Improving US economic data and stabilization in the global economy have upped the odds that the Federal Reserve (Fed) will raise interest rates in the coming months following a long pause. Roger Bayston, senior vice president, Franklin Templeton Fixed Income Group, discusses why he thinks the Fed may now feel more comfortable increasing rates for the first time since December 2015 and explains why he thinks another rate hike this year may not mean the “lower-for-longer” trend in interest rates is over. He also provides a short overview of the US economy and reveals how he’s positioning his portfolios in the sixth year of an economic recovery.

Federal Reserve (Fed) Chair Janet Yellen recently hinted that a rise in the central bank’s benchmark interest rate could be on the way. With major US market averages hovering near all-time highs and the US economy showing modest growth, I believe the Fed has the ammunition it needs to pull the trigger and raise its short-term interest rate, likely this year.

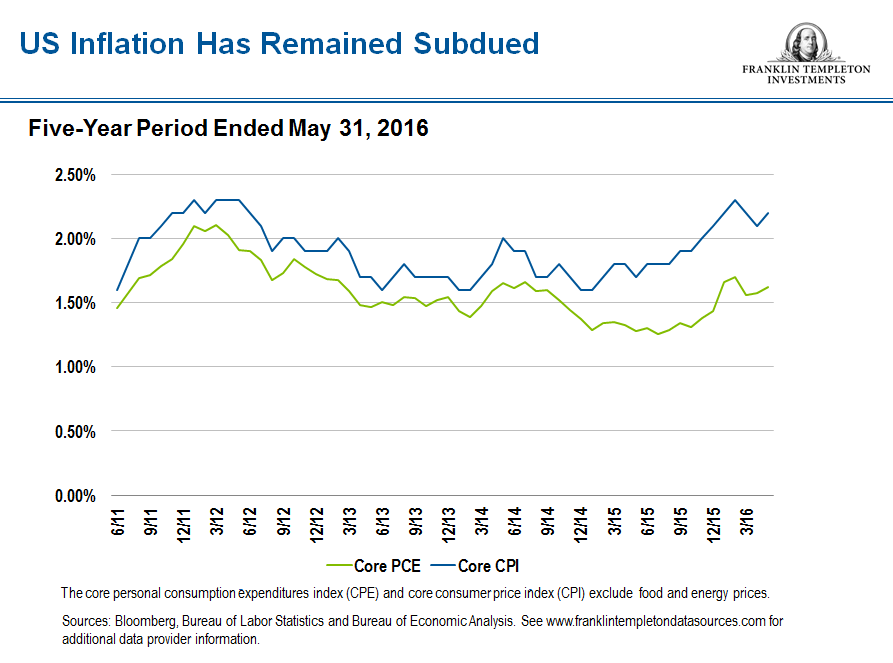

However, I don’t think the Fed will go on a rate-raising spree in the coming months, and the “lower-for-longer” scenario will likely continue for US interest rates. Along with employment statistics, the Fed considers inflation a key factor when it decides whether to raise rates, and we don’t see any meaningful inflationary pressures building in the economy. The employment picture has improved, but it does not appear to have been accompanied by a corresponding rise in consumer prices overall. And, although some major US cities have raised their minimum wage, we think companies will find innovative ways around mandated wage increases. For example, some fast-food restaurants have already announced plans to replace some frontline counter workers with tablet computers.

We also think technology and demographic factors also will likely keep inflation under control. Across the entire tech spectrum, as technology is upgraded, consumers generally receive more services for the same price. And as the bulk of the baby-boomer generation formally retires, they will spend less money, which should also help keep a lid on inflation. While the Fed’s official inflation target is 2%—meaning a rise above this level would signal inflationary pressures—maybe it isn’t the most important factor in the rate-hike equation.

Focus on Fundamentals

Despite the likely buzz surrounding the Fed’s potential decision on rates either this month or in the last two policy meetings of the year, I doubt a modest increase of 25-basis-points would significantly affect overall US economic activity, although it could create some short-term market volatility. Focusing on the bigger-picture fundamentals, the US economy and market appear healthy enough to absorb the shock of a small tightening move.

