With China’s mortality protection shortfall projected to reach nearly $50 trillion by 2020, local regulators are being forced to “mind the gap.” Combined with a very low penetration rate, the industry is benefitting from several important tailwinds that should drive growth in the years ahead.

Slowing wage and job growth in China has made the insurance industry a more attractive source of employment. Over the last two calendar years, agent growth has soared, climbing 12% in 2014 and a whopping 57% in 2015. Historically, agent growth has been a good leading indicator for premium growth thanks to the industry’s focus on the agency channel. That can make for very attractive investment opportunities for insurance companies and their shareholders.

Shanghai

Shanghai

At the end of 2015, nearly half the agents had less than one year of experience, which temporarily suppressed agent productivity growth. Productivity is rebounding this year with agent experience and perhaps a more important shift that removed a drag on industry growth over the last few years. After an initial rebound following the financial crisis, the Chinese banking regulator sought to reign in credit growth by setting formal loan targets. However, funding needs often exceeded these quotas, leading to the creation of alternative financing products known as wealth management and trust products. These products carry an implicit guarantee from the issuing bank and a much higher yield than those generally allowed with insurance products. Investors are effectively capturing a risk free and attractive yield while funding in many cases weaker operating companies with questionable cash flow generation capability. Now that the regulators are cracking down on the growth of these products, life insurance product volumes are coming back as more consumers seek to build their wealth and protect it, too. The combination of a more experienced agent network and improving demand should drive strong premium growth and higher agent productivity for years into the future.

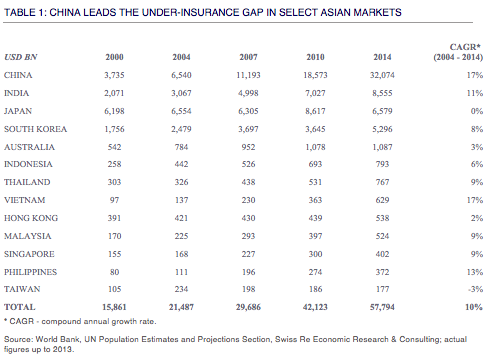

China’s insurance regulator is also pushing to drive consumer demand. Recent changes in pricing regulation as well other incentives around tax and lower capital requirements have enhanced the profitability on medium- to long-term regular premium products. The insurance companies, in turn, are providing greater incentives for agents selling those products. The result is less demand for higher-risk wealth management products and accelerating new premium growth. At $32.1 trillion by the end of 2014,1 China’s mortality protection gap—the amount needed after readily available financial resources to sustain the living standards of dependents after the death of a working family member—remains exceedingly large. Given the country’s still thin social safety net, the government is clearly mindful of the under-insurance gap and taking important steps to close it. Yet there’s a long way to go: life insurance penetration in China amounts to just 2.4%. The runway for future growth in China’s life insurance industry is long indeed.

As incomes and living standards rise, though, the gap won’t be closed anytime soon. In fact, it will continue expanding. Based on current trends, pan-Asian life insurer AIA Group forecasts that the gap across Asia will continue to rise and total $82 trillion by 2020.2 It projects China’s mortality gap alone will hit $46 trillion in four years. “The widening protection gap underlines the growing need for innovative, compelling and meaningful savings and protection offerings (for) consumers all around the region,” AIA said. Insurers and their shareholders appear well positioned for this huge, long-term structural growth opportunity, both in China and the rest of Asia.

1. Asia-Pacific 2015, Mortality Protection Gap,Swiss Re, August 2015

2. Asia’s Protection Gap Underlines Need for Greater Insurance Planning,AIA Group, July 29, 2015

Read more Emerging Views from Thornburg Investment Management

Important Information

Before investing, carefully consider the Fund’s investment goals, risks, charges, and expenses. For a prospectus or summary prospectus containing this and other information, contact your financial advisor or visit our literature center. Read them carefully before investing.

The views expressed by the portfolio managers reflect their professional opinions and are subject to change. Under no circumstances does the information contained within represent a recommendation to buy or sell any security.

Investments carry risks, including possible loss of principal. Additional risks may be associated with investments outside the United States, especially in emerging markets, including currency fluctuations, illiquidity, volatility, and political and economic risks. Investments in small- and mid-capitalization companies may increase the risk of greater price fluctuations. Investments in the Fund are not FDIC insured, nor are they bank deposits or guaranteed by a bank or any other entity.

Please see our glossary for a definition of terms.

Thornburg mutual funds are distributed by Thornburg Securities Corporation.

Thornburg Investment Management, Inc. mutual funds are sold through investment professionals including investment advisors, brokerage firms, bank trust departments, trust companies and certain other financial intermediaries. Thornburg Securities Corporation (TSC) does not act as broker of record for investors.