The ongoing shift (along with expectations of slow Fed rate hiking) has pushed short-term funding rates higher as lenders face decreased demand for short-term instruments: The London Interbank Offered Rate (Libor) has spiked to 0.87% currently from just 0.33% a year ago, and we don’t expect Libor to recalibrate back to levels seen earlier in the year anytime soon. So what we see is lenders, investors and asset managers adjusting to a true structural change in funding rates – one that will benefit those investors willing to evaluate and embrace this new paradigm.

On the other side, we believe those who don’t adapt and who keep overallocating to government money market funds will continue to suffer. Paltry net returns (near 0%) will only look worse when the Federal Reserve chooses to move rates higher. And inflation continues to edge upward. This is notable because over most of the 40 years prior to the global financial crisis, investors in money market funds received handsome positive nominal returns that not only moved up when rates were rising, but also often exceeded inflation. But owing to the structural changes in the market, a positive inflation-adjusted real return for money market fund investors is likely becoming a distant memory.

Do these reforms have a direct impact on the ETF market specifically? And what role might ETFs play in the resulting asset shifts?

Zahradnik: For the first part of the question, the short answer is no. The new rules apply only to money market funds, so their impact on ETFs is more indirect, in that we could see demand pick up for ETFs positioned to offer an effective alternative for cash and liquidity management.

ETFs provide the benefit of both portfolio and price transparency, given that holdings are posted daily and the funds trade on exchanges at market prices throughout the day. ETFs have always featured floating NAVs, which are calculated at the end of each trading day. Additionally, investors in ETFs avoid the potential for liquidity gates that will accompany prime money market funds following the reform. With these factors in mind, we believe the reform could shift some of the prior demand for prime money market funds to short-duration ETFs that meet investors’ needs for liquidity and capital preservation.

What are you seeing now with Treasury index ETFs, and how should investors think about their use versus actively managed ETFs for cash management?

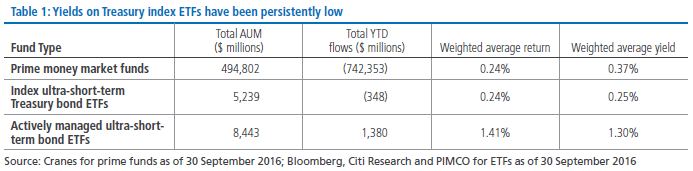

Zahradnik: The big issue for pure Treasury index ETFs is that yields continue to be suppressed. Although flows for these funds have been mixed, in aggregate they have seen outflows in 2016 to date. That may seem counterintuitive, given the recent moves into government securities. But because yields on three-month Treasury bills have continued to compress, return potential for Treasury ETFs has been very low, even considering these funds’ generally low fees. Over the past few years, yields on Treasury ETFs have barely exceeded total expenses; and while the Fed’s December 2015 rate increase led to a slight uptick, yields remain low (see Table 1). So we can expect low returns to persist for pure passive Treasury index ETFs that have limited ability to deviate from their indexes, given that reform-driven demand for the underlying bonds will keep the pressure on yields.

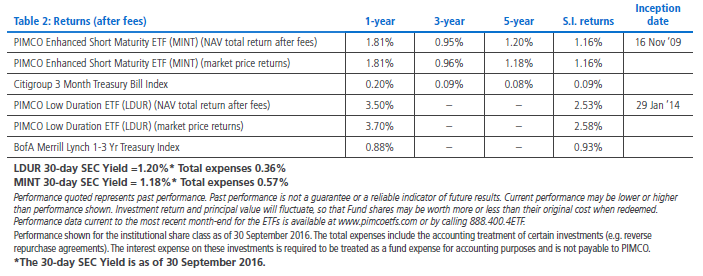

Given these considerations, we believe actively managed ETFs invested in securities beyond the index and able to take advantage of reform-driven dislocations in the market may be the better choice in the current environment. Options such as PIMCO’s MINT (Enhanced Short Maturity Active Exchange-Traded Fund) and LDUR (Low Duration Active Exchange-Traded Fund), which target short-term or short-duration investments outside the scope of regulated money markets, may be attractive to investors looking for money market alternatives and who can tolerate modestly higher volatility than that in government money funds. Short-duration ETFs like MINT and LDUR emphasize capital preservation, but because they have the flexibility to trade in assets beyond regulated money markets, they can exploit targeted opportunities for enhanced yield and total return potential. And an active, risk-focused approach helps to limit volatility while still taking advantage of pockets of value outside the benchmark. These attributes may appeal to investors who are seeking to go beyond simply maintaining par to protect their purchasing power.

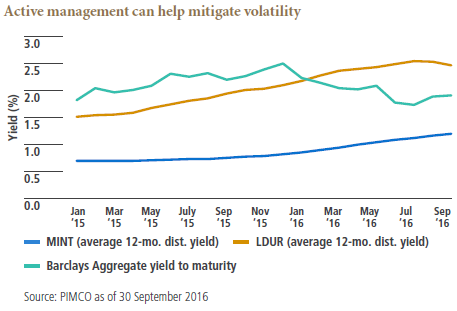

In a world where exposure to interest rates is a major source of volatility for many portfolios, especially at the front end of the yield curve, active management may help mitigate that risk with the goal of producing potentially better risk-adjusted returns (see chart).

What other considerations would you point out to ETF investors?

Schneider: It’s more important than ever for investors to understand an ETF’s strategy for risk and return management and to have a good understanding of its actual investments. For instance, does the ETF invest in high yield? Does it take non-dollar positions? We believe, for example, that floating rate assets linked to Libor may be a good bet right now because banks will likely continue paying relatively higher funding costs as a result of structural changes. We hold these securities in both MINT and LDUR. However, floating rate index ETFs that do not employ rigorous credit analysis and size their holdings based on the issuer’s amount of debt outstanding can have unintended risks.

Investors also must fully understand the strategy behind these funds. Is the fund sufficiently focused on maintaining purchasing power, in addition to providing liquidity and preserving capital? In a “lower for longer” interest rate reality where traditional money market funds have failed to deliver returns that exceed inflation, this has become paramount.

Lastly, it’s important to consider an ETF’s track record, longevity and management team. Has it benefited in past cycles from responsive management, performing well against its benchmark while mitigating volatility? Time-tested short-duration ETF strategies like those behind PIMCO’s MINT and LDUR, which aim to maximize cash potential while protecting against rising rates, may offer an attractive solution to investors in the new reality of liquidity management. Independent evaluators including Morningstar and Lipper have recognized PIMCO's short-term team, which manages these ETFs, for the long-term performance of many strategies as well as the portfolio managers’ tenure, diversified skill sets and active management of liquidity through diverse market conditions. With more than 30 years managing liquidity-minded portfolios, our goal is to help our clients successfully balance their needs for liquidity and true purchasing power preservation.