredibly brazen and cowardly attacks around the world—some of which involved the targeting of children. This begs the question, “What is the cost of terrorism?”

Trying to calculate the incalculable

This is such a difficult question to answer as there are so many different costs of terrorism, from psychological to economic to political to human lives, which is of course incalculable. In terms of economic costs, there are the direct ones: the value of property damage and the cost of death and injury, including medical care and lost earnings, which is how the Institute for Economics and Peace calculates the price of terrorism.

For example, the direct cost of the September 11 attack has been estimated by multiple sources at many billions of dollars. The Comptroller of the City of New York estimated the direct cost (both physical and human) at more than $302 billion.

Then there are the indirect costs—the market and consumer responses to the terrorist acts. In the short-term, we typically see a fairly resilient stock market after an initial drop. In the short-term we also see a curtailment in consumer spending, particularly travel—as several airlines reported a significant drop in European travel following the Paris terrorist attacks. Also, several months ago, when a Russian plane appeared to be blown up by a bomb over the Sinai region of Egypt, many flights to the region were cancelled, which in turn resulted in numerous hotel and restaurant reservation cancellations; this was a major hit to Egypt’s economy.

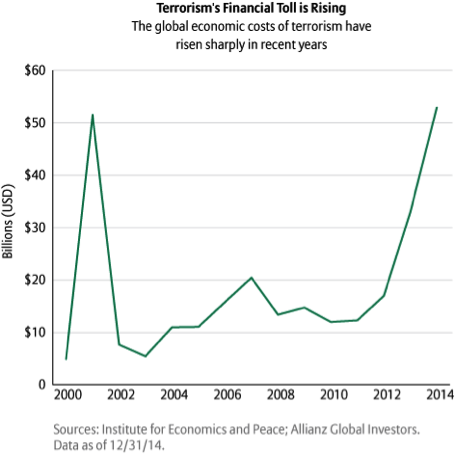

Then there is the government funding to fight terrorism, which should be added to the overall tab. Money is spent on a laundry list of items such as anti-cyberattack software and modelling, an expensive unproductive investment. According to the latest annual Global Terrorism Index produced by the Institute for Economics and Peace, in 2014 terrorist acts cost the world $52.9 billion—a number that has increased significantly over the past decade.

The opportunity cost of anti-terrorism

While increased spending to fight terrorism is a form of fiscal spending that injects money into the economy, we must also recognize the opportunity cost of anti-terrorism spending. That is money that arguably could be spent on endeavors with a higher return on investment, such as education, or it could result in countries taking on more debt that becomes increasingly difficult to service. Also, we typically see measures taken to prevent terrorism result in an increased burden on trade, as additional layers of security at borders add time and costs to the supply chain. We should expect costs to be passed on to consumers, with added supply-chain costs and other anti-terror actions by businesses likely to create some consumer inflation.

The recent terrorist attacks should also be viewed in terms of their ability to influence political developments. For example, the Paris and Brussels bombings could have a significant impact on the UK’s decision on whether to remain part of the European Union. Interestingly, depending on the lens one looks through, these tragedies could either move the UK closer to, or further from, the European Union. On one hand, it could cause the UK to believe it can benefit from participation in the EU as clearly information sharing among countries is a critical part of being able to stop terrorism.

Alternatively it could cause the UK to believe it needs to leave the European Union in order to secure its borders; after all, in such a structure one is only as strong as its weakest link. And political ramifications of terrorism are not confined to Europe; the US presidential election could be significantly impacted by heightened terrorism concerns on the part of the electorate.

Can stocks continue to shrug-off?

So while stocks have heretofore largely shrugged off terrorist attacks, it does not mean that terrorism is inconsequential. Beyond the obvious and horrific human costs, the economic and political costs are very significant. Looking ahead, because of the geopolitical uncertainties ranging from Algeria across to Afghanistan and from Azerbaijan down to Somalia, we could see terrorism become both more frequent and possibly more dramatic.

Headlines will create volatility for the markets as well as possible gyrations in oil prices, given that many of the countries impacted by terrorism are also some of the largest producers of oil. Finally and unfortunately, many of these uncertainties seem to be difficult to resolve and so could last much longer.

Subscribe Today

The Upshot is available as a subscription for financial professionals only. New issues will be delivered via email every Monday. Visit us.allianzgi.com/theupshot to learn more.

Follow Us on Twitter

For more investment insights and market perspectives from our global research network, follow @AllianzGI_US on Twitter or visit us.allianzgi.com.

About the Author

Kristina Hooper is the US Investment Strategist and Head of US Capital Markets Research & Strategy for Allianz Global Investors. She has a B.A. from Wellesley College, a J.D. from Pace Law, a master's degree from Cornell University and an M.B.A. in finance from NYU, where she was a teaching fellow in macroeconomics.

Important Information

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

A Word About Risk

Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

There is no guarantee that an active manager’s investment decisions and techniques will be successful. It is possible to lose some or all of your investment using active management.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1 800 926 4456.

AGI-2016-03-28-14800

© Allianz Global Investors Distributors LLC