It seems unprecedented to us that the US stock market is in the 7th year of a bull market and investors generally remain too fearful to invest in equities. The data clearly show that not only are individual investors cautious, but so are pensions, endowments, foundations, and hedge funds. Investors are typically quite bullish by this time in the bull market, but that does not appear to be the case today.

Our “Year Ahead” report for 2016 was titled “Mute the TV”. We highlighted last December that 2016 was a Presidential election year, and that investors could potentially be overwhelmed by political propaganda. The key to investing in 2016 would be investors’ ability to sift through all the election-related noise and invest based on fundamentals.

Our guess is that few investors realize that the S&P 500® has appreciated more than 15% in the past year (through September 30), and those that realize stocks have performed so well feel that an impending bear market will be worse because it hasn’t happened yet. It is inconceivable to investors that the US bull market has been and continues to be justified by fundamentals.

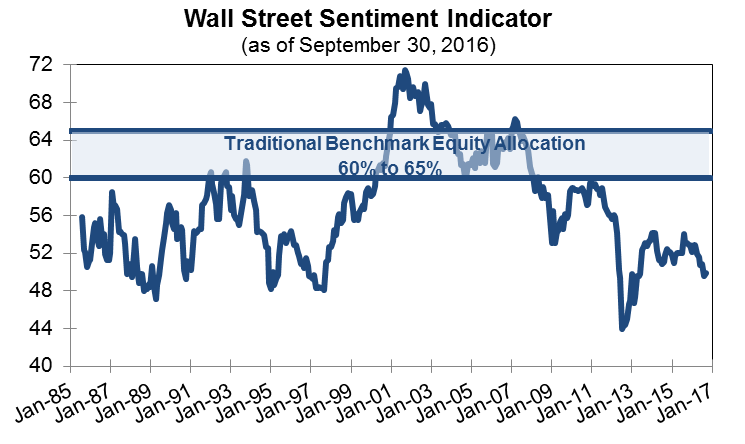

This overwhelming bearish sentiment is supported by data. All the groups mentioned above have been net sellers of equities during this bull cycle according to data from Bank of America/Merrill Lynch1. In addition, Chart 1 points out that Wall Street has been recommending that portfolios have underweighted positions in equities throughout the bull market. This may be more typical than one might at first realize; Wall Street also recommended underweighting equities throughout the entire bull market of the 1980s and 1990s.

Source: Richard Bernstein Advisors LLC. 1 BofAML Equity Client Flow Trends, 8/23/16

Blaming, not crediting, the Fed for the bull market?

It has been popular among bearish observers to blame the bull market on the Fed. They feel the Fed is artificially pumping up asset prices. First, we think such comments constitute a rather obvious sentiment barometer. Investors do not believe the stock market should appreciate, but the bull market continues to defy their bearish forecasts. Rather than altering their asset allocations, investors have so much conviction in their fears that they are actually “blaming” the Fed for a bull market. This is highly unusual because historically investors thanked the Fed, rather than blamed the Fed, for bull markets. The constant negative consensus regarding equity returns suggests the current bull market could still have a considerably longer life than most investors expect.

Don’t forget earnings!

Many investors have dismissed our bullish views because they believe there is nothing fundamental behind the bull market. This is simply not true. Fundamentals have improved dramatically, and have been a major support to the bull market.

