The major secular investment theme during the past eight years was global deflation. However, the post-bubble secular period of deflation and slow nominal growth now seems to be ending, and re-inflation could be a prime investment theme for 2017. We hope to take advantage of that important shift because consensus portfolios generally remain positioned for stagnation and deflation rather than for stronger nominal growth.

The deflating global credit bubble left the world with massive productive overcapacity, bloated financial sector balance sheets (See Chart 1), and little incentive for capital investment. Central banks were faced with a textbook “liquidity trap”, and credit creation remained moribund regardless of how low central banks set interest rates or how wildly their balance sheets expanded. Most investors wouldn’t take risk because they were too fearful that 2008’s bear market would repeat, despite that the economic environment was quite good for financial asset appreciation.

However, this past summer’s hackneyed theme of “lower for longer”, meaning that interest rates would stay lower for longer than investors might expect, might prove to be the swan song for the deflation investment theme. Secular global stagnation and deflation probably ended last February, and our portfolios have been positioned for improving nominal growth for much of 2016. Our positioning, which still seems quite out-of-consensus judging by other “year ahead” reports, will likely become consensus as 2017 progresses.

S&P 500® Diversified Financials - Total assets cut by 2/3rds since the bubble

Source: Bloomberg Finance L.P.

“Lower for longer?”

Investors are typically the most bullish about an asset class in the very last stages of a bull market. To use a baseball analogy, investors become most bullish with 2 strikes on the batter with 2 outs in the bottom of the 9th inning. Rather than leaving the game early to beat the traffic from the stadium parking lot, investors stay firmly in their seats sure that there will be extra innings.

Investors were most bullish about Technology stocks in March 2000 and the most bullish on housing in the fall of 2007. The “New Economy” and “housing never depreciates” were the widely accepted economic themes with 2 outs and 2 strikes in the bottom of the 9th.

This past summer, it was “lower for longer” with respect to interest rates, and bond bulls declared that the global economy would remain under deflationary pressures. Few investors made the “lower for longer” claims five or six years ago because investors feared central bank policies would produce rampant inflation (Remember the TV commercials that had central bank buildings with mouths that vomited printed money?). The “lower for longer” theme became popular last summer when the economic backdrop finally began to meaningfully change.

Investors’ rabid fervor for bonds and income during 2016 might ultimately prove to be the bond market’s equivalent of March 2000’s over-enthusiasm for technology stocks or 2007’s for housing stocks.

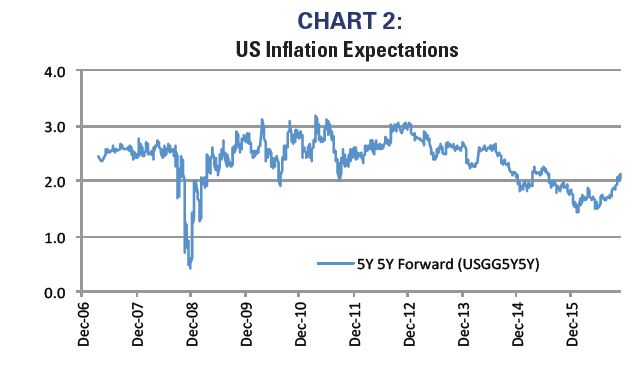

US inflation expectations troughed last February

We shortened the duration of our fixed-income investments some time ago because inflation expectations were forming a trough. In fact, as Chart 2 points out, inflation expectations, measured using the Fed’s supposed favorite measure of inflation expectations, actually troughed last February.

The upcoming administration has so far argued for the largest Keynesian stimulus package since the Depression, and thus the upward move in expectations for inflation and nominal growth has accelerated. The new administration’s economic package might not match that promised during the campaign, but it seems reasonable to assume that there will be more fiscal stimulus rather than less, and that the positives of fiscal stimulus will be greater than the potential negatives from the normalization of monetary policy and rising interest rates.

US Inflation Expectations

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P

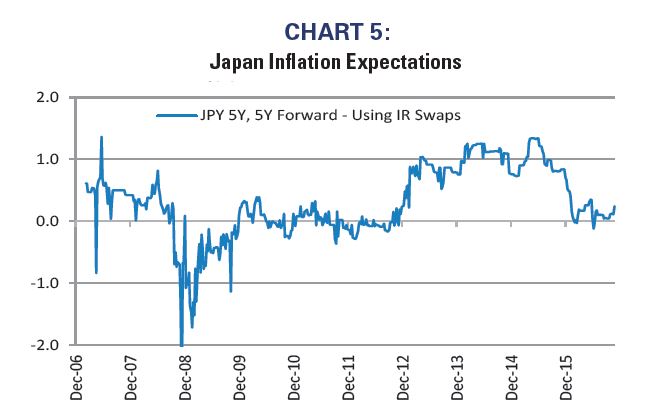

The reevaluation of potential inflation has occurred as well outside the US. Charts 3 through 5 demonstrate that inflation expectations have troughed in the UK, in Germany, and in Japan. The global economy is changing and may finally be recovering from the credit deflation’s crushing pressures.

