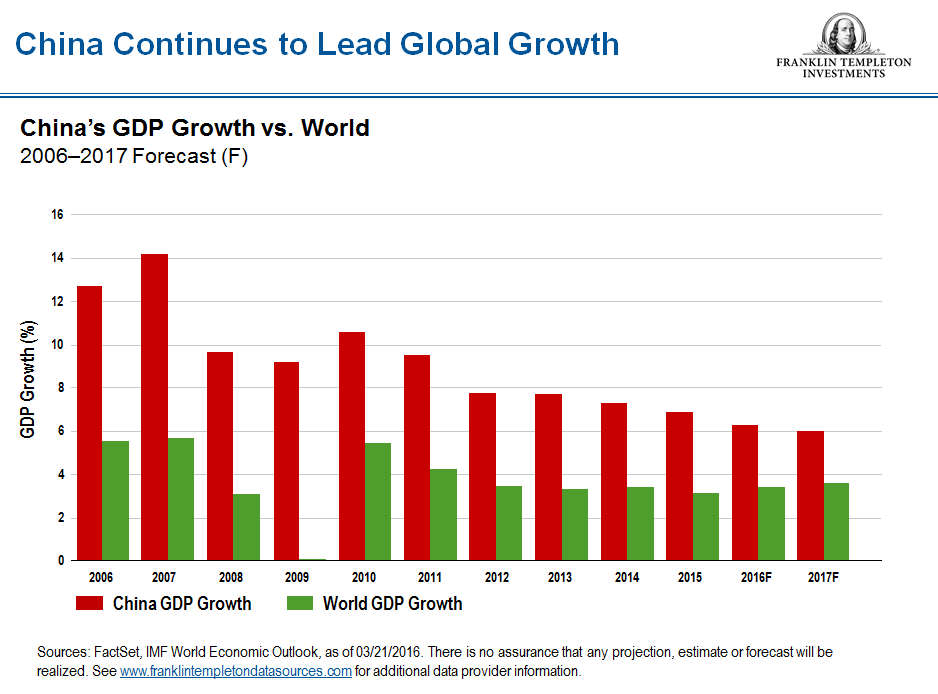

After a long period of outstanding economic growth, many investors are now wondering about the future path of China’s equity market and its economy, with some making doom-and-gloom predictions. Although China’s gross domestic product (GDP) growth is slowing compared with past years, the transformation of the economy from investment- to consumption-driven growth is under way and is going to have tremendous implications for every part of that economy. China’s economic transition—along with incredible economic growth already experienced—has resulted in a much larger economy so that the percentage growth numbers will naturally decelerate going forward. In our view that’s not a reason to panic. The changes aren’t going to happen overnight. The important continued urbanization of the country, which is still behind the urbanization rate of the United States, is moving forward and should have a significant impact. China’s growth rate, while slowing, is expected to continue to outpace global growth by a wide margin, as you can see in the chart below.

Here, I join my colleagues Dennis Lim and Eddie Chow for a discussion about China. Dennis is senior executive vice president and a 25-year veteran of Templeton Emerging Markets Group based in Singapore. Eddie, based in Hong Kong, is senior executive vice president and has been a member of the team for more than 20 years. If you’d like to know more about my recent travels in China, read my blog series covering the cities of Wuhan, Nanchang, Fuzhou, Nanning, Guiyang and Shenzhen. I have found the situation in China, when you see it with your own eyes, is often different than what you read in the popular press.

On China’s Shifting Economy

Dennis Lim

China is an important trading partner for most—if not all—countries around the world, and therefore, it’s an economy widely watched around the world. Recently, we have seen some negative headlines about the health of China’s economy. There have been concerns that Chinese manufacturing is in recession, and that the investment-led growth over the last three decades in China has ended with the need to shift the economy from manufacturing- and investment-led to a services- and consumer-oriented direction. We know that China’s currency, the renminibi (also known as the yuan), continues to be under pressure because of events in the Chinese manufacturing sector. In the fourth quarter last year, we saw a big drop in the value of the renminbi versus the US dollar, but since the beginning of this year, we have seen a sustained recovery in the exchange rate. The government’s crackdown on corruption in China continues, and there’s a theory that it has created some caution on the part of the Chinese consumer because of perceived scrutiny on conspicuous spending. Those who can spend are likely holding back because of a concern that they could be targets of investigation.

