After years of favoring growth and momentum stocks, many equity investors have turned their attention to value-oriented shares so far in 2016, including those of so-called “dividend achievers.” Donald G. Taylor, portfolio manager, Franklin Rising Dividends Fund, explains why he has a positive outlook for the segment going forward. He also provides a short primer on dividend-growth investing.

The US equity market has experienced a sea change this year, as many investors appear to be turning away from the momentum and growth stocks that had buoyed 2015 returns and casting their nets toward other more value-oriented parts of the market, including “dividend achievers.”

Dividend achievers, defined as companies that have consistently increased their dividends for 10 years or longer, have returned 7.73%,1 while momentum stocks have remained flat2 and the overall market has returned 1%.3 We believe investors so far this year have greater confidence that modest global economic growth should benefit a wider swath of companies, particularly those with long-standing business models such as dividend achievers. And we expect the favorable sentiment toward achievers to continue, as more positive news about China’s economy and certain forward-looking indicators appear, in our view, to point to an increase in global growth.

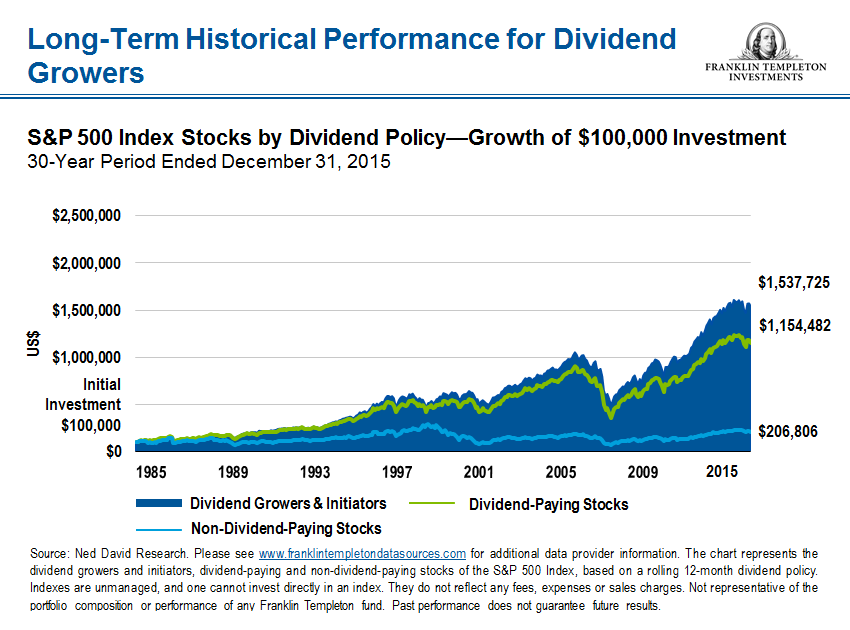

Although most achievers are household names, investment strategies that focus on dividend growers remain a mystery to many investors. I’m often asked why a dividend-focused strategy stresses dividend growth instead of high dividend yields. In my view, quality high-yielding companies that don’t offer much dividend growth are really alternatives to investing in the bond market. Instead, we are seeking capital appreciation, and research suggests that companies that grow their dividends tend to experience greater long-term stock price appreciation than companies that maintain their dividends or don’t pay one at all. (See chart below.) And we have found that a consistently rising dividend tends to be an indicator of solid earnings growth, a resilient business model, and a commitment by management to return cash to shareholders. (Of course, dividends are not guaranteed and can increase, decrease or be totally eliminated without notice.)

Companies that fall under the dividend achiever category are usually leaders in their industries or market niches, and have managements with long, positive track records. A 10-year period of rising dividends is a good gauge of corporate soundness, in our view, because at some point in that 10-year period the company is likely to have experienced a down cycle. Companies that can continue raising dividends during a downturn have displayed some measure of fiscal strength. In our own portfolio, we deviate from some dividend-achiever indexes in that we expect the company to raise its dividend in just eight out of 10 years. This policy gives a company the chance to keep its dividend flat during tough times.

In addition to screening for a history of consistent dividend increases, we require that our holdings have at least doubled their dividends over the previous 10 years, have what we consider strong balance sheets and reinvest their earnings for future growth. And, as value investors, we purchase shares of companies at what we believe to be opportunistic prices.

Sector Switch

Since the financial crisis of 2008-2009, we have seen a much broader, more diverse group of companies qualify as dividend achievers. Before the crisis, financial companies dominated the category, but in the midst of the crisis, many banks cut or eliminated their dividends. Many in the financial sector have since recovered and have been consistently growing their dividends, but it will be a few years before they have a decade-long record of increases under their belts again. Meanwhile, companies in other sectors, including technology, initiated dividend programs in the early 2000s and eventually became achievers.

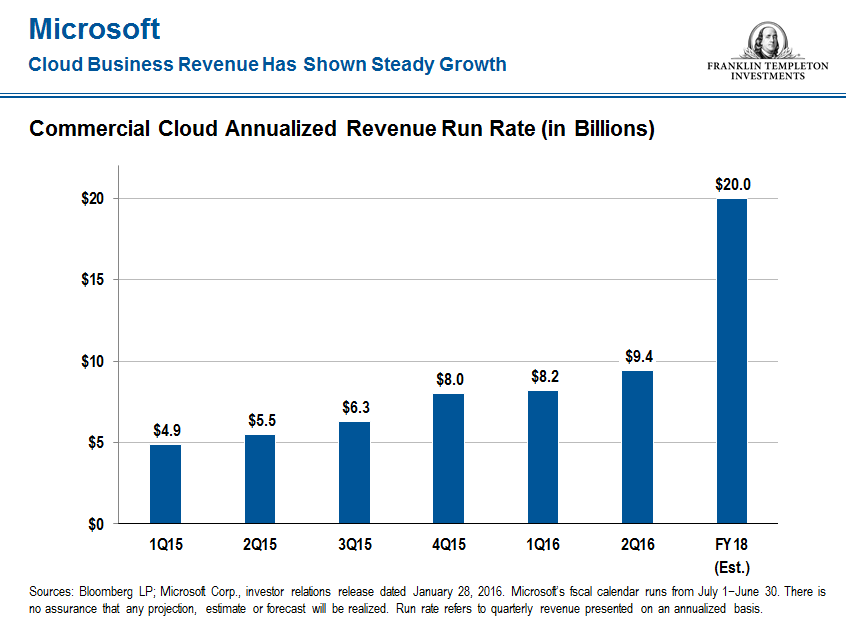

Microsoft,4 for example, started its dividend program in 2003—one of the first tech titans to do so—and has increased its payouts every year since then. The company has a core legacy software business that has high margins and generates a lot of cash, which is funding its transition from a packaged-software to a cloud-based software and services company. We believe this transition will allow Microsoft to continue to be a leader in the enterprise and consumer software space, and allow for consistent revenue, earnings and dividend growth. Although the company has endured a few quarters of disappointing earnings, we expect the cloud businesses to grow and mature and become a bigger part of the whole company. At that point, we believe it’s likely that earnings growth will reaccelerate.

Microsoft aside, tech companies are generally underrepresented in the dividend achiever category compared with, for example, in the S&P 500. But we expect to see an increasing number of tech names come into the achiever universe as the industry matures. It’s a similar story for health care, where we find the more established medical devices and equipment companies as achievers versus biotech or pharmaceutical companies, many of which have not initiated dividend programs.

