- Decision Day for Italy

- The ECB Has Done Enough

- Confusing News on the U.S. Labor Market

Claire Meier of our European fixed income team reports from London on Sunday’s referendum in Italy.

The electorate is back at the controls of the ballot box rollercoaster this weekend with the Italian referendum on senate reform. This event is an important one, but it seems like a ride at a kiddie amusement park when compared to the steep twists of fate we’ve seen in the United Kingdom and the United States.

The referendum will have critical implications for Italy, of course, as its government could collapse next week. But it is also a warm up for Dutch, French and German elections next year. The populist tide that has been washing over world capitals since June may flood the Via Appia.

Italy has the eurozone’s third-largest economy, and one of its most anemic. Growth has been very slow, unemployment remains stubbornly high and national debt relative to gross domestic product (GDP) is higher than every other European country except Greece. Most observers agree Italy desperately needs structural reform, but its Byzantine form of government hinders such efforts. The country has had 65 governments in the past 71 years.

The reform itself tries to address this instability by subjugating the Upper House to the directly elected Lower House in hopes of avoiding the political gridlock that has historically crippled reform implementation. The referendum would:

1. Cut the number of senators from 315 to 100. Ninety-five members would be elected by regional councils, with the remaining five appointed by the president (a non-partisan head of state).

2. Cut the legislative duties of the Upper House by changing the ordinary procedure of legislation to bypass a final vote in the Upper House.

3. Eliminate the ability for the Upper House to participate in confidence votes on the government.

The decision has morphed from its specific purpose to a referendum on reform, put forth by Prime Minister Matteo Renzi in an attempt to streamline the legislative process. The voting is also seen as a referendum on Renzi’s leadership, the economy in general and the status of the political class.

Concerns about the banking sector are also at the forefront of voters’ minds. Italy’s banks have been crippled by bad debt and their share prices have been under pressure. Their inability or unwillingness to extend fresh credit has been one factor in Italy’s ongoing malaise.  Renzi would like the flexibility to offer support, but the European Union’s (EU) Bank Recovery and Resolution Directive requires bank debtholders to accept losses before public money can be infused. Renzi has been unable to secure leniency from the EU directive. This leaves the electorate at risk, as their pensions and other investments are tied up in their banks. The close relationship between the banking sector, local governments and the central government further complicates both the banking sector resolution and the referendum.

Renzi would like the flexibility to offer support, but the European Union’s (EU) Bank Recovery and Resolution Directive requires bank debtholders to accept losses before public money can be infused. Renzi has been unable to secure leniency from the EU directive. This leaves the electorate at risk, as their pensions and other investments are tied up in their banks. The close relationship between the banking sector, local governments and the central government further complicates both the banking sector resolution and the referendum.

The resulting anxiety has not helped Renzi’s standing and has hindered the chances of his referendum’s passage.

While the Italian economy continues to suffer under the weight of the banking sector, the market is getting used to the banking sector dysfunction just as Italian sovereign investors recognize the challenges that have been in place for a long time in that space.

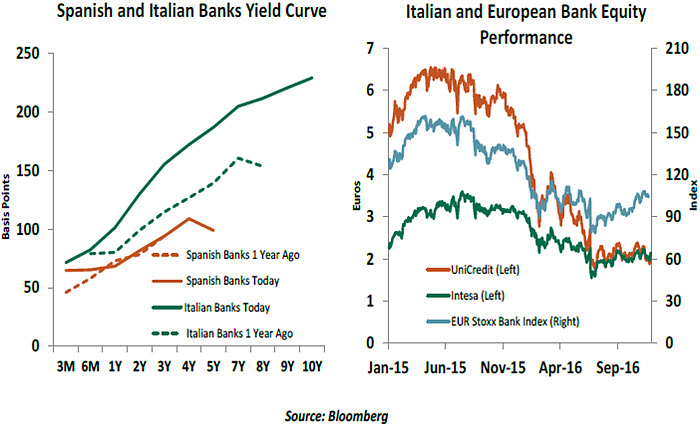

A look at the share prices of the large Italian banks UniCredit and Intesa, plotted against the EURO STOXX Banks Index, shows bank equity investors have been hesitant on Italian names for a while now. A comparison of the yields on Italian bank bonds and Spanish bank bonds also demonstrates that over the past year, Italian bond spreads have widened, driven by a deteriorating environment and lack of any resolution; while Spanish bank bonds have stayed firm despite the country having no government in place for most of 2015.

