The delta is in EM

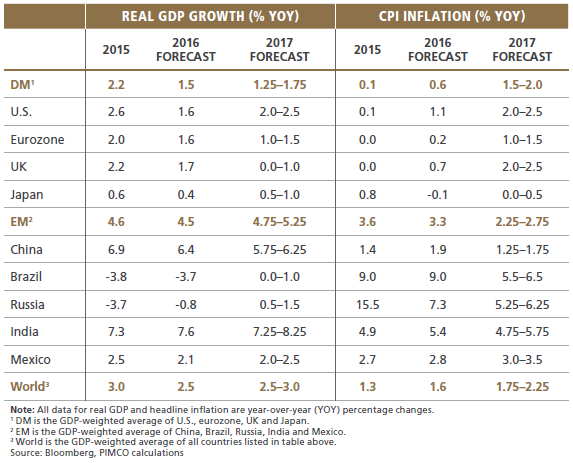

A key feature of our 2017 baseline forecast is better prospects in emerging markets (EM), where we see aggregate GDP growth accelerating from some 4.5% this year to between 4.75%–5.25% next year.

External conditions for many EM economies have improved due to the stabilization of commodity prices and the U.S. dollar. Internal conditions are more conducive to growth, too: Inflation has likely peaked, giving central banks room to ease, and several countries are making progress on structural reforms. Also, with the deep recessions in Brazil and Russia now likely to end and give way to a moderate recovery, a major drag on EM aggregate growth should disappear.

Regarding China, our base case is that the ongoing rebalancing from investment to consumption leads to a further gradual slowdown in growth, which continues to be overstated by the official statistics. However, the hard landing in the industrial complex, which is what matters most for global trade and commodities, has already happened in recent years – evidenced by the past decline in commodity prices and dismal growth rates of industrial output, exports and imports. This, together with our expectation that further currency depreciation will be gradual and orderly, suggests that China won’t throw major spanners in the wheels of the global economy and its EM peers over our cyclical horizon.

Benign baseline, but zero room for complacency

While our baseline scenario of ongoing global growth helped by better EM fundamentals and supportive policy is relatively innocuous, there is no room for complacency, for three reasons:

- First, asset markets seem fully priced for a very benign outcome and thus vulnerable to even small negative surprises.

- Second, as we explained in our Secular Outlook in May, we are concerned about longer-term risks that are lurking beneath the surface, such as high debt levels, diminishing returns to monetary easing and the longer-term consequences of rising populism.

- Third, even if these bigger secular risks remain contained, a lot can derail our and the (similar) consensus baseline forecasts even over the cyclical horizon. Therefore, we actually spent more time at the forum discussing the swing factors that could drive left tail or right tail outcomes, rather than the baseline itself.

Enter the three P’s: Productivity, policy and politics

In our view, the most relevant swing factors for the cyclical outlook are productivity, (monetary and fiscal) policy and politics. The simple framework is as follows:

-

Productivity drives the supply side of the economy and thus potential output growth;

-

Policy is the main determinant of aggregate demand and thus of the fluctuations of actual GDP relative to potential (the “output gap”); while

-

Politics enters the forecast equation as the main non-economic source of uncertainty and volatility.

Stronger productivity: Blessing or curse?

Declining productivity growth in recent years has been the main culprit in the slowdown of potential output growth and for declining estimates of the neutral rate of interest (r*), which figures prominently in central banks’ thinking about the appropriate current and future policy stance.

The consensus now seems to take a continuation of weak productivity growth for granted. Yet, as guest speaker Olivier Blanchard reminded us at our annual Secular Forum in May, productivity growth is inherently difficult to forecast. Therefore, it would be foolish to dismiss the possibility that productivity growth rebounds from its recent dismal pace (−0.4% year-over-year in Q2 2016 and +0.5% annualized over the past five years) over our cyclical horizon.

In fact, a significant rebound in productivity would likely raise the Fed’s estimate of r*, would induce markets to price in a steeper path for rate hikes and could lead to an adjustment of extremely low bond yields. Whether risk assets would fare well in such a scenario is uncertain: While stronger productivity should help corporate profit margins, it cannot be taken for granted that equity markets, which have long become addicted to monetary accommodation and low real interest rates, wouldn’t suffer from withdrawal symptoms.

Policy: Fiscal could make a big difference

We’ve spent much time in previous forums debating the diminishing effectiveness of monetary policy, and the debate continued at this forum. Yet, while we continue to worry about monetary policy exhaustion on our secular horizon, it still appears that the net effects of easing are mostly positive, albeit shrinking, and central banks are now focused on mitigating the negative side effects of low or negative interest rates and flat yield curves on the financial sector with compensating measures. A major U-turn (as opposed to tinkering at the edges) by central banks on negative interest rate policy or QE thus seems very unlikely over our cyclical horizon.

Meanwhile, fiscal policy could become a bigger source of surprises next year, mostly in the form of more stimulus, particularly in DM. Japan has already announced a fiscal stimulus package amounting to around 1.5% of GDP spread out over the current and the next fiscal year. In the UK, following Brexit, the government has also indicated that policy will be eased, but details remain to be seen. In the euro area, our base case includes a moderate fiscal stimulus for next year, but given that several large countries (Germany, France, Netherlands) will hold general elections next year, policy may well turn more expansionary than currently announced. In the U.S., any expansionary fiscal measures announced and agreed with Congress by the next president would probably only be implemented in the 2018 fiscal year that starts on 1 October 2017. However, expectations for more stimulus after the election, irrespective of who wins it, could already lift confidence and thus encourage corporate and consumer spending well before implementation.

