Blame it on Regulation Q.

Within the Glass-Steagall Act of 1933, Regulation Q used to impose a cap on the interest rates banks could pay on deposits. Over time, investors sought a better liquidity management solution and higher returns for their excess liquidity. Eventually, innovation took hold, and the regulated 2a-7 U.S. money market fund industry began to germinate in the 1970s, offering a balance of higher returns, $1 par share price and same-day liquidity.

Just as the emergence of money market funds more than four decades ago encouraged investors to consider a different approach to liquidity management, the SEC’s new money market fund regulations, which take effect in mid-October, should also mark a point of reflection for investors. We would encourage investors to consider the impact of these alterations, including the deteriorating purchasing power protection of money funds. We would also encourage those still allocated to money market funds (hopefully to a lesser degree), to look “under the hood” at the composition of fund holdings. At a glance, investors can see that all money market funds are not equal. Substantive differences in holdings can result in differences in net returns to investors over time, even though each of these funds is adhering to the same SEC regulatory requirements.

What to consider in money market funds

In an attempt to safeguard money market funds and remove previous structural deficiencies, the SEC regulations have refined what investments these funds can make. Government money market funds, which can still offer investors the stability of a fixed $1/share net asset value, now need to hold 99.5% of assets in government-related securities – namely, Treasury bills, agency discount notes and repurchase agreements, or repos. As with other core fixed income strategies, these funds’ largest risk will now be interest rate risk.

To successfully navigate this risk, asset managers need to have a robust investment process to analyze their expectations for interest rates/monetary policy against what is priced into the market, as well as compelling views on global macroeconomic trends. Without these, an investment manager will likely leave valuable basis points of income on the table.

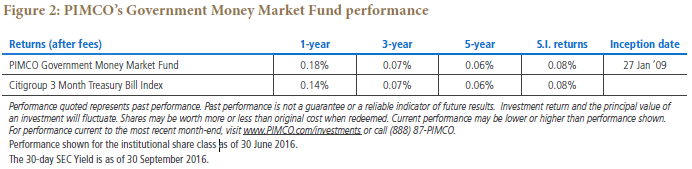

Another consideration for investors should be the size and scope of the investment manager’s capabilities. The skillset, expertise (even beyond money markets) and size of the manager should be focal points rather than the size of the fund itself. Firm size can mean greater access to the repo market in particular, and repos will be a precious commodity: They have historically offered higher yields than short-dated Treasury bills and agency discount notes, and the yield differential between overnight repos and three-month T-bills is currently at its widest in years (see Figure 1).

Moreover, different types of repurchase agreements can potentially yield even more: Delivery-versus-payment (DVP) repos, which PIMCO generally favors, have historically offered superior returns and collateral protection for investors compared to the tri-party custodian alternative, which the majority of larger money market fund complexes employ. Thus, money-fund managers that have greater access to (DVP) repo balance sheet can potentially earn higher yields.