Global Economic Perspective: April

Fed Surprises with Dovish Stance amid Mixed US Economic Data

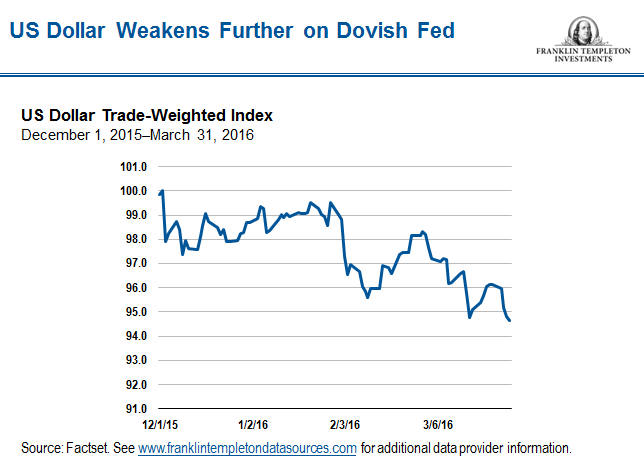

US economic data produced somewhat mixed signals in March, with the weaker indicators leading to a reduction in consensus forecasts for first-quarter 2016 growth. But, as had been the case in February, there was also enough resilience in the numbers to allay concerns about a more prolonged slowdown. The major surprise during the month was the extremely dovish stance of Fed Chair Janet Yellen, which placed far greater weight than had previously seemed the case on external factors, including the slow pace of global growth and recent financial market volatility, and led to a sharp pullback in the US dollar as investors concluded US policy rates would remain lower for longer.

Our viewpoint on the economy is that the underpinnings for the US consumer remain solid, and we expect growth to return to more elevated levels later in 2016. Given our relatively positive outlook, we have some apprehension about the Fed’s latest signals on monetary policy, which in our view may place too great a focus on global factors, despite a relatively tight US labor market and some indications of a pickup in core inflation.

February’s personal income and spending report pointed to a slightly softer start to the year for the consumer than previously thought. Though spending for February came in modestly higher than expected, there was also a large downward revision to January’s data, from 0.5% to 0.1% month-on-month (m/m), while February’s fall in wages and salaries was the first since September. However, the US labor market, far from showing signs of faltering, once more provided evidence of a healthy underlying economy, with nonfarm payrolls coming in higher than consensus expectations, up 215,000 m/m for March. A further uptick in the labor force participation rate to 63.0% explained a slight increase in the unemployment rate and underlined how slack in the labor market was gradually being used up. Average hourly earnings also beat estimates with a gain of 0.3% m/m, though the annual rate remained subdued at 2.3%. There was also a sign consumer spending might soon start to pick up again, as the Institute for Supply Management’s (ISM’s) non-manufacturing purchasing managers’ index (PMI) showed a strong rise to 54.5 in March from 53.4 a month earlier.

Other data painted a similarly diverse picture. In manufacturing, the ISM’s manufacturing PMI for March came in above the 50 level that signifies expansion for the first time since September 2015, with the new orders component rising to its highest level since 2014. While the ISM release hinted that exporters might start to see the benefits of the US dollar’s current weakness, a decline in manufacturing employment in the labor report for March illustrated the effects of the currency’s previous strength. For trade, February’s data revealed the largest deficit for six months, indicating net exports would probably hold back first-quarter gross domestic product (GDP) growth, although the rise in imports was given a positive spin by the strong demand seen for consumer goods and a gain in services.

Overall, we feel the data remain encouraging. While the labor market may tail off a little from its robust performance of recent months, its underlying state for this stage of the business cycle is impressive, in our view, and should provide a solid foundation for growth to pick up again after a couple of sub-par quarters. Even manufacturing, a dampening influence in recent times, may be starting to show signs of recovery. While earnings are taking longer to reflect tightening labor market conditions than might have been anticipated, our view is that ultimately this strength should be transmitted into consumers’ pockets, fostering a pickup in spending.

With this in mind, the extent of Fed Chair Yellen’s dovishness during the month has been somewhat surprising and a little troubling to us. Markets were taken aback by an increased emphasis on global threats to growth over domestic metrics and consequently downgraded a rate rise in the first half of the year to only a slim possibility. The other justification mentioned by the Fed was so-called asymmetric risk, that is to say the limited policy response available in the event of a downturn, given that interest rates are still close to zero. Less of a surprise was the Fed’s scaling back of its own forecasts for the timing of future rate rises—though these still anticipate two rate increases in 2016—since these were already far in advance of the slower pace reflected in market consensus estimates.

A relatively benign reading in February for the Fed’s preferred measure of inflation may have encouraged its more dovish assessment. The core personal consumer expenditures (PCE) price index slowed from 0.3% to 0.1% m/m, while the annual rate remained at 1.7% year-on-year. But core consumer price data were firmer, with a 0.3% m/m February reading pushing the annual number up to 2.3%, significantly above the Fed’s target of 2%.

Nevertheless, we retain a slight unease that the Fed may be tilting too far in one direction when assessing the inflation part of its dual mandate. With its median March projections for the longer-run normal rate of unemployment at 4.8%, its mandate on employment appears close to being fulfilled, suggesting little slack in this area, even if for the moment wage inflation remains muted. Though core PCE was stable in February, it remained at its highest annual rate in three years. The additional boost the economy has received in the last month in the wake of the Fed’s increased global concerns should not be overlooked either, with a fall in long-term interest rates and a weaker US dollar acting as further stimuli, which may add to inflationary pressures further down the line.

Slower Growth in the Global Economy, but Markets More Stable

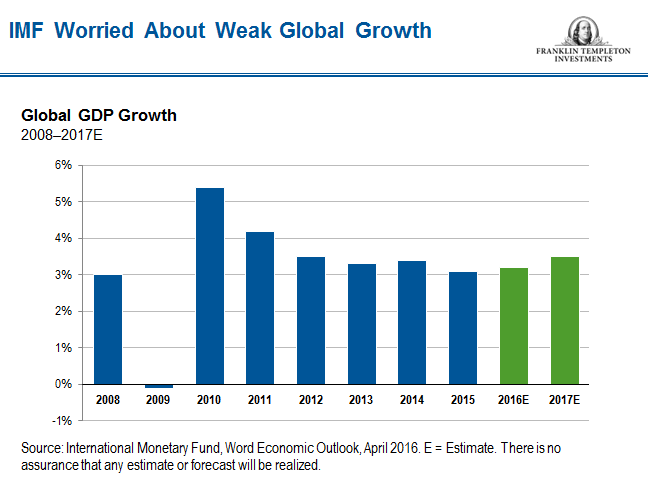

One reason for the Fed’s caution may have been a concern about appearing out of step with the direction of interest rates in most of the rest of the world, where slower growth meant the likely trajectory of monetary policy still appeared downward. International Monetary Fund Managing Director Christine Lagarde described the threat of an era of weak expansion as the “new mediocre,” and she urged more support from governments through structural and fiscal measures.

However, data from China, the source of much anxiety among investors so far this year, improved somewhat over the month. The country’s official manufacturing PMI for March indicated expanding activity for the first time since July 2015, and the equivalent index for services also increased over the month, from 52.7 to 53.8. Profits among industrial companies showed the strongest growth for over 18 months, rising 4.8% on an annual basis over January and February, helped by additional monetary stimulus and higher government spending on infrastructure projects. The Chinese renminbi continued its rebound from a five-year low reached against the US dollar in January, allowing the country’s foreign exchange reserves to rise in March for the first time in five months, and easing fears about capital flight.

Against the backdrop of a weaker US dollar, other emerging-market currencies also performed strongly, with the Brazilian real posting one of the strongest rises of more than 10% against the US currency in March, as investors seemed to decide that the country’s political and economic crises may have peaked. A further rise in oil prices from their early February lows, another factor tied to US-dollar weakness, boosted the assets of countries that are major producers and helped the Russian ruble to its second biggest monthly gain on record against the US currency. Though the Japanese yen was broadly unchanged against the US dollar during the month, the effect of its recent strength was seen in the quarterly Tankan survey of business sentiment among larger Japanese manufacturers, which fell to its lowest reading since 2013.