Some investors continue to expect a hard landing in China—a rapid shift from high growth to slow/no growth or even recession. They look at the country’s economic statistics and the Chinese government’s announcements with skepticism. We don’t see a hard landing for China, and according to our research and on-the-ground observations, the numbers coming from the National Bureau of Statistics of China seem to be a fairly good indication of where the economy is headed. Credit continues to ease, and one of the repercussions appears to be the housing market, which we think could be showing signs of a small bubble in some areas of the country.

Mark Mobius

There is a lot of debate about China’s GDP numbers and statistics coming out of China in general. I think people have to remember that China is a planned economy and, to a large extent, it can engineer and plan growth to meet specific targets.That means orders from China’s leaders in Beijing go out to the various provinces, cities, towns and villages to obtain a particular growth rate. The regions are thus empowered to make investments to ensure that the growth rate they have been assigned is met. This can, of course, lead to substantial amounts of waste; for example, roads or bridges that shouldn’t have been built and apartments or other buildings that aren’t fully occupied or are empty. But at the end of the day, most of these projects do turn out to be worthwhile. China’s high-speed railways, for example, have been a tremendous boost to the economy—which I’ve been able to experience myself while traveling throughout the country. I believe the Chinese are aware of the problems of not having a fully market-oriented economy, where the allocation of resources is done by the market instead of central planning. Nevertheless, I believe the economic numbers we see out of China are, by and large, no less accurate than what we are getting in many other parts of the world.

Dennis Lim

We recognize that the era of double-digit growth in China is probably over. Going forward, we expect to see growth in the range of 4% to 6%, which isn’t all that unexpected or disconcerting given the tremendous increase in the base of the economy. Single-digit growth rates should be more the norm going forward, in our assessment.

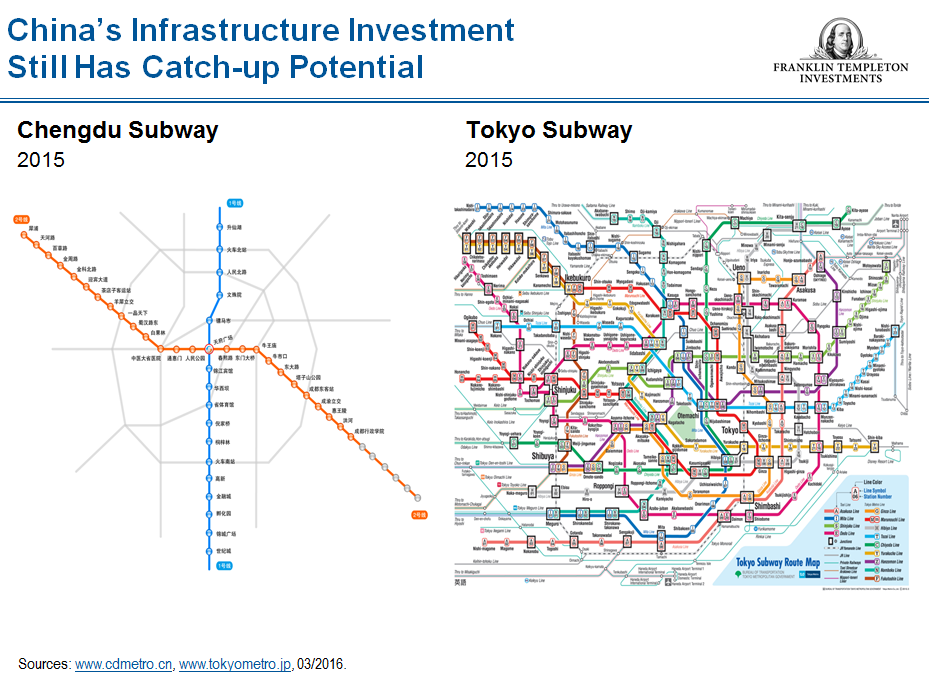

There’s clearly been great investment going into the rail system in China. At the end of last year, there were a total of 121,000 km of railway in China (19,000 of which is high-speed), and the system carried about 2.5 billion passengers in 2015.1 In spite of this very rapid growth in recent years, the railway density of the big Chinese cities is still below that of other large cities including London, Paris and Tokyo. In our view, there’s still a need for more investment in rail.

