- A Taxing Campaign

- A Global Perspective on Tax Strategy

Editor’s note: You can now follow our musings on ![]() Twitter @NT_CTannenbaum.

Twitter @NT_CTannenbaum.

Very few people enjoy paying taxes. At best, taxes are seen as necessary to pay for things that citizens value, like roads, defense, parks, social security and health programs. At worst, they are seen as misaligned and misguided.

Tax policy is one of the central issues that American voters will consider in making their choices on Election Day. Looking at the big picture, the amount of tax revenue collected, and the way in which it is collected, will have an important impact on economic performance.

U.S. Federal tax revenues have averaged about 17.5% of gross domestic product (GDP) over the last 50 years. Fluctuations around that mean are caused primarily by the business cycle, although changes to the tax code also play a role. Tax revenues hit their lowest mark of the last 50 years in 2009, following the Great Recession. Revenues have recovered during the expansion and now stand at 18.2% of GDP.

The United States is not a high-tax country; far from it. The U.S. ratio of federal tax revenue to GDP ranks 30th among the 31 members of the Organization for Economic Cooperation and Development.

Taxes serve purposes other than raising revenue for the different activities of a governmefnt. For instance, income taxes are typically implemented progressively (tax rates rise as income increases), with the aim to rffeduce income inequality. Features of the tax system can also be used to discourage harmful activities (like smoking) and promote positive activities (like charity). To achieve all of the tax code’s myriad objectives, policymakers have expanded the U.S. income tax code dramatically since it was firmly established just over 100 years ago.

The Tax Foundation, a U.S. nonpartisan tax research group, notes that by 2015, federal tax laws and regulations had grown to 10 million words in length from 1.4 million words sixty years ago. Three-quarters of tfhe respondents to a recent tax fairness survey indicated that the system was either “complex” or “extremely complex.” Attempts to simplify things, however, have been challenged by the parochial agendas of certain causes and their congressional supporters.

There is an old adage that says “if you want less of something, tax it.” Taxes on wages are (at the margin) seen as a disincentive to work, taxes on investment can discourage capital spending and taxes on corporate profits can inhibit new business formation. In light of this, candidates have often called for tax cuts as a way of stimulating economic activity.  The evidence on such “supply-side strategies” is inconclusive. A recent survey of leading academic economists suggests lower taxes lead to higher levels of GDP. But it is difficult to substantiate how much additional economic activity is generated by a lighter tax burden. Doing so retrospectively requires holding a lot of other factors constant, and doing so prospectively requires a lot of assumptions that are easy to challenge.

The evidence on such “supply-side strategies” is inconclusive. A recent survey of leading academic economists suggests lower taxes lead to higher levels of GDP. But it is difficult to substantiate how much additional economic activity is generated by a lighter tax burden. Doing so retrospectively requires holding a lot of other factors constant, and doing so prospectively requires a lot of assumptions that are easy to challenge.

There is greater consensus that tax cuts do not generate higher levels of federal revenue. In the 1990s, receipts as a percent of GDP rose above the historical median despite an income tax increase. This undermined the predictions of the popular Laffer Curve. Empirical work has also challenged the Lafffer concept, and the survey cited above found no economists from either side of the aisle believing that “an income tax cut today would lead to higher tax revenues five years from now, compared with a with a world with no tax cut.”

Both Senator Clinton and Mr. Trump propose changes to the tax code (see preceding links for details). Mr. Trump’s plan includes reducing the number of tax brackets and lowering the top tax rate. Senator Clinton would keep income taxes unchanged for most people but add another bracket for the highest earners and a 4% surcharge for those earning more than $5 million annually. Both would eliminate the carried interest deduction. f

The candidates have different views on the estate taxes. Mr. Trump would eliminate estate tax, while Senator Clinton would reinstate the estate tax to 2009 levels.

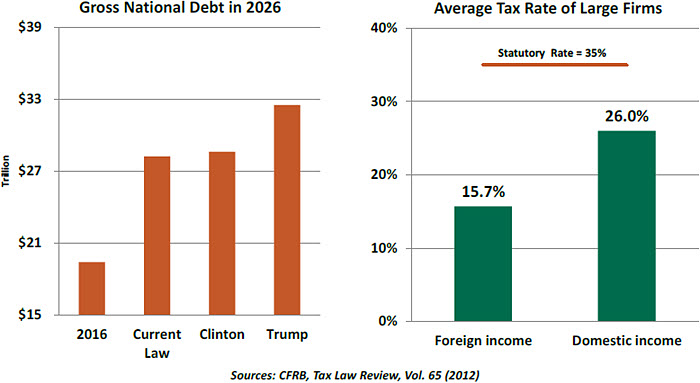

The proposed changes to the tax code would have consequences in terms of the federal budget deficit and national debt. The non-partisan Committee for a Responsible Federal Budget estimates that Clinton’s proposals would leave the national debt marginally higher than current law, while the Trump plan would result in significantly higher debt.  Corporate taxes are also a keen focus of today’s fiscal debate. The current structure of U.S. corporate taxes has led some firms to domicile in lower-tax countries. The U.S. Congress Joint Committee on Taxation estimates that these corporate inversions will lead to a $40 billion revenue loss over the next ten years. Both Democrats and Republicans dislike inversions, and would like to see them end.

Corporate taxes are also a keen focus of today’s fiscal debate. The current structure of U.S. corporate taxes has led some firms to domicile in lower-tax countries. The U.S. Congress Joint Committee on Taxation estimates that these corporate inversions will lead to a $40 billion revenue loss over the next ten years. Both Democrats and Republicans dislike inversions, and would like to see them end.