UK Inflation Expectations

Germany Inflation Expectations

Japan Inflation Expectations

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P

The global economy is improving

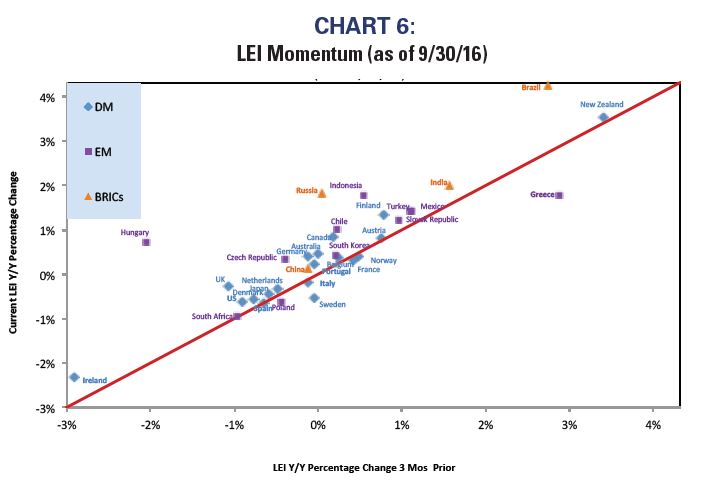

The global economy might still be in secular stagnation (although we are increasingly doubtful), but cyclical acceleration is clearly underway. Leading economic indicators (LEIs) around the world are strengthening in a unified manner that hasn’t existed since the credit bubble.

Chart 6 shows the relationship between the current global LEIs to those of three months ago. If a country lies above the diagonal line in the chart, then the rate of change in that country’s LEI is stronger than it was three months ago. If a country is below the line, then the rate of change is deteriorating. Most LEIs are improving in unison, which indicates broad improvement in the global economy and an increasing chance of rising interest rates over the next year or so.

LEI Momentum (as of 9/30/16)

Source: Richard Bernstein Advisors LLC, OECD

Yield curves are steepening

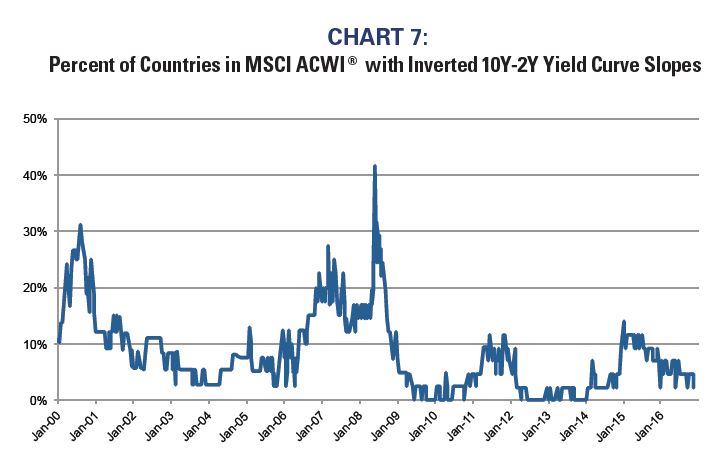

The slope of the yield curve is one of the most reliable indicators of future nominal growth. Steeper curves forecast faster nominal growth, flatter yield curves forecast slower

growth, and inverted yield curves forecast recession.

Global yield curves are steepening, which supports the forecasts of global leading indicators. Chart 7 shows the percentage of global yield curves that are inverted (i.e., forecasting a recession). In 2008, 41% of global yield curves were inverted. Currently, it is only 2%. The US yield curve, for example, has been steepening for 5 months.

Steepening global yield curves imply that most investors’ asset allocations are inappropriate, and are too defensively positioned. Our research has argued for nearly 30 years investors should emphatically overweight bonds and extend duration when the yield curve inverts. Investors’ enthusiasm for bonds this past summer (i.e., lower for longer) seems quite counter to that research. They myopically looked for income despite rising inflation expectations and a steepening yield curve.

Percent of Countries in MSCI ACWI ® with Inverted 10Y-2Y Yield Curve Slopes

Source: Richard Bernstein Advisors LLC, Bloomberg Finance L.P

Our positioning

We began to reposition our portfolios for improving global nominal growth beginning in the first quarter of 2016 and, if we are correct regarding the improvement in the global economy, we expect our views to become consensus during 2017.

As of now, our equity portfolios remain overweight cyclical, smaller capitalization, and lower quality stocks along with emerging markets, while remaining underweight non-US developed markets. Because inflation expectations appear to have troughed, short duration remains the primary theme within our fixed-income holdings and we maintain modest weights to gold and gold miners.

The world is changing

This summer’s “lower for longer” rush for fixed-income and income-oriented equities ignored that deflation appears to slowly be giving way to re-inflation. Although some of our themes have become incrementally popular since the election last month, our overall positioning still seems quite out of consensus.

Investors could be surprised in 2017 by the strength in the nominal economy, and might have to significantly reposition their portfolios toward more cyclical investments.

© Copyright 2016 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors