- Rulers and Rules

- Nothing New Under the Rising Sun

- Is America Getting Too Concentrated?

Our feelings about rules change with age. As children, we hate being told when to go to bed and when we can eat ice cream. As parents, we come to see sensible limits as necessary to the maintenance of order and the promotion of the common good. Of course, this latter perspective may be due to adults’ ability to lay down the law.

Rules play an important role in an economy. Most regulations are designed, at least in theory, to facilitate the achievement of good overall outcomes. But some directives beget unintended consequences and others take on a life that goes far beyond their initial purpose.

Does regulation go too far, or not far enough? Does compliance hinder growth and entrepreneurship, or does it create a useful system of checks and balances? The new administration’s posture on these questions may be one of the more consequential outcomes of the November balloting here in the United States.

There is a broad range of activities covered by regulation. Food and drug safety, environmental protection, labor utilization and civil rights are among the subjects of laws or restrictions set at the federal, state, or local levels. The desired outcomes can be promoted by carrots (incentives) or sticks (potential penalties).

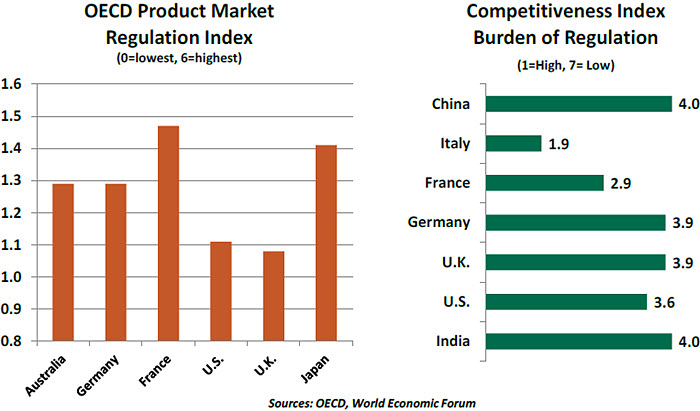

By several objective measures, such as the two shown below, the level of regulation in the United States is not exceptional relative to other nations. That isn’t to say that regulation isn’t burdensome, but that it does not appear to put the country at a competitive advantage.

With all due respect to the libertarians among us, some regulations do make some sense. We shouldn’t have people flying commercial airplanes who have not been properly trained. Pharmaceuticals should not be offered to the public without clinical trials. Financial institutions should be required to hold adequate levels of capital so that their failures don’t become public liabilities. Given these examples, most people would agree that the optimal amount of regulation is nonzero.

When is regulation justified? Proponents often cite situations where one party’s actions introduce costs on another (economists call these “externalities”). In a recent example, limitations on oilfield wastewater disposal were tightened in the wake of a series of Oklahoma earthquakes caused by the injection of the water back into the substrata.  To be sure, there are market-based solutions to problems like these. In theory, Oklahoma residents could collectively bargain with the oil companies on the optimal level of seismic activity before granting drilling rights. But the two sides of such a transaction may not be equally organized, sophisticated or informed. Monitoring may be difficult, and consequences may take many years to arise. Where frictions like these prevent markets from clearing effectively and equitably, regulation may be appropriate.

To be sure, there are market-based solutions to problems like these. In theory, Oklahoma residents could collectively bargain with the oil companies on the optimal level of seismic activity before granting drilling rights. But the two sides of such a transaction may not be equally organized, sophisticated or informed. Monitoring may be difficult, and consequences may take many years to arise. Where frictions like these prevent markets from clearing effectively and equitably, regulation may be appropriate.

But compliance comes at a cost. For example, the Sarbanes-Oxley Act (SOXA) of 2002 placed substantial new requirements on corporate accounting. Compliance with SOXA now costs companies an estimated $20 billion annually, yet bookkeeping sleight of hand continues.

