Cash to Chips, Bricks to Clicks

- Cash to Chips, Bricks to Clicks

- Brexit Looks Harder Than Ever

- Is There Renewed Hope for Capital Spending?

My first job was in the planning department of Marshall Field & Co., a Chicago merchant founded in 1852. The flagship store on State Street housed nine floors of apparel, furniture, books, appliances, toys and fine foods. The holiday season wasn’t complete without a visit to Field’s.

The company had a wonderful mail-order catalogue, but the majority of sales were done in-person and in cash. You saved throughout the year to pay for gifts; banks offered “Christmas Club” accounts for this purpose. Field’s had its own in-house charge card, but users rarely carried significant balances from month to month.

We thought we had a pretty good view on the future of our industry, but we could not have possibly comprehended the change that was to come. Today, people who visit stores in city centers and pay with cash are considered anachronisms. The evolution in how and where people make purchases has had a pronounced impact on the global economy.

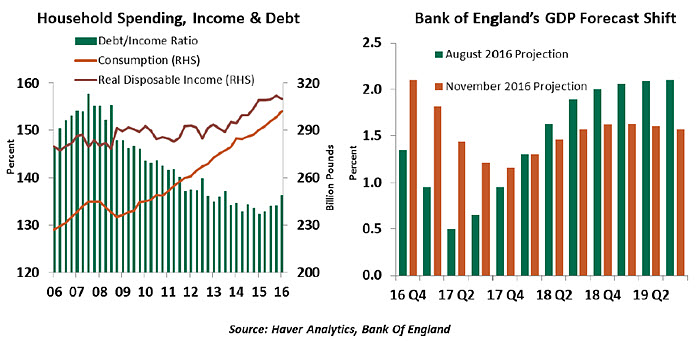

Consumption is the largest share of gross domestic product in all of the world’s developed markets, and consumption by developed markets provides export opportunities for emerging markets. Household spending has recovered slowly since the global financial crisis (GFC) for a variety of cyclical and secular reasons.

Chief among them is balance sheet repair. Innovations in payments, including the advance of credit cards and the securitization of consumer credit, have allowed a substantial expansion of household debt. The GFC prompted a reversal of that trend; deleveraging is well underway in many countries, and potentially around the corner for others.

Not surprisingly, countries with the greatest penetration of revolving credit cards (the U.S., Canada, Australia and the U.K. among them) saw the largest increases in household indebtedness in the years leading up to the crisis. In other parts of the world, the use of credit was more restrained, either due to regulation or because of the advance of mobile payments systems where debit transactions predominate.  Credit card balances in the U.S. declined by almost 25% from their peak in 2008 through the first quarter of 2014. Since then, however, card balances have grown more rapidly than incomes. Solid employment and income gains certainly support a renewed use of credit. But sustained periods where credit growth exceeds income growth are not sustainable. One can only hope that debtors and creditors won’t soon forget the hard lessons of the crisis.

Credit card balances in the U.S. declined by almost 25% from their peak in 2008 through the first quarter of 2014. Since then, however, card balances have grown more rapidly than incomes. Solid employment and income gains certainly support a renewed use of credit. But sustained periods where credit growth exceeds income growth are not sustainable. One can only hope that debtors and creditors won’t soon forget the hard lessons of the crisis.

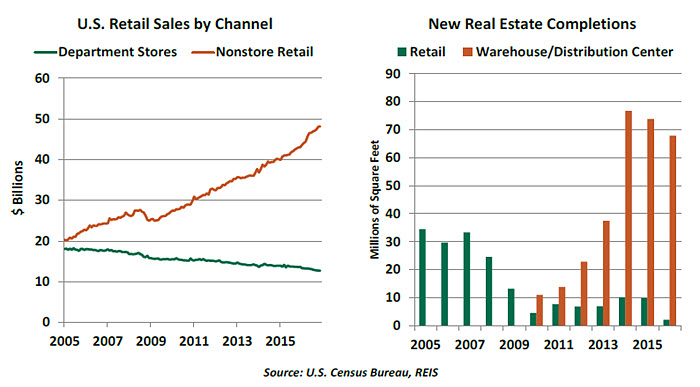

An even more significant transformation centers on where purchases are made. At first, physical outlets followed people to the suburbs, kindling the construction of regional malls and “big box” stores. That model, in turn, is in the process of being disrupted by online merchants that are changing the retail landscape both literally and figuratively.