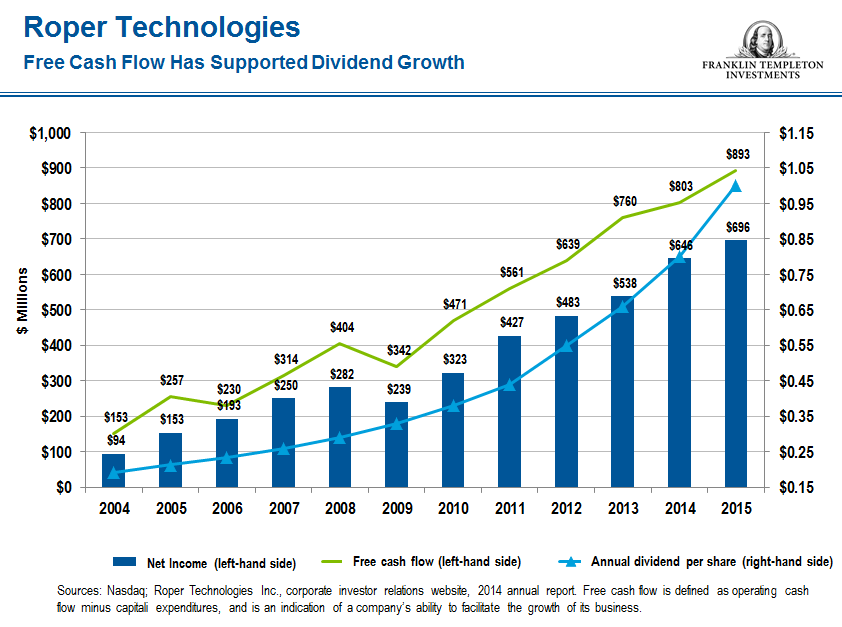

Diversified industrial companies, however, are generally well-represented as achievers, primarily because many are decades-old businesses with strong balance sheets. A company that we believe fits that description is Roper Technologies,5 a diversified industrial company that produces engineered products for global niche markets. Roper has generated a lot of cash over the years, and it has used that cash to gradually grow its dividend. It also uses its excess funds to acquire smaller companies that have a history of generating a lot of cash in their own right.

For merger partners, the company tends to favor software or medical-related firms, avoiding heavy manufacturing concerns that require large capital commitments. Roper’s track record of investing in organic growth and targeted acquisitions, combined with a culture of strict cost controls and an asset-light business model, is driving strong free cash flow growth, as shown in the chart below.

We believe the industrial sector will likely benefit from the modest growth we expect for the global economy. We are positioning our portfolio with that in mind, and are seeking opportunities in the industrial and other cyclical sectors, which tend to have revenues that typically rise in good economic times and fall during down cycles. Those opportunities, however, must meet our stringent investment requirements, which we adhere to no matter which way the economic winds are blowing.

Don Taylor’s comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

Franklin Rising Dividends Fund

All investments involve risks, including possible loss of principal. Value securities may not increase in price as anticipated or may decline further in value. For stocks paying dividends, dividends are not guaranteed, and can increase, decrease or be totally eliminated without notice. While smaller and midsize companies may offer substantial opportunities for capital growth, they also involve heightened risks and should be considered speculative. Historically, smaller- and midsize-company securities have been more volatile in price than larger company securities, especially over the short term. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. The fund may invest up to 25% of its total assets in foreign securities, which may involve special risks, including currency fluctuations and economic and political uncertainty. These and other risks are detailed in the fund’s prospectus.

Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. Download a prospectus, which contains this and other information. Please carefully read a prospectus before you invest or send money.

______________________________________________

1 Source: Morningstar, as of May 16, 2016. Please see www.franklintempletondatasources.com for additional data provider information. Dividend achievers are represented by the Nasdaq Broad Dividend Achiever Index. Indexes are unmanaged, and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. Past performance does not guarantee future results.

2 Source: S&P Dow Jones Indices, as of May 16, 2016. Please see www.franklintempletondatasources.com for additional data provider information. Momentum stocks are represented by the S&P 500 Momentum Index. Indexes are unmanaged, and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges. Past performance does not guarantee future results.

3 Source: Ibid, as of May 16, 2016. The overall market is represented by the S&P 500.

4 As of March 31, 2016, Microsoft Corp. common stock represented 3.15% of Franklin Rising Dividends Fund. Holdings are subject to change without notice.

5 As of March 31, 2016, Roper Technologies Inc. common stock represented 4.05% of Franklin Rising Dividends Fund. Holdings are subject to change without notice.

© Franklin Templeton Investments

© Franklin Templeton Investments