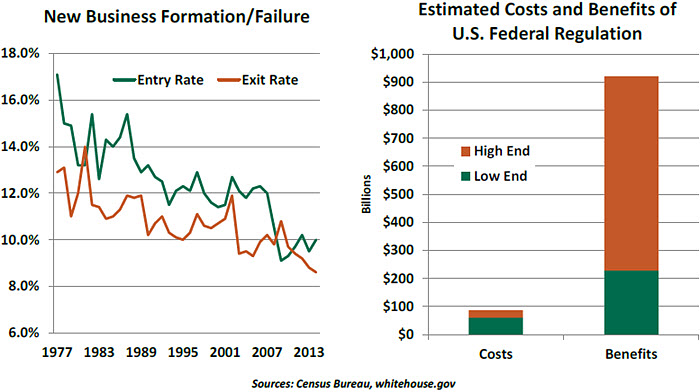

Regulation can also introduce more general costs to an economy. The advance of post-crisis rulemaking has been blamed for a slow pace of entrepreneurship and innovation. Rising minimum wages, requirements under the Affordable Care Act (ACA) and tighter restrictions on bank lending (among others) have all been cited for a slowing pace of business formation. New firms are especially adept at creating jobs and advancing novel ideas, so a paucity of startups means less economic dynamism.

The debate over the costs and benefits of regulation is fierce and parochial. As you might expect, the U.S. administration reports that the  benefits of regulation are far in excess of the cost. As you might also expect, conservative think tanks have estimated that the regulatory burden costs America almost $2 trillion annually. It is terribly hard to reconcile these perspectives.

benefits of regulation are far in excess of the cost. As you might also expect, conservative think tanks have estimated that the regulatory burden costs America almost $2 trillion annually. It is terribly hard to reconcile these perspectives.

During this year’s campaign, debate has focused most heavily on the following regulatory areas:

- Bank supervision - The 2008 crisis bred an understandable wave of new rules and new monitoring for financial companies. Yet, although the resulting Dodd-Frank Act was well-intentioned, some contend that it has limited the amount of intermediation in the U.S. economy. (Home mortgages are a case in point.) While some have called for a repeal of the act, others are hoping for openings to relax some of its more restrictive elements.

- Health insurance - We’ll offer a long discussion of health policy in an upcoming issue. The regulatory aspect refers to the requirements of individuals and firms under the ACA, which some see as a step forward in insurance coverage and others see as a pox on insurers and providers.

- Environmental protection - Preserving habitats and ensuring clean water have long been subjects of longstanding debate, but climate change and its impact on the environment is the current signature issue on this front. Debate centers on the seriousness of the issue and what should be done about it.

- Antitrust. We’ve witnessed a renewed wave of large corporate combinations of the past several years. Do these promise additional efficiencies, or do they represent undue restraint of trade?

The new president will choose an attorney general and set the tone of enforcement across federal agencies. While regulation may not get the attention that fiscal and trade policy might, it is nonetheless influential in setting the business landscape.

As we become elderly, our feelings about regulation turn dark again. At that juncture, our children begin setting rules for us. I’ll say this right now: if my kids tell me I can’t eat ice cream, they’re out of my will.

Merger Mania?

Anthem and Cigna, Aetna and Humana, Dow and Dupont, Monsanto and Bayer. These proposed pairings are the most prominent examples of a mergers and acquisition (M&A) frenzy of recent months. To proponents, corporate combinations will increase efficiencies and foster the creation of new products and services. There are, however, detractors who take a much dimmer view of the urge to merge.

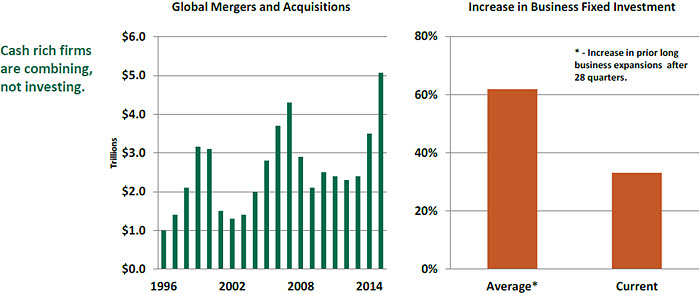

The value of global M&A transactions surpassed $5 trillion in 2015, exceeding the record reached in 2007. U.S. M&A activity made up nearly 50% of these deals during 2015 and a number of factors accounted for this surge. The main one is that economic growth following the Great Recession has been sub-par by historical standards. In this environment, firms faced challenges generating organic revenue growth.

Of course, companies could seek that growth by investing internally. Business fixed investment has proceeded at a much lower pace during this expansion; given the uncertain outlook, companies have been very cautious about this strategy.