Online sales compose about 8% of total sales in the U.S., slightly more than the global average of 7.4%. One might be surprised that those numbers are so small, given media coverage of the sector. But many items that we buy cannot be purchased online; gasoline, restaurant meals and motor vehicles are good examples. Removing these items significantly increases the penetration of internet merchants. And analysts expect this trend to extend substantially in the decade ahead.

Traditional merchants, especially those with underdeveloped internet portals, have struggled. Their stocks have slumped and store closures have accelerated. The evolving delivery model has resulted in rising vacancy rates for retail property in many parts of the U.S. and in other countries. The empty parcels cannot be redeveloped easily, leaving blights on many communities. On the other side of things, facilities integral to the shipping of products are popping up with increasing frequency along major highways and in close proximity to regional airports.  Retailing employs 16 million people in the United States and around 150 million people worldwide. The nature of the work done by these individuals has changed markedly. The bookseller who could converse with equal facility on Decartes and Dilbert has given way to “fulfillment professionals” who pack boxes with books people have selected online.

Retailing employs 16 million people in the United States and around 150 million people worldwide. The nature of the work done by these individuals has changed markedly. The bookseller who could converse with equal facility on Decartes and Dilbert has given way to “fulfillment professionals” who pack boxes with books people have selected online.

Average hourly earnings for those in the retail trade are growing more slowly and the hours they work are declining. And as in other areas, those that can develop programs to support online merchants are in high demand while those who remain sales clerks are at risk.

The shift in channels has also affected communities reliant on sales taxes to keep their budgets in balance. Sales taxes account for about 22% of the revenue earned by U.S. state and local governments; the loss of tax proceeds from online sales is estimated to be more than $20 billion annually. This shortfall has been among the contributors to the challenging fiscal situation faced by many regional governments and remains the subject of legislative debate.

The retailing narrative is just one example of the change technology is bringing to a variety of industries. Employees in those industries, and the communities in which they reside, are feeling the consequences of that change. Much has recently been made of the bad influence that international trade has had on American industry, but the true culprit may lie within.

For the first time in a long while, our family did not visit Marshall Field’s this holiday season. (Technically, the store is now owned and operated by Macy’s, but I refuse to refer to it by its new name.) Thanks to my wife’s smartphone, the space under the Christmas tree was amply filled. But somehow, something was missing.

What Brexit Means

For a long while, absence of a coherent post-Brexit negotiating stance with the European Union (EU) had forced the British government to fall back on a tautology: “Brexit Means Brexit.” This week, British Prime Minister Theresa May finally provided some additional definition. May stressed that border security would be the primary objective of her negotiating team. Regaining control over immigration would mean the U.K. leaving the European Single Market.

What will that mean for the U.K. economy? Despite May’s promise for greater certainty, it will be a long time before we know what Britain’s trading arrangements will look like in the post-Brexit era. One thing that now seems certain is the loss of “passporting rights” that allow U.K. financial companies to seamlessly sell their services to Europe. U.K. financial regulators could try to preserve access by retaining rules equivalent to those of Brussels, but this would turn out to be a headache for banks and supervisors alike. The risk to the City of London looks real.

The U.K. government has offered the rhetoric that new trade deals can be struck seamlessly with the rest of world. But consider three things. First, the continent-sized neighborhood market across the English Channel will not be inclined to offer favorable terms when a new trade arrangement is eventually negotiated. Secondly, trade deals can take years to negotiate at the best of times, and a rising wave of anti-trade sentiment around the world will add to the degree of difficulty.  Finally, Ms. May emphasized she’d prefer no deal to a bad deal with Europe, implying that the U.K. was ready to fall back on World Trading Organization (WTO) trading rules. While reasonable on the face of it, the WTO option would rob the U.K.’s service sector — by far the dominant sector of the economy — of the ability to do business with Europe.