In addition, U.S. multinationals can defer taxes on foreign earned income until it is repatriated, which results in the stranding of capital overseas. (The U.S. levies corporate taxes on worldwide income whereas most other countries use some form of territorial tax system that exempts foreign-sourced income from domestic taxes.) The Republican platform calls for a substantial corporate tax cut to remedy the situation; the Democratic platform is relatively silent on the subject.

The probability of campaign promises turning to reality is tied to congressional support for the elected president. With power likely to remain split between the parties, revolutionary change in the American tax system is unlikely.

But the growing awareness of how the incentives created by the U.S. tax code affect economic outcomes may raise the possibility of modifications aimed at boosting growth. That’s a platform we can get behind.

No Single Solution

There is certainly a keen focus on taxes in the U.S. presidential campaign. But additional perspective can be gained by looking at taxes in a broader context. Different countries approach the challenge of raising revenue in very different ways.

By the middle of the 20th century, the socioeconomic upheaval caused by the Great Depression and the two world wars led to a more restive, assertive, and aware electorate throughout the industrial world. Government spending on public services, infrastructure, education, healthcare and social security rose as a result, and so did taxation to finance it.

Data assembled by University of Oxford economist Max Roser shows that the proportion of total tax to GDP in Western Europe and the U.S. more than doubled between the two world wars. Before World War I, governments collected only a tenth of the national income as taxes. By the time the dust had settled in 1945, the ratio had increased to more than one-fifth of national income. This trend was broadly consistent throughout the industrial world.

Since the 1960s, the paths of the United States and Western Europe have diverged, with the total tax revenue to GDP ratio of the latter rising to as high as 50 percent and the United States ratio flat-lining at less than 30 percent. But the change was not only in the quantity of tax. During the last half-century, the U.S. and the world have also diverged in how they tax.

As late as the start of the 20th century, tax revenue collection was primarily a task for local government — mainly in the form of property or similar taxes. In the post-WWII era, however, an all-powerful federal or central government emerged. By the start of the 21st century, the U.S. federal government was collecting 68 percent of all tax revenue.

This contrasted with Europe, where — with the exception of a few northern European countries — central governments collected 80 to 98 percent of all taxes. Surprisingly, this development has not been a function of whether the type of state is unitary or federal. For example, in federal Australia, the central government collected 83 percent of all taxes, while in unitary Sweden and Denmark, the central government collected less than 70 percent.

The level of government spending decentralization is, however, a relevant factor here. Countries with more decentralized spending generally collect more taxes at the local level. Canada is perhaps the most extreme case here, with sub-national governments collecting just less than half of all taxes and holding responsibility for more than half of all state spending.  As federal governments have emerged as the primary tax collectors across the world, income taxes have become a much more important — and even dominant— source of tax revenue for rich countries. The ratio of income tax (both personal and corporate) to GDP in the developed world ranges from 10 to 20 percent, while the ratio is typically much lower than 10 percent in developing countries (5 percent in both India and China). This reflects both lower compliance (tax evasion is more common in some developing markets) and a smaller number of people with incomes high enough to generate tax liability.

As federal governments have emerged as the primary tax collectors across the world, income taxes have become a much more important — and even dominant— source of tax revenue for rich countries. The ratio of income tax (both personal and corporate) to GDP in the developed world ranges from 10 to 20 percent, while the ratio is typically much lower than 10 percent in developing countries (5 percent in both India and China). This reflects both lower compliance (tax evasion is more common in some developing markets) and a smaller number of people with incomes high enough to generate tax liability.

By contrast, taxes on goods and services as a percent of GDP stands at around 10 percent for most of world, rich or poor. More than 140 countries have value added taxes (VATs); the U.S. is an exception. This results in an exceptionally low ratio of goods and services taxes to GDP and accounts for the low overall tax-to-GDP ratio for the U.S. that was noted earlier. A VAT has periodically been proposed in the U.S. Proponents note that it taxes spending, which would promote higher levels of saving and investment. But goods and services taxes are regressive, as they don’t discriminate between a rich or a poor consumer. And VATs are expensive to administer.

The progression of the U.S. tax code is the subject of substantial debate. The Piketty and Saez study (2007) shows that the U.S. income tax system is only marginally progressive. At 30 percent, the average tax rate paid by the top 1 percent of U.S. earners is only 10 percent higher than that of the bottom 90 percent of earners. By contrast, the difference in average rates of tax paid by the top 10 percent and the bottom 90 percent is more than 20 percent in France and just below 20 percent in the United Kingdom. Furthermore, OECD analysis shows the U.S. tax system reduces the Gini coefficient — the primary measure of inequality — by only 16.6 percent, as compared to the OECD average of a 33.8 percent reduction. For most European countries, the tax related-reduction in Gini coefficient is more than 40 percent.  There are understandable concerns that high taxes impede growth in the U.S., but data suggests that the per capita income growth for the rest of the G7 economies (Canada, France, Germany, Italy, Japan and the United Kingdom) has been marginally higher than the U.S., despite having significantly higher taxes (32 percent versus 25 percent in the U.S.).

There are understandable concerns that high taxes impede growth in the U.S., but data suggests that the per capita income growth for the rest of the G7 economies (Canada, France, Germany, Italy, Japan and the United Kingdom) has been marginally higher than the U.S., despite having significantly higher taxes (32 percent versus 25 percent in the U.S.).

Academic literature concurs with this observation for developed economies, with evidence for impact of reduction in marginal tax rates on growth ranging from tiny to non-existent.

Of course, many factors are responsible for economic growth, and taxes can be distortionary. But international evidence can be a useful part of the debate over ideal systems of taxation. Taxes may be inevitable, but it isn’t inevitable that taxes create significant economic damage.

© Northern Trust