There is a similar dynamic when comparing the subway systems of China’s major cities with others around the world. For example, Chengdu, a major city in the southwest part of China with 7 million people and a municipality of 14 million, has two subway lines—one going north-south and one going northwest-southeast. Compared to Tokyo, a city of about 13 million, the difference is quite stark. In spite of the very high investments in infrastructure that we have seen in China in recent years, it is nowhere near saturation, so we expect to continue to see investments in areas including rail, roads and ports.

In terms of manufacturing activity, capacity utilization remains low. That’s a real concern for us because of the years of big investments. Railway freight traffic has also reflected a slowdown, and the last two years in particular have been weak. Power generation paints a similar picture. Since the global financial crisis of 2008-2009, there has been a slowdown, and power generation today reflects low-single-digit growth rates, which I think is probably going to persist for the next couple of quarters.

On China’s Equity Market

Eddie Chow

China’s A-share market is large, with more than 2,000 companies listed on the Shanghai Stock Exchange and about 1,000 listed on the Shenzhen and other stock exchanges in China. Quoted in local currency, only residents of the People’s Republic of China (PRC) or those under the Qualified Foreign Institutional Investor (QFII) and Renminbi Qualified Foreign Institutional Investor (RQFII) schemes can trade A-shares, which are considered the “domestic” market. The main characteristic of the domestic market is that it’s dominated by retail investors, so there are often big swings that tend to be tied to short-term investor sentiment rather than longer-term fundamentals. Index provider MSCI has been considering the inclusion of the Shanghai domestic market in its benchmark indexes, and it has even been talking about including 5% of China A-shares’ free float-adjusted market capitalization in the MSCI Emerging Markets Index. MSCI is expected to announce its decision in June 2016, and if A-shares are included, we would anticipate increased foreign investor interest in China’s domestic market.

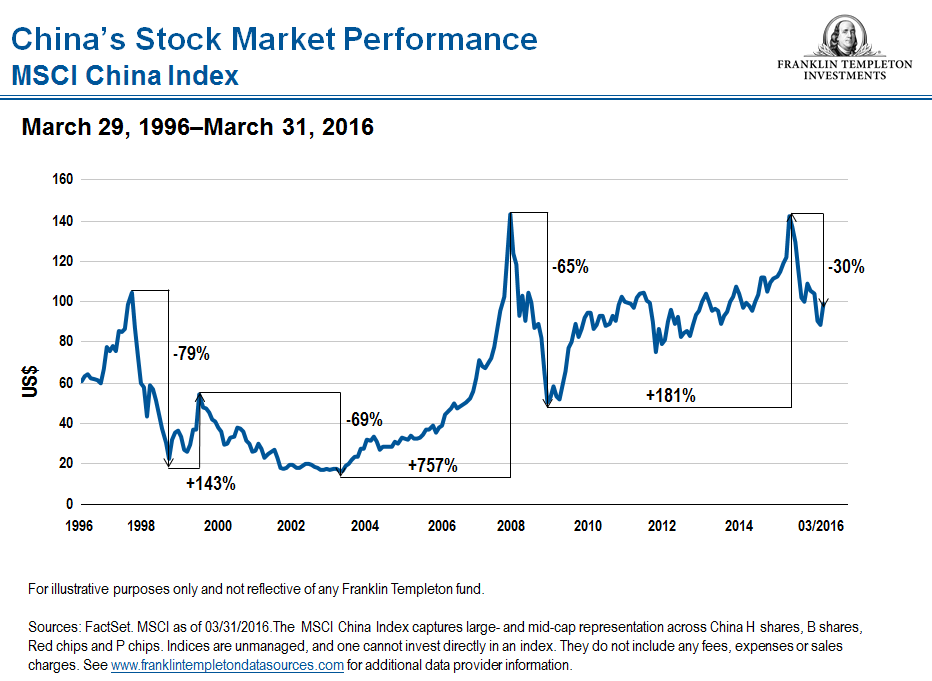

The MSCI China Index captures large- and mid-cap representation across China H-shares (securities of Chinese companies traded in Hong Kong and quoted in Hong Kong dollars), B-shares (securities of Chinese companies that trade on either the Shanghai or Shenzhen stock exchanges and quoted in US or Hong Kong dollars), Red chips (companies outside the PRC traded in Hong Kong, but owned directly or indirectly by mainland Chinese state-entities) and P chips (companies outside the PRC traded in Hong Kong and owned by individuals in mainland China). This is considered the “offshore” market more widely accessed by foreign investors, and like the domestic market, it has been very volatile over the years, as you can see in the chart below.