Finally, Ms. May emphasized she’d prefer no deal to a bad deal with Europe, implying that the U.K. was ready to fall back on World Trading Organization (WTO) trading rules. While reasonable on the face of it, the WTO option would rob the U.K.’s service sector — by far the dominant sector of the economy — of the ability to do business with Europe.

Our relative pessimism is at odds with both the market’s reaction to Ms. May’s speech and the recent strength of the British economy. Real activity in the U.K. has been solid, defying most post-referendum expectations. Short-term forecasts for the U.K. economy have been raised across the board — no doubt partially buoyed by the change in the global economic sentiment after the U.S. elections.

But it is important to realize that Brexit hasn’t really bitten yet. Either out of wishful thinking that Brexit would never happen, or simple complacency, forecasters have paid scant attention to the difficult mechanics of exiting the EU. As we consider an extended exit window, businesses are in a wait-and-watch mode. As for consumers, a majority of them chose Brexit, so the outcome has not altered their behavior much. Their confidence may ultimately be tested by the coming real earnings squeeze (driven largely by the depreciation of the pound) and overstretched balance sheets.

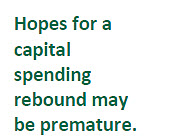

But while the forecasters may have got the timing and pace wrong, there is no doubting the long-term impact of Brexit. Even as the Bank of England (BoE) raised its short term GDP forecast, the U.K. economy is projected to suffer in the long term. With Mrs. May negotiating for a ‘Hard Brexit’, we believe that the BoE’s November projections won’t be far off the mark.

There remain many uncertainties that can only be resolved as negotiations take form. Both houses of British Parliament will vote on the final Brexit deal, but turning back will not be an option. The U.K. government will aim for a reasonably long transition period, but the destination is uncertain. We now have a clearer picture of what Brexit means, and what it means for the U.K. economy does not look encouraging.

Raw Emotion vs. Cold Calculus

U.S. capital spending is likely to show a decline in 2016, a weakness that has trimmed economic growth and held back productivity of the economy. Correcting this trend is a central goal for incoming policy makers.  There is increasing hope that business investment may begin to accelerate. There are two reasons for the optimism. Firstly, economists Robert Shiller and George Akerlof argued in the book Animal Spirits that confidence plays a role in driving economic activity. Consumer confidence has been rising, and business confidence is also much higher since the election.

There is increasing hope that business investment may begin to accelerate. There are two reasons for the optimism. Firstly, economists Robert Shiller and George Akerlof argued in the book Animal Spirits that confidence plays a role in driving economic activity. Consumer confidence has been rising, and business confidence is also much higher since the election.

However, history indicates a mixed record on the link between business confidence and spending (especially over the past several years). And if the sources of recent optimism do not come to fruition, the brighter national mood may prove fleeting.

Secondly, the U.S. corporate tax code features high on the reform list of the new administration. Trump’s campaign proposal of reducing the corporate tax rate to 15% from its current level of 35% would lower costs, and some economic theories suggest the resulting increase in marginal returns will lead businesses to undertake additional investment. There is also discussion about allowing immediate write-offs of a range of new capital spending.

Some have also hoped a tax holiday on profits stranded abroad may increase funds for infrastructure spending and other business investments. Unfortunately, the benefits of a similar tax holiday in 2004 were largely funneled to shareholders in the form of buybacks. That outcome might recur; corporations have already purchased $3.2 trillion of their own equity in the current expansion, significantly more than the $1.9 trillion of equity buybacks in the last expansion.

Additional business spending would benefit the U.S. economy in the short and the long term. But neither of the potential motivations being discussed today is guaranteed to bring about this outcome. As with other proposed policies, it might be best to wait to see the details before getting hopes too high.

© Northern Trust