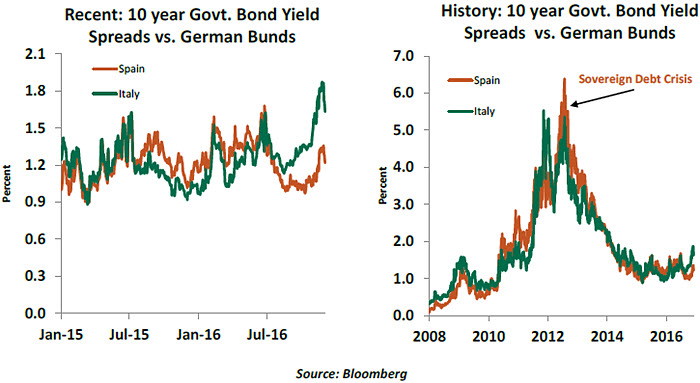

Current yields on Italian sovereign bonds don’t suggest panic because, regardless of the vote, little will change in Italy in the short term and sovereign European investors know that. Throughout the sovereign debt crisis in Europe, Spain and Italy traded within a narrow band of each other depending on political and economic developments on a spread basis to German Bunds; that relationship continues today.

When individual risks in the one country outweighed the other, the country’s bond spreads would trade positions. In June, at the beginning of the Italian referendum process, Italy’s bond spreads widened compared to Spain’s as the individual risk increased, but that is now reversing.

Based on the latest polls, the odds are stacked against the referendum passing. Last month, Prime Minister Renzi repeated his threat to step down if the referendum failed. His departure would likely not pave the way for Italy’s populist party, the Five Star Movement, to take power. But markets might certainly take renewed Italian instability as another data point in the trend away from conventional regimes that seems to be spreading across the globe.  Nonetheless, the Italian referendum does not represent a real threat to the EU. The Italian referendum is significant to domestic politics and the speed of addressing the banking sector, but it is not an indication for the future of Europe. The sovereign market reflects that low risk. We’ll all have to wait until the Dutch, French and German elections to see where the EU stands.

Nonetheless, the Italian referendum does not represent a real threat to the EU. The Italian referendum is significant to domestic politics and the speed of addressing the banking sector, but it is not an indication for the future of Europe. The sovereign market reflects that low risk. We’ll all have to wait until the Dutch, French and German elections to see where the EU stands.

Time to Look beyond QE

Sometimes, whole regimes come to be defined by a single act or a statement. Former European Central Bank (ECB) President Jean-Claude Trichet will go down in history as the man who tightened policy in haste and likely precipitated the European sovereign debt crisis.

Incumbent Mario Draghi would be remembered for a simple, but equally potent, phrase – “Whatever It Takes”. “It” was the preservation of the euro, and “whatever” amounted to a commitment to supply liquidity on demand that later resulted in quantitative easing (QE). On that essential, though narrow, benchmark, the ECB has succeeded. But has it delivered on the more prosaic goals of monetary policy such as price stability and growth?

One of the challenges in assessing the impact of a policy is the lack of a valid counterfactual. One may point to low inflation in Europe and wonder about QE’s achievement. But we cannot know that inflation wouldn’t have been lower, or even negative, without QE. Still, some conclusions can be drawn.

