KEY TAKEAWAYS

- Municipal bonds have dodged a seasonally weak June period, with notable gains so far in June 2016.

- A strong first half of June has pushed yields on 10- and 30-year municipal bonds to all-time lows, which should temper investor expectations for seasonal strength over July and August.

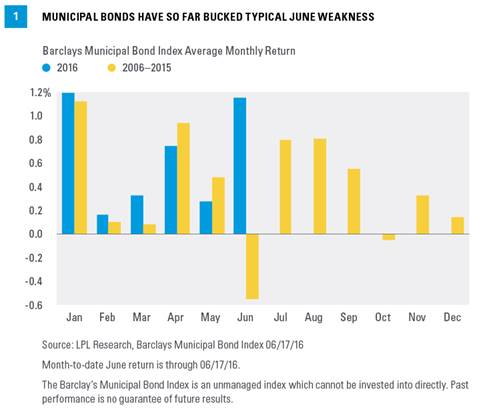

Municipal bonds have thus far bucked the trend of typical headwinds in June [Figure 1]. The Barclays Municipal Bond Index has returned 1.1% month to date through June 17, 2016, a stark contrast to the -0.55% total return the Barclays Municipal Bond Index has averaged in June over the past 10 years. The index has posted positive returns only three times over that time span—a remarkably poor batting average for any interest bearing sector—illustrating the consistency of June challenges until this year. If current performance holds, the Barclays Municipal Bond Index is on track to post its best June performance since 2000, when recession fears sparked notable price gains. However, June’s returns may take away from seasonal strength that typically buffers the municipal bond market in July and August.

A major driver of June weakness in past years has been an increase in supply, with June averaging $38 billion in new issuance over the past 15 years—the heaviest month of the year. Supply did increase on cue in late May 2016, but proved to be little more than a speed bump in the face of global bond strength. Robust demand has easily absorbed new issuance thus far with a strong helping hand from the Treasury sector.

BROAD-BASED BOND GAINS

Treasury sector strength led to broad-based high-quality bond price gains, as international bond strength has spilled over into the U.S. bond market. After closing at 1.84% on May 31, the 10-year Treasury yield declined to 1.58% before moving higher in recent days as investors have taken profits amid a very strong start to June. Municipal bond prices failed to keep pace with Treasuries over the first two weeks of June but still managed strong gains. Even after a modest move higher on June 20, both 10- and 30-year municipal bond yields are very near all-time lows[Figure 2].

Municipal bond strength is also a homegrown phenomenon, not just attributable to global bond strength, reflected by an impressive streak of consistent domestic demand. Municipal bond mutual funds are currently experiencing the fourth longest streak of positive weekly inflows since the Investment Company Institute (ICI) began keeping data in 2007, and the average weekly inflow is the second strongest of any streak since the same date [Figure 3]. Municipal bond funds tallied their 36th week of consecutive inflows for the five trading days ending June 8, 2016 (the last reported) with more than $1.4 billion in inflows.

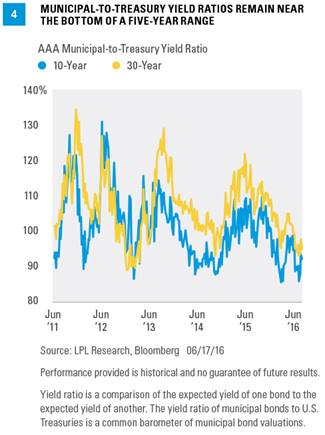

Although municipals failed to keep pace with Treasuries over the first two weeks of June, they did not trail by much. In some cases, municipals managed modest outperformance, a rare feat in an up market for Treasuries. Valuations, on balance, cheapened over the first half of June 2016 but remain on the more expensive end of a five-year range. On June 20, 2016, average 10- and 30-year AAA municipal-to-Treasury yield ratios closed at 92% and 96%, respectively [Figure 4]. Both measures have rarely been below 100% over the past few years.

TEMPERING EXPECTATIONS FOR JULY AND AUGUST

Investors should keep expectations in check for what have historically been good months of July and August [Figure 1]. A sharp decline in new issuance coupled with heavy reinvestment needs from maturing bonds in June and July have driven this phenomenon over the years. But record low yields and higher valuations, which have combined to produce a strong first half of 2016, may limit the impact in 2016. High-quality bond strength has begun to reverse over the past couple of days (June 20 and 21), as investors take profits over the recent run-up in bond prices.

Municipal bonds have not been immune, and should the selling pressure continue, the summer months may prove challenging. On a positive note, the favorable supply-demand balance that has supported municipal bonds in recent years remains intact. Earlier this month, the Federal Reserve (Fed) reported that the municipal bond market grew by only $52 billion during the first quarter of 2016 and remains below its 2010 peak. Such meager growth may not be enough to quell steady demand for tax-exempt income, especially against the prospects of rising tax rates in coming years. Despite recent strength and near-term challenges, municipal bond prices do not fully reflect their tax benefit, and constrained supply should limit weakness should the nascent rise in rates persist. Still, although we are more optimistic on the prospects of municipal bonds, we believe the sector is unlikely to break free of the low-return environment plaguing bond investors.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Municipal bonds are subject to availability, price, and to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rate rise. Interest income may be subject to the alternative minimum tax. Federally tax-free but other state and local taxes may apply.

As with all mutual funds, municipal bond funds carry a degree of risk. You can lose money investing in a municipal bond mutual fund.

INDEX DESCRIPTIONS

The Barclays U.S. Municipal Index covers the USD-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and pre-refunded bonds.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 5541 0616 | Tracking #1-508862 (Exp. 06/17)