India cut its interest rates to a five-year low, despite its economy’s recent strong growth of more than 7% in recent quarters, in an effort to take further advantage of the headroom provided by past falls in energy prices. The Reserve Bank of India has warned that many of the country’s banks are in need of restructuring, in order to tackle a buildup of bad loans that threatens the economy’s ability to sustain the current period of elevated growth.

We feel general perceptions may paint growth in the global economy as worse than it actually is, though the current level of expansion is undeniably sub-optimal. To take China and India as two examples, their real growth rates may well be lower than official estimates but are likely, in our opinion, to remain respectable and well above levels suggested by some of the more bearish analysts. However, in the current uncertain environment, investors’ doubts about the effectiveness of monetary policies may continue for some time, extending a demand for perceived safe-haven assets that could see their prices remain higher than fundamentals would otherwise suggest.

ECB Committed to Pushing up Inflation and Stimulating Lending

European data continued to indicate slow but steady growth, mainly driven by domestic demand that has been bolstered by the ECB’s monetary easing program, though a weaker global outlook and financial volatility provided some headwinds. Germany’s Ifo index of business confidence rebounded from its poor showing in February, while the country’s record low unemployment rate of 4.3% in the same month remained the smallest of any country in the European Union (EU). Despite Spain’s political gridlock, which has left it without a government since December 2015, the country’s economic recovery appeared intact, as the Spanish central bank estimated growth for the first three months of the year had been a solid 0.7% quarter-on-quarter, largely due to household spending and corporate investment. However, as the country’s economy powered ahead, tax cuts prior to last year’s elections led to a deterioration in its fiscal position. The Spanish government revealed that its budget deficit for 2015 had been 5.0%, significantly worse than its target. In the United Kingdom, there were some signs the economy was slowing—probably partly due to the dampening effect of uncertainty ahead of the country’s June referendum on whether to remain a member of the EU—and the UK government lowered its estimate for growth for the current year from 2.4% to 2.0%.

The ECB also slightly trimmed its estimate of growth in the eurozone for the year to 1.4% and noted its inflation forecasts as 0.1% for 2016, 1.3% for 2017 and 1.6% for 2018. The region’s estimated headline inflation rate for March remained below zero for the second consecutive month, though core inflation edged up over the same period. The ECB’s prediction that inflation would take at least three years to reach its target level of 2% underscored why the central bank felt the need to move more aggressively in the monetary easing measures announced in early March, which reinforced its commitment to get inflation back up.

Though the ECB’s latest moves seemed unlikely to impact core eurozone sovereign bonds very much, the package included an extension of the bank’s purchases to encompass debt issued by companies, which in our view is a significant change of policy. Spreads on euro-denominated corporate bonds narrowed in response to the move, in an indication that tight liquidity in these markets could complicate the ECB’s efforts to carry out its purchases, although initially the bank will probably look to target the primary market when it commences buying investment-grade issues in June.

There was some disappointment that the ECB did not add purchases of bank debt to its program, but its reluctance to do so may have been because of its role as regulator of the banks: If a lender got into trouble, the ECB would have to supervise a “bail-in” of that bank’s debt, and owning its debt would represent a large conflict of interest. Instead, the ECB tried to address concerns about the impact of negative interest rates on banking profitability by restricting its cut in the deposit rate to 10 basis points, as well as creating virtually free money for the banks through a new round of TLTROs (Targeted Long-Term Refinancing Operations), which offer four-year loans effectively for zero or even negative rates.

All in all, we think the ECB is doing everything it possibly can for the moment. While the euro’s strength this year has created some unease, we believe such worries are exaggerated, since most of the eurozone’s current growth is being generated domestically. In fact, in our view the outlook for eurozone corporate bonds is now more attractive, given the additional boost to credit conditions for companies and banks that the ECB has put in place in its latest package.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity.

© Franklin Templeton Investments

© Franklin Templeton Investments