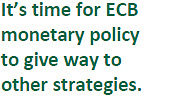

There is sufficient evidence for the ECB to claim victory on what we generally consider the channels of transmission: lower credit spreads and higher asset prices. Both have delivered balance sheet relief and stable inflation expectations. Evidence is more equivocal on real activity. For instance, the latest data suggests that lending to the nonfinancial corporations has now risen to the same level it reached in mid-2011 — an undeniable improvement, but hardly enough to pull the eurozone out of its low-growth trap.  You can take the horse to water, but cannot force it to drink. Monetary policy can fix price signals, but cannot ensure that economic activity will respond. There are many reasons why businesses and households have not stepped forward, including an uncertain economic outlook, lack of visible growth opportunities, political and policy uncertainty and a prioritization of balance sheet repair.

You can take the horse to water, but cannot force it to drink. Monetary policy can fix price signals, but cannot ensure that economic activity will respond. There are many reasons why businesses and households have not stepped forward, including an uncertain economic outlook, lack of visible growth opportunities, political and policy uncertainty and a prioritization of balance sheet repair.

Fiscal actions will provide a more direct and effective strategy for picking up the private sector slack in investment and consumption. Indeed, Mario Draghi has been very vocal in calling for both fiscal stimulus and structural reforms. Just this week, he lamented, "If supported by decisive action taken by other policymakers – monetary policy measures in the euro area could be even more effective"

In its latest economic outlook, OECD recommended an expansionary fiscal path for Germany, Austria, Finland, the Netherlands and France. A growth boost is desperately needed amid the prevailing wave of discontent and populism in much of the western world, and a fiscal stimulus can do the job for now.

But long-term challenges such as non-existent productivity growth, ageing population, low labor force participation, labor market inflexibility in southern Europe and missing pieces in the monetary union’s architecture cannot by addressed by blunt macroeconomic stimulus. While it may not be time for the ECB to retreat, it is time for it to pass the baton.

On Track for Tightening

The November U.S. employment report points to continued favorable labor market conditions. The details and overall tone of employment numbers present no hurdle for the much- anticipated December increase in the U.S. Federal Reserve’s (Fed’s) policy rate.

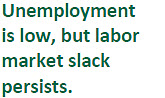

The unemployment rate surprisingly fell to 4.6% in November. The broad unemployment rate (U6) dropped to 9.3% in November vs. 9.5% in the prior month. Both these numbers are at new cycle lows. The number of job leavers as share of the unemployed (12.5%) is larger than the peak seen in the previous business expansion.  Although the number of unemployed declined, the reduction in the labor force (-226,000) played a central role in bringing down the jobless rate. Large swings in the labor force are not uncommon and a rise in the unemployment rate next month would not be surprising.

Although the number of unemployed declined, the reduction in the labor force (-226,000) played a central role in bringing down the jobless rate. Large swings in the labor force are not uncommon and a rise in the unemployment rate next month would not be surprising.

Details show that there are opportunities for further improvement in the labor market, as gains remain asymmetric. The jobless rate of those with lower educational attainment is a source of concern. The polarization of the labor market implies that things are not so rosy for the less-educated and the less-skilled.

Payroll employment increased 178,000 and downward revisions reduced employment by 2,000 during September and October. The increase in employment was broad-based, with the goods sector adding 17,000 jobs and private service sector hiring moving up 139,000. Professional and business services (+63,000), and education and health (+44,000) posted relatively large increases. Government employment rose 22,000 during November compared with a 7,000 increase in the prior month.

The 3-cent dip in average hourly earnings to $25.89 was unexpected. It translates into a 2.5% year-to-year increase, which is lower than the 2.8% gain seen in October. It appears to be a one-off event that is likely to be reversed soon given the solid status of the labor market.

There is little to stop the Fed from moving the federal funds rate 25 basis points higher at its December meeting. The latest unemployment rate is below what the Fed considers full employment (4.7%-5.0%). The Fed’s September Summary of Economic Projections has the median unemployment rate at 4.6% in 2017. With these numbers in mind, the Fed’s forecasts published at the December meeting and its rhetoric about the labor market will be especially interesting.

© Northern Trust