To be sure, more fiscal action would be a big deal for financial markets as it could shake up the newfound consensus that we are in secular stagnation, that central banks are the only game in town, and that therefore rates will remain low forever. As with productivity growth, it is not clear whether more fiscal stimulus will turn out to be a boon or a gift of poison for risk assets, given its likely impact on central banks’ reaction function.

Will politics trump economics?

Politics is the main non-economic wild card over our cyclical horizon, and the outcome of the Brexit vote demonstrates that polls and political betting markets can get outcomes spectacularly wrong when the political landscape is shifting. True, global mayhem didn’t materialize after the Brexit vote, but arguably this was because global central banks turned even more dovish and bond yields fell significantly on the back of this, thus propping up risk assets. And just as the Brexit vote had a material impact on actual monetary policy, policy expectations, rates, currencies and risk assets, so too could surprising outcomes in the upcoming elections in the U.S. this year and in France and Germany next year. Moreover, in the run-up to the 19th National Party Congress in China in the fourth quarter of 2017, uncertainty about the country’s future political, economic and military course is also likely to be elevated. Given the series of political risk events over our cyclical horizon, there is plenty of room for temporary bouts of market volatility or even more permanent economic, policy and political regime shifts.

Investment conclusions

While our cyclical outlook is for ongoing growth, policy that remains supportive and broadly range-bound markets, we remain focused on the secular theme of insecure stability (outlined in May) at a time when market valuations, pretty much across the board, range from fair to rich.

Stretching the limits

Diminishing returns to central bank interventions, high debt levels and rising political risks could result in higher term premiums, credit risk premiums and equity risk premiums and suggest more cautious portfolio positioning. In particular we want to be careful about positions that rely to a high degree on central bank support.

Indeed, the Bank of Japan explicitly acknowledged the declining effectiveness of its “quantitative and qualitative monetary easing with a negative interest rate framework” over the summer, with a formal review of the approach and whether it was working. It was no surprise that the central bank answered the question in the affirmative at its September meeting. Yet, its tweaked framework of “quantitative and qualitative monetary easing with yield curve control” amounts to an acknowledgement that both further negative rate cuts and lower long-term rates would be likely to do more harm than good to the financial sector and hence overall financial conditions. It serves to illustrate the limits to extraordinary monetary measures in trying to achieve long-term macroeconomic outcomes.

Positioning

We expect to be fairly neutral overall in terms of duration risk, balancing unattractive valuation with downside risks in the economic outlook. We will likely favor U.S. duration overall versus a number of the global alternatives given that, in a world of low global yields, higher U.S. yields also enhance the flight-to-quality nature of the U.S. markets during periods of market disruption. We continue to favor TIPS (U.S. Treasury Inflation-Protected Securities), based on valuation, the forecast of 2%–2.5% U.S. CPI inflation in 2017 and the risk that different forms of monetary easing could lead to higher-than-expected inflation outcomes over the secular horizon. We also expect to run modest positions in agency mortgage-backed securities (MBS), given reasonable valuations.

While we continue to find opportunities across global spread markets, we have generally reduced overall spread risk in our portfolios and expect to de-risk further with tightening valuations. We continue to favor non-agency MBS and some other securitized assets. We expect to be at benchmark weight or overweight in corporate credit and will favor credit exposures that, while they may weaken during periods of market volatility, tend to have low default risk – and will also demonstrate a preference for short-dated/self-liquidating positons in investment grade and high yield credit. Financials continue to offer some good opportunities as well.

We have reduced currency risk in our portfolios as we do not see any major mispricing or opportunities in G-10 currencies.

On emerging markets, we remain cautiously optimistic. While improving domestic fundamentals and “Calmer C’s” have been reflected in strong performance of emerging markets, we expect to benefit from select opportunities in local and external markets. Higher-yielding EM currencies provide one way to express a positive view on the overall EM beta.

In asset allocation portfolios, we expect to be modestly underweight equities, preferring to take equity-like risk higher up the capital structure. While understanding the volatility and need for differentiation, we expect EM equities to outperform their DM counterparts. At current valuations we think we need to see significant earnings growth in order for equities to outperform.

We will look to grind out alpha across sectors in a low return environment, accessing the global opportunity set. In addition to top-down and bottom-up opportunities, we will continue to emphasize structural alpha opportunities, aiming to benefit from market inefficiencies and diversify alpha sources in our portfolios.

In a generally low volatility environment, we will look to benefit from the periodic volatility spikes that have been characteristic of the past few years, providing liquidity when markets demand it. These spikes may be based on little change in terms of fundamental information, with greater regulation and related reduced transactional liquidity leading to greater local market volatility – all reinforced by concerns about declining policy effectiveness.

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Inflation-linked bonds (ILBs) issued by a government are fixed income securities whose principal value is periodically adjusted according to the rate of inflation; ILBs decline in value when real interest rates rise. Treasury Inflation-Protected Securities (TIPS) are ILBs issued by the U.S. government. Mortgage- and asset-backed securities may be sensitive to changes in interest rates, subject to early repayment risk, and while generally supported by a government, government-agency or private guarantor, there is no assurance that the guarantor will meet its obligations. Corporate debt securities are subject to the risk of the issuer’s inability to meet principal and interest payments on the obligation and may also be subject to price volatility due to factors such as interest rate sensitivity, market perception of the creditworthiness of the issuer and general market liquidity. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Investing in foreign-denominated and/or -domiciled securitiesmay involve heightened risk due to currency fluctuations, and economic and political risks, which may be enhanced in emerging markets. Currency rates may fluctuate significantly over short periods of time and may reduce the returns of a portfolio. Equities may decline in value due to both real and perceived general market, economic and industry conditions. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. Investors should consult their investment professional prior to making an investment decision.

This material contains the opinions of the manager and such opinions are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material has been distributed for informational purposes only. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2016, PIMCO.