We currently view the offshore market as very attractive from a valuation standpoint. The price-earnings (P/E) ratio of the MSCI China Index is trading at roughly 10 times, which to us is very attractive by historical standards.2 The price-to-book (P/B) ratio is also trading near historically low levels at about 1.3 times book.3

We see many areas of potential investment opportunity in China, particularly in the consumer sector as the economy continues to transition. China’s automobile market has experienced strong structural growth, including strong sales of luxury auto sales. In 2015, passenger vehicle sales in China were up by about 5%, and forecasters again expect mid-single-digit growth this year.4 The car penetration rate in China remains low when compared with a more mature market like the United States, so we still see good potential for select Chinese companies in this area, as well as select foreign auto makers looking to increase market share in China.

Athletic goods, sportswear and footwear, represent another area of interest to us. The market for sportswear in China can be broadly divided into two major segments: foreign and domestic, with foreign brands typically at higher price points. We are seeing some domestic companies in this space doing a good job penetrating the second-tier and third-tier cities with strong distribution networks. We also are seeing domestic companies tap into the high-end segments through joint ventures with foreign brands who are lending marketing rights. Leisure pursuits are growing in popularity, from soccer (football) to skiing.

On Banking and Corporate Bonds

Mark Mobius

I would like to add a few additional comments about China’s banking system and corporate bond market, where some observers have also expressed concern. There is no question to us that there are a number of companies in China which are overleveraged and that will likely be in trouble—in fact, are already in trouble—and unable to make payments on their loans and bonds. However, the large banks in China are government-controlled and thus have the support of the government in times of stress. China still has tremendous amounts of foreign reserves, and there are many safety valves in place which should enable the banks to meet their obligations to help these companies if need be. So, I don’t think we are going to see a nationwide banking panic, and I don’t think there are going to be mass company bankruptcies. Some of the private companies will likely go under; in fact, it is already happening. But the structure of the society and the basic structure of the financial system will not deteriorate to that significant a degree, in our view.

Eddie Chow

It is true that the Chinese government has a major goal of developing a better bond market; relative to China’s equity market, its bond market is still in its infancy. We have started to see the kind of government-implied guarantee given on some of the state-owned enterprise (SOE)-issued bonds being removed last year, and we have seen the first case of an SOE default on its bonds. We think this is actually a healthy development in the sense that it could help bond investors understand the risk involved in investing in bonds. It is true that we may see more defaults down the road, but I think, in general, they will not be on a scale that will threaten the general liquidity situations of the banking systems or the whole economy. In terms of the general monetary conditions of China’s economy, things still look quite healthy to us. China has a high savings rate, and the People’s Bank of China (PBOC) is very closely monitoring the liquidity situations of the whole system. At times of need, we believe the PBOC will likely inject short-term liquidity into the market. In general, I think the government is looking for ways to help the corporate side deleverage where necessary, and remove excess capacity; it recognizes the need to rejuvenate the banking system so credits can be channeled from weaker to healthier companies. The closure of some of the weaker entities will remove some of the banking system’s problematic bank loans, which are taken care of by the government, without going into outright default. In general, I think the government is looking for ways to help the corporate side deleverage, and so the chance of having a system-wide financial crisis will be very low.

Mark Mobius

I hope Dennis, Eddie and I have cleared up some misconceptions about China and addressed some common concerns. In sum, we believe fears about a banking or economic collapse in China are overblown and that there is still a lot of room for infrastructure growth to catch up to global and regional peers. We still see a lot of potential investment opportunities across different segments of China’s market and believe the currently low valuations of Chinese stocks could reward patient investors over the long term.

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Important Legal Information

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

_____________________________________

1 Source: China Internet Information Center, China.org.cn, January 2016.

2 Sources: FactSet, as of March 2016. The P/E ratio for an individual stock compares the stock price to the company’s earnings per share. The P/E ratio for an index is the weighted average of the price/earnings ratios of the stocks in the index.

3 Sources: FactSet, as of March 2016. For an individual company, the P/B ratio is the current share price divided by a company’s book value (or net worth) per share. For an index, the P/B ratio is the weighted average of the price/book ratios of all the stocks in the index.

4 There is no assurance that any estimate or forecast will be realized.

© Franklin Templeton Investments

© Franklin Templeton Investments