Q: Should investors and issuers be prepared for even higher Libor levels in the weeks and months to come, or have we already seen the most significant moves?

Schneider: Anticipation of U.S. money market reform has pressured short-term funding rates higher as U.S. investors move toward money market funds that invest only in government securities and away from prime (credit) money market funds. As a result of this diminished appetite (as reflected in past and expected redemptions in prime money market funds), issuers of commercial paper and certificates of deposit, mainly non-U.S.-domiciled banks, have to pay more for funding as yields move higher and funding risk premiums widen. As a result, many funding benchmark rates, including U.S.-dollar-denominated Libor resets, have seen dramatic increases of more than 50 basis points (bps) over the past year – and less than half of that increase can be attributed to the 25 bp hiking action by the Federal Reserve last December.

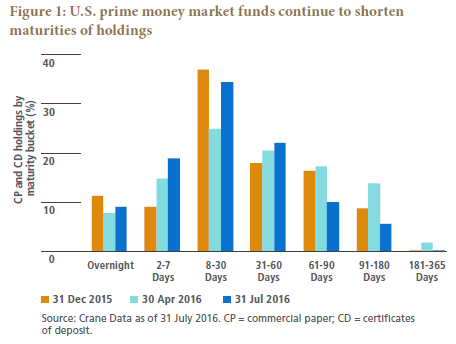

While prime money market funds have raised a lot of liquidity in preparation for the reforms, the “known unknown” factors remain steadfast: How much additional outflow can we expect, and over what timeframe – will 14 October be the turning point, or will outflows continue into 2017? To hedge these known unknowns, we think many prime fund managers will continue to buy shorter and shorter maturities (see Figure 1) and invest more and more in government-related paper to fund potential outflows. This should keep upward pressure on Libor during the weeks ahead. Our base case is for the Libor-OIS spread (i.e., the difference between Libor and the overnight index swap rate, which is often benchmarked to the fed funds rate) to peak in early October at about 5 bps – 10 bps higher than the current level of roughly 40 bps (as of 25 August). More importantly, we believe that the Libor-OIS spread (and hence relative Libor rates) will remain cyclically elevated beyond October as banks and investors adjust to a significantly diminished investment base and new rules governing prime funds.

Q: What are the downsides of higher Libor rates?

Schneider: Banks and other debt issuers who utilize Libor-based floating notes or commercial paper will feel the pain of higher Libor, paying more for funding as yields move higher and funding spreads widen. Such institutions need to realize that what they are experiencing is a structural change, not simply an episodic period of upward repricing. As such, these institutions should reevaluate their capital structures in light of these altered conditions and potentially seek longer-maturity or more diversified funding sources over time.

We also note that the vast majority of these higher rates is paid by institutional issuers of credit (and especially non-U.S.-domiciled banks) who have floating rate debt outstanding. For individuals, the pain of such increases is for the most part limited to those who have mortgages tied to Libor resets, which is less than 20% of the U.S. residential mortgage market (according to the Wall Street Journal).

Q: Could the Libor rate be driven down, or at least stabilized, by increasing demand from investors outside the money market sphere?

Schneider: It’s important to remember that this is not simply a market reaction to a piece of data, but a structural reform that will change the way most investors allocate their cash liquidity over time. So while this year’s spike in Libor reflects the initial market reaction to money market reform, it will take months if not several quarters for rates to recalibrate to lower levels again relative to perceived “risk-free” rates such as OIS or the fed funds rate. And don’t expect once the October implementation date has passed for levels simply to recalibrate back to thresholds we observed earlier in 2016. And yes, as with any free market, repricing of assets will invite new participants to consider investing in short-term paper, which eventually should limit the rise of dollar-denominated Libor spreads for issuing financial institutions.

Q: For investors focused on liquidity and short-term assets, does the increase in Libor signal a potential opportunity?

Schneider: It absolutely presents a unique opportunity for those investors willing to assess and adapt to this structural evolution. Money market reform really isn’t “new news” to most investors at this point, although its effects might appear to be newsworthy of late. As an active portfolio manager, PIMCO has been anticipating money market reform for more than two years, opportunistically positioning our short-term capital preservation strategies to seek additional returns ahead of the effective date in October.

For example, we are overweighting floating rate assets that are indexed to Libor because we expect banks will continue paying relatively higher funding costs for the foreseeable future as a result of these structural changes.

Another avenue of opportunity we would seek to capture is the emerging demand for U.S. dollars by foreign investors. Strategies that seek to lend U.S. dollars on a fully hedged basis to foreign investors have a unique and attractive tailwind that allows them to invest dollars at attractive yields compared with investing only in U.S.-dollar-denominated assets such as U.S. Treasury bills or notes.

Q: How should investors be thinking about the bigger picture of short-term portfolio positioning in light of money market reform and the rise of Libor?

Schneider: At PIMCO, we have been anticipating this structural change in Libor for years. For some time we have viewed floating rate assets as an attractive trade, and we will continue to evaluate other opportunities that emerge from money market reform.

We believe the most important thing for investors to realize is that this is an evolutionary process. The new era calls for comprehensive resources that are able to assess the changing landscape of liquidity management and to understand and successfully navigate the new regulatory frameworks, which require new paradigms for capital preservation strategies beyond solely utilizing traditional money market funds.

Investors also should acknowledge how these structural changes are likely to affect their investment outcomes and risk profiles. Active and innovative management of liquidity in this new era will likely be critical to preserving not only liquidity, but also purchasing power for their capital over time. Traditional approaches to liquidity management that don’t embrace these structural modifications may fail to do both.