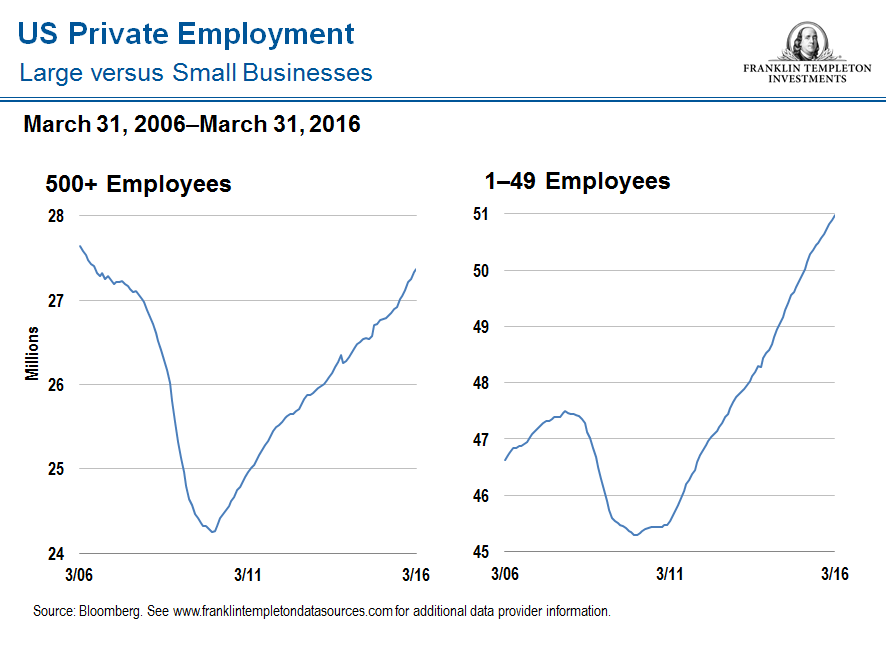

Recent indicators point to a moderately healthy US economy. As mentioned, the labor market, especially for small businesses, appears healthy. Consumer spending rose 0.4% in July1 and housing prices climbed 1.2% in the second quarter,2 and we expect those numbers should continue to rise.

While there have been complaints in some circles about the relatively slower level of economic growth in the United States than in previous recoveries, we believe this slower pace of growth has prevented the development of some of the excesses in the economy that led to the 2008-2009 financial crisis, such as the housing bubble. With a lack of excesses, we think it’s possible the expansion may continue longer than usual.

A Look at the Credit Markets

In light of stable US growth, we still like the corporate credit market. However, we have adjusted our investment strategy as we move further along in the economic expansion. For instance, we have been rotating out of the cyclical sector because those companies are typically more sensitive to what’s happening in the business cycle.

In the investment-grade credit area, we favor financials and health care. Although US banks have struggled with lower net interest margins in the years-long, low-interest-rate environment, their capital ratios have greatly improved over the last seven years. After the financial crisis of 2008-2009, regulators wanted banks’ balance sheets to have less leverage and look more like utilities’ and less like hedge funds’. This focus on stockpiling capital may not benefit banks’ equity owners in the long term, but, in my view, bondholders have more security than they have had in many years. Meanwhile, health care companies have benefited from an increasingly aging population, and, in our view, the sector has produced many promising advancements.

On the high-yield credit side, we favor stable, non-cyclical companies that are generating a lot of cash, particularly telecommunications and, again, health-care outfits. With high-yield bond prices rising about 20% since mid-February,3 we’ve recently taken some risk capital off the table and have redeployed the proceeds elsewhere, including into agency mortgage-backed securities, which we believe offer attractive returns with lower levels of risk.

While managing risk is important, we like to remind investors that there are potential long-term rewards for taking those risks. I think it’s human nature to be risk-averse, especially when investors can be bombarded with sometimes-misleading headlines about interest rates or other economic news. As portfolio managers, however, it’s our job to push through those fears with the goal of helping our investors achieve long-term success. So, in sum, regardless of whether the Fed raises interest rates this month or in the coming months, we think the market can absorb potential tightening in stride, and we remain focused on spotting potential opportunities, no matter where we are at in the economic cycle.

Comments, opinions and analyses expressed by the investment manager are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

What Are the Risks?

All investments involve risks, including possible loss of principal. Interest rate movements and mortgage prepayments will affect a fund’s share price and yield. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in a fund adjust to a rise in interest rates, a fund’s share price may decline. Changes in the financial strength of a bond issuer or in a bond’s credit rating may affect its value. The risks associated with higher-yielding, lower-rated securities (commonly called junk bonds) include higher risk of default and loss of principal. Diversification does not guarantee profit nor protect against risk of loss.

Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. Download a prospectus, which contains this and other information. Please carefully read a prospectus before you invest or send money.

___________________________________________________

1 Source: Bureau of Economic Analysis, release dated August 29, 2016.

2 Source: Federal Housing Finance Agency, release dated August 24, 2016.

3 Source: BofA Merrill Lynch, as of September 13, 2016. High-yield bonds are represented by the BofA Merrill Lynch US High Yield Total Return Index, which tracks the performance of US dollar-denominated, below investment grade-rated corporate debt publically issued in the US domestic market. Indexes are unmanaged, and one cannot invest directly in an index. They do not include any fees, expenses or sales charges. Past performance is not an indicator or a guarantee of future performance. See www.franklintempletondatasources.com for additional data provider information.

© Franklin Templeton Investments