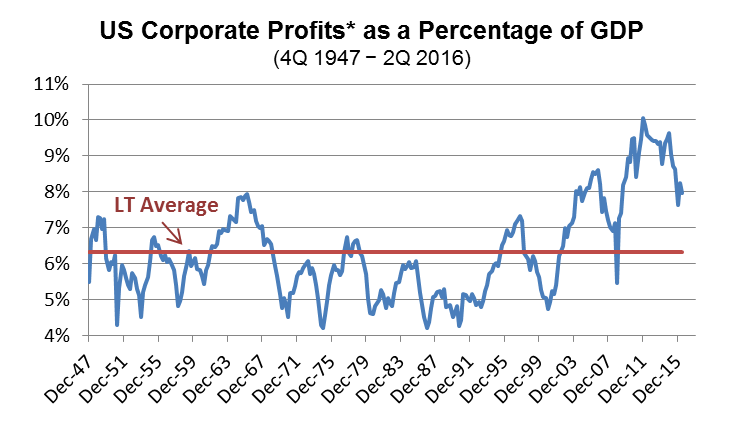

Chart 2 shows corporate profits’ proportion of GDP through time. Although there are some quirks to these particular figures, one should focus on the trends in the data rather than on the numerical figures. As one can see, corporate profits became the largest proportion of GDP ever in history. One certainly would have been bullish a decade ago if one had posited that corporate profits would be the fastest growing portion of national income.

The chart strongly supports the notion that the bull market is not solely attributable to the Fed simply inflating the value of financial assets. Rather, it suggests that the constitution of the current bull market is much more normal than bulls would suggest. Most bull markets are comprised of the combination of central bank liquidity, improving fundamentals, and negative sentiment. All three have been present during this bull market.

Source: Richard Bernstein Advisors LLC, BEA *US Corporate Profits after tax with IVA and CC Adjustments

When do bear markets start?

We recently read yet another article of a famous investor risking his entire hedge fund on massively bearish positioning. Although we don’t for a second doubt that there will be bear markets in the future, such extreme pessimism seems premature to us until the typical bear market signals begin to appear.

The three major signs that the probability of a bear market is increasing have historically been:

- The Fed and other central banks withdrawing liquidity from the global economy.

- Profits recession.

- Overly bullish sentiment.

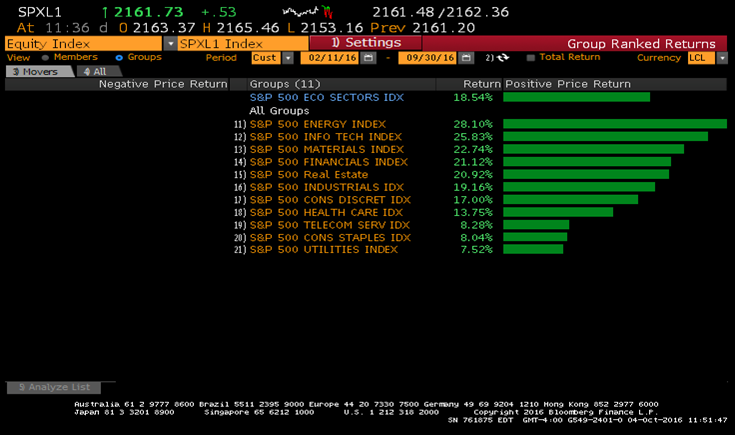

None of these are present today. Although the Fed is considering raising interest rates for the second time in this tightening cycle, there is little evidence that global liquidity will be constrained. Rather than entering a profits recession, the US profits cycle is in a recovery phase and the stock market’s leadership has shifted away from defensive sectors toward cyclical ones. Chart 3 shows S&P 500® sector performance since the February market trough. As we pointed out earlier, sentiment remains quite bullish as it is very hard to find any data that suggests investors are euphoric about investing in US stocks.

Source: Bloomberg Finance L.P.

It’s just a bull market. Get over it.

When we formed Richard Bernstein Advisors in 2009, we highlighted that we thought the US equity market was entering one of the biggest bull markets of our careers. The current bull market is now the second longest bull market in the post-war era, and we still feel the bull market will be one for the record books by the time it is over.

The notion that the only reason the stock market has appreciated is because of the Fed seems blatantly untrue to us, and ignores the significant improvement in fundamentals during this cycle.

Investors will eventually get over their fears and realize that it is simply a bull market, but that doesn’t seem to be happening yet. For the time being though, fear continues to dominate.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

© Copyright 2016 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.