European Bond Market: What Lies Beyond the Politics?

Although continued political uncertainty looks set to dominate the investment agenda for 2017, much as it did in 2016, David Zahn, head of European Fixed Income, Franklin Templeton Fixed Income Group, feels investors need to take heed of other themes that may be bubbling under the surface in the year ahead. Here he shares some thoughts on divergent central bank policy and divergence in economic growth as well as discussing some of the likely political highlights of 2017.

At a recent roundtable I attended, the participants were almost unanimous in their view that continued political uncertainty will be the dominant theme for markets in 2017.

We tend to agree: 2016 was a very politically charged year, and we think 2017 will be even more exciting, particularly from a European markets perspective. But while politics may dominate the investment agenda in Europe and further afield, it won’t be the only theme for investors, in our view.

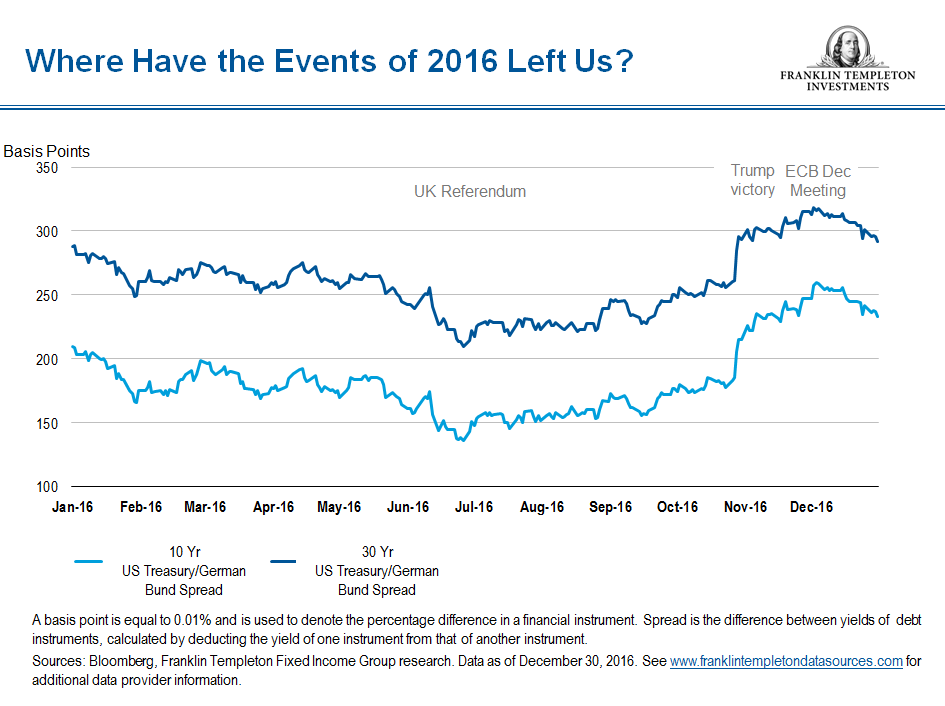

Europe has an interesting story at the moment: over the past six months European government bonds have outperformed US government bonds considerably. The charge began in June 2016 in the aftermath of the United Kingdom’s European Union (EU) referendum, with US bonds starting to sell off in the summer as European bonds remained relatively well-anchored.

As markets started to digest the news of Donald Trump’s victory in the US presidential election, US Treasury yields began to widen while European bond yields remained in place. We think this trend of European bonds outperforming US bonds should continue for 2017 because of political dynamics and central bank policy. In our view, the divergence of central bank policy between the United States and Europe will likely be quite stark this year.

The End of the Bond Bull Market?

A number of market commentators have been asking whether 2017 will spell the end of the bull market for government bonds. They point out that 10-year bond yields for government bonds across much of the world have gone up substantially in recent months, although they remain at historically low levels.

Our view is this trend of rising bond yields won’t continue in Europe. On the contrary, we think bond yields in Europe should remain in a range-bound area, in large part because of the influence of the European Central Bank (ECB).

The ECB, in our opinion, will likely be the driving force behind bond markets in Europe for the next 12–18 months. In December, ECB President Mario Draghi announced the central bank would reduce monthly asset purchases while increasing the program’s duration. We thought this was a smart move.

In essence, it means quantitative easing (QE) should likely continue in Europe into 2018. Significantly, it should push out speculation about whether the bank will extend or taper its QE program until after some of the major political events scheduled for 2017, such as the Dutch, French and German general elections. We consider that to be supportive for the European bond market.

Separately, we believe the ECB has acted smartly to ease concern about the availability of bonds for it to purchase as part of the program. Its decision to alleviate the deposit rate restrictions has opened up a raft of new buying opportunities, including negative-yielding bonds.

A Weak Recovery

While data suggest the European economy is recovering, we consider it a weak recovery, certainly not on a par with the strong recoveries of 2004 and 2009.

What makes that even more disappointing is that it comes against a very supportive background: the ECB has cut rates to historical lows, the euro has weakened significantly, austerity has come to an end in most of the region’s countries and oil prices have been substantially lower than normal.

To have all these tailwinds and still only generate minimal growth suggests the underlying growth is not strong.

French Elections

Unexpected political outcomes—represented by the United Kingdom’s Brexit vote and