Policies that could nudge rates lower

Quite a few aspects of President-elect Trump’s potential policies might actually work toward lowering the natural, or equilibrium, interest rate rather than increasing it.

What’s known of Trump’s plans to lower personal and corporate tax rates, abolish the estate tax and roll back some of the regulations in financials and energy would tend to increase income and wealth inequality further. The wealthy can and do save more than the needy, so this would add to rather than subtract from the savings glut.

Curbing immigration and sending back undocumented workers would tend to reduce U.S. labor force growth and thus potential output growth further. Of course, those sent back or not able to immigrate into the U.S. might then be employed outside the U.S., adding to global potential output growth. However, with productivity levels in most home countries of actual or potential U.S. immigrants lower than U.S. levels, this implies a net loss to global potential growth.

Major factors unlikely to change

Whatever Trumponomics will look like exactly, it will be unable to affect some of the other secular drivers of the global savings glut.

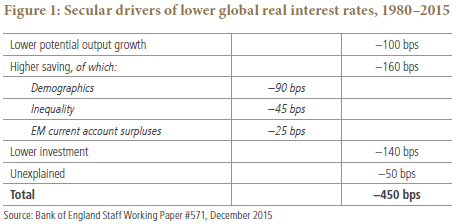

Global demographics, one of the major drivers, is a given. And when it comes to domestic U.S. demographics, Trump’s plans to curb immigration along with the well-documented trend toward increasing longevity and rising labor force participation of wealthy, high-saving individuals above 65 years of age (see Matt Tracey’s and my In Depth article, “ 70 Is the New 65”) both work to increase rather than lower the savings glut.

Moreover, trying to reduce large EM, Japanese or German current account surpluses – another source of global excess savings – through renegotiating bilateral trade deals is likely to be futile. The current account surpluses of these countries reflect an excess of domestic saving over domestic investment. If, say, the U.S. managed to make imports into the U.S. more expensive and exports more competitive through tariffs or a VAT-like destination corporate income tax, the U.S. dollar would simply appreciate to erase the tax- or tariff-induced gain in competitiveness because the underlying saving and investment pattern in the rest of the world wouldn’t change. And so the current account deficit of the U.S. and the surplus of other countries wouldn’t change. To be sure, affecting sectoral and bilateral surpluses and deficits is possible through trade or tax policies, but trying to change the overall aggregates is like Don Quixote’s vain fight against windmills.

Similarly, some of the drivers of lower global desired investment are unlikely to be reversed by Trumponomics. Smarter technology makes much traditional capital investment obsolete. And even if Trumponomics manages to bring manufacturing jobs back to the U.S. through trade and other policies (a big “if”), the higher domestic business investment in these sectors would likely be canceled out globally by lower investment in these sectors abroad.

Turning the secular tide in interest rates?

Where and how could Trumponomics reverse the factors that have worked toward lowering the natural real rate of interest, and how meaningful would the reversal be? One potential avenue is through raising U.S. potential output growth, the other is through a much larger fiscal deficit caused by a combination of tax cuts and higher infrastructure and/or defense spending, which could absorb some of the ex ante excess savings of the private sector, including the EM/Japan/German current account surpluses.

Regarding U.S. potential output growth, I explained above why labor force growth, one of the two factors driving potential output, is more likely to slow than increase under Trump due to immigration policies. Labor productivity growth is the other factor, and this is where Trumponomics could potentially be positive. A bulk of research suggests that the main factor limiting labor productivity growth is the decline in capital deepening, i.e., weak business investment. It is certainly possible that a combination of corporate tax cuts, deregulation of capital-intensive sectors such as energy, and protectionist measures to support the capital-intensive manufacturing sector could raise capital expenditures (capex) and thus productivity over the next several years. However, the gains would probably be slow in coming and it remains to be seen whether corporate tax cuts won’t be used primarily for mergers, acquisitions, share buybacks and higher dividends. Also, keep in mind that higher capex in U.S. manufacturing would likely be at the expense of capex elsewhere in the world.

So how about infrastructure spending and a higher fiscal deficit absorbing more of the global excess savings? Looking at the infrastructure plan advanced by Trump’s economic advisors, the idea seems to be to finance the bulk of the higher spending not through higher government borrowing but through tax credits for (wealthy, I guess) private investors. This raises the chance that many of the investment projects would not be additive but merely projects that would have been undertaken anyway, and they could also crowd out other private investment. Moreover, it remains to be seen whether the deficit hawks in the U.S. Congress will agree to a major widening of the budget deficit.

New paradigm? Not yet

In summary, while I started out by stating that I’m of two minds about the “new paradigm” thesis, nothing clarifies one’s own thinking like writing it down. So for now, my tentative conclusion is that the secular forces holding down global growth, inflation and interest rates remain strong and that Trumponomics is unlikely to change them in any significant way, unless we get a massive increase in government-debt-financed infrastructure spending.

However, this doesn’t mean the sell-off we’ve seen in global rates is irrational, for two reasons.

First, as I noted in the PIMCO Blog a few weeks before the election, it seemed most investors around the world were worshipping at the secular stagnation church and markets had actually undershot PIMCO’s 2% New Neutral fed funds rate. This irrational despondency is now being corrected.

Second, my arguments above relate to secular trends, which I tend to believe won’t be affected by Trumponomics in any meaningful way. However, cyclical swings around long-lasting, slow-moving secular trends can be quite vicious. For example, as my former colleague Gerard Minack pointed out recently (Downunder Daily: Setbacks Amidst Secular Stagnation, Minack Advisors, 22 November 2016), amidst a secular stagnation trend Japanese bond yields doubled in 2003 and quadrupled over a three-year period, before declining again for the rest of the decade and beyond until recently. And most of Trump’s economic plans would tend to support a cyclical rise in inflation, as I wrote following the election.

A new (?) paradigm, a new president, the push-pull of global secular and cyclical trends: plenty of food for discussion at PIMCO’s upcoming investment forum. As always, following the December Cyclical Forum we’ll share our outlook for the global economy for the coming year.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world.

©2016, PIMCO.

© PIMCO

Read more commentaries by PIMCO