Instead, firms have used substantial accumulations of cash to find acquisitions or combinations that boost market share and address margin pressures. Low interest rates allow acquiring firms to secure attractive financing terms.

Concerns about M&A fall into two categories. Firstly, large combinations often do not deliver the innovation, growth or shareholder value projected at the time of the transaction. Secondly, worries about increases in industry concentration are rising. When firms engage in practices that reduce competition, their profits may increase but consumer welfare may be sacrificed. The negative reception of recent health care mergers by the U.S. Justice Department is a reflection of these concerns.

So in this sense, bigger may not necessarily be better for the broad population. The question of how big is too big will be an issue for the next administration.

Lower for Longer in Japan

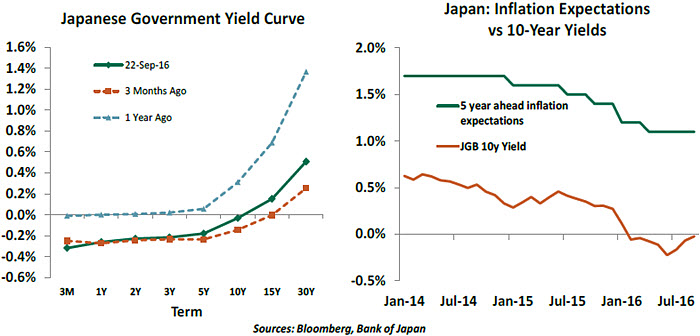

The Bank of Japan (BOJ), while resisting any additional monetary stimulus, made two significant changes in its monetary policy framework this week. The first was to move from targeting the quantity of Japanese government bond (JGB) purchases to targeting the yield of JGBs. Secondly, it committed to continuing with monetary stimulus not only until the 2% inflation target is met, but until inflation “stays above the target in a stable manner.”

Given that the BOJ hasn’t been even able to meet the 2% target satisfactorily, some might find the latter pronouncement brave or even futile. However, it is designed to quash any speculation about the end of accommodative monetary policy and prevent premature tightening of monetary conditions if and when inflationary pressures revive.

The commitment to keep 10-year JGB yield at around 0% (which is also the current yield) is more interesting. There have been worries for a while that BOJ would run out of bonds to buy and swapping the quantity target for a price target should allow the BOJ to taper purchases without provoking a market reaction.

Furthermore, by gaining control over the long end of the yield curve (central banks typically only set the short-term rates), the BOJ can afford to cut short-term rates more deeply into negative territory without impacting the profitability of the banking sector (commercial banks typically borrow short term and lend long term).  Targeting long-term yields is not a novel idea. It was most prominently used by central banks to deal with war-related debts in the middle of the 20th century. The Federal Reserve, for example, capped the long term treasury yield at 2.5% from 1942-1951. The Bank of England followed a similar policy. In the sense that the BOJ’s policy is now overlapping with government’s debt management, one might even term this helicopter money.

Targeting long-term yields is not a novel idea. It was most prominently used by central banks to deal with war-related debts in the middle of the 20th century. The Federal Reserve, for example, capped the long term treasury yield at 2.5% from 1942-1951. The Bank of England followed a similar policy. In the sense that the BOJ’s policy is now overlapping with government’s debt management, one might even term this helicopter money.

Overall, the BOJ is setting itself the rather ambitious task of managing a number of things simultaneously — shorter-term interest rates, long-term interest rates, the shape of the yield curve, the profitability of the banking sector, exchange rates, inflation and economic activity.

Does this new policy framework change anything for the broader economy? As part of the comprehensive assessment of monetary policy that accompanied the policy announcement, the BOJ presented some interesting findings. Its review highlighted the role of monetary policy in lowering both nominal and real interest rates. While it asserted that these developments have improved economic conditions, the evidence was less convincing. The efficacy of negative rates also remains an open question.

Thus, BOJ’s optimism about meeting its target and the revival in economic activity appears to be misplaced. We continue to believe that the key for Japan to break out of its deflationary rut is for policy makers to make progress on the other two arrows of Abenomics: larger fiscal stimulus and supply side measures such as labor market reforms. Without progress on these fronts, all of the BOJ’s efforts could come to naught.

© Northern Trust