High-yield municipal bonds have benefited from broad bond market strength in 2016, but are now more subject to the path of interest rates over the remainder of the year. As we mentioned in our Midyear Outlook 2016: A Vote of Confidence publication, we expect more muted returns across the bond market, and high-yield municipal bonds may see a slowdown after a robust 8.9% total return through July 22, 2016. Additionally, a small number of high-yield municipal sub-sectors, including tobacco bonds, have benefited from outsized gains over the first half of 2016, which we believe are unlikely to be repeated. We are neutral on high-yield municipal bonds as above-average yields are offset by a smaller yield advantage to comparable maturity AAA bond yields and greater than market interest rate sensitivity. On a positive note, default risk, perhaps the greatest threat to high-yield municipal bond prices, remains subdued and unlikely to pose a notable risk absent an economic recession.

DRIVEN BY INTEREST RATES

Many investors may be unaware that interest rate sensitivity can be a key driver of municipal high-yield bond prices, and that has indeed been the case in 2016. The average maturity of high-yield municipal bonds is roughly 20-years, which makes prices very sensitive to interest rate changes and helps explain the rise in prices given widespread yield declines over the first half of 2016. By comparison, the average maturity of taxable high-yield corporate bonds is roughly six years.1 The greater the interest rate sensitivity, the greater the price gains associated with falling interest rates.

Investor demand for higher-yielding bonds has led to stretched valuations. Average yield spreads between top-quality AAA-rated general obligation (GO) bonds and BBB-rated GO bonds fell to their narrowest level of the post-recession period and below early 2015 levels[Figure 1]. Due to the volatility of Puerto Rican bonds in the municipal high-yield universe over the past years, we find the AAA to BBB yield spread a good proxy for the declining risk premium investors are willing to accept to hold lower-rated bonds.

Excluding Puerto Rico, the average yield of the broad high-yield municipal bond market is now lower than pre-2008 levels [Figure 2]. The bulk of Puerto Rican municipal bonds have now dropped out of the Barclays Municipal High-Yield Index upon failure to make payment on approximately $20 billion worth of bonds on July 1, 2016. The sharp drop in yield in July 2016 reflects the exit of Puerto Rican bonds and reveals how low yields are absent the riskiest segment. The average current yield is 5.0%, below yields witnessed in early 2007 and mid-2013 just prior to the taper tantrum bond sell-off.

On a positive note, credit quality underlying the vast majority of lower-rated municipal bond issuers remains firm. Although the dollar amount of defaulted municipal bonds has spiked due to Puerto Rico, the number of municipal defaults is on pace to fall below 2015’s already low number, according to Municipal Securities Rulemaking Board (MSRB) data.

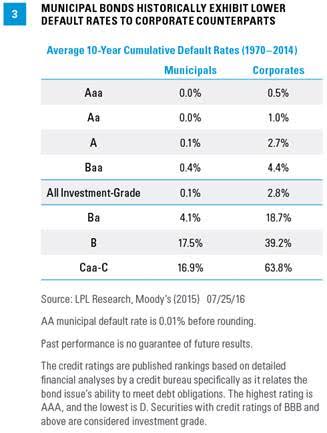

Historically, municipal bonds have had a much lower default rates compared with taxable corporate bonds [Figure 3]. In addition to the average maturity disparities, this is another reason why high-yield municipal bonds exhibit greater interest rate sensitivity. Their inherently higher quality makes them more sensitive to interest rate shifts compared with taxable high-yield corporate bonds, which are much more sensitive to changes in the pace of economic growth and credit quality risks. Most large municipal defaults in recent years, including Puerto Rico, Detroit, and Jefferson County, Alabama, have been years in the making and received a disproportionate share of news headlines; but generally, they had little lasting market impact as municipal problem issuers remains isolated.

Still, much of this good news is largely factored into current yield spreads, a measure of valuations. An increase in defaults or downturn in the economy could lead to wider yield spreads and weigh on high-yield municipal bond prices. Although we do not see either posing an immediate risk, higher valuations mean room for error has decreased and investors need to be cautious.

As mentioned in our Midyear Outlook 2016, we expect the 10-year Treasury yield to end the year flat to slightly higher than the current 1.57%, perhaps ending the tailwind of falling interest rates even if not immediately reversing. However, we also don’t expect deterioration in the economy that would lead to sharply higher defaults. Therefore, credit exposure could remain generally supportive of the sector. Last, investor demand for municipals has also been strong and may continue to benefit the broader municipal market, with municipal bond funds recently marking their 42nd consecutive week of inflows, according to Investment Company Institute data.

CONCLUSION

High-yield municipal bonds have had a solid run year to date, aided by strong investor demand for yield, favorable credit quality trends, and greater interest rate sensitivity as bond yields declined. Valuations have richened and yields are near historic lows in response, suggesting caution. Still in a relative world of near record low yields, valuations may remain expensive absent a sharp reversal in credit quality trends or notable increase in interest rates. Both these risks appear muted. We remain neutral on the sector overall, expecting lower returns over the second half of the year.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Municipal bonds are subject to availability, price, and to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rate rise. Interest income may be subject to the alternative minimum tax. Federally tax-free but other state and local taxes may apply.

General obligation(GO) bonds are municipal bonds backed by the credit and "taxing power" of the issuing jurisdiction rather than the revenue from a given project.High-yield/junk bonds (grade BB or below) are not investment grade securities, and are subject to higher interest rate, credit, and liquidity risks than those graded BBB and above. They generally should be part of a diversified portfolio for sophisticated investors.Government bonds and Treasury bills are guaranteed by the US government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value.

INDEX DESCRIPTIONS

The Barclays U.S. Corporate High Yield Index measures the market of USD-denominated, noninvestment-grade, fixed-rate, taxable corporate bonds. Securities are classified as high yield if the rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below, excluding emerging markets debt.

The Barclays Municipal High Yield Bond Index is comprised of bonds with maturities greater than one year, having a par value of at least $3 million issued as part of a transaction size greater than $20 million, and rated no higher than ‘BB+’ or equivalent by any of the three principal rating agencies. (The long and the short are subindexes of the Municipal Bond Index, based on duration length.)

The Barclays U.S. Municipal Index covers the USD-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and pre-refunded bonds.

This research material has been prepared by LPL Financial.

To the extent you are receiving investment advice from a separately registered independent investment advisor, please note that LPL Financial is not an affiliate of and makes no representation with respect to such entity.

Not FDIC or NCUA/NCUSIF Insured | No Bank or Credit Union Guarantee | May Lose Value | Not Guaranteed by Any Government Agency | Not a Bank/Credit Union Deposit

RES 5581 0716 | Tracking #1-519712 (Exp. 07/17)

1 Barclays High-Yield Bond Index and Barclays High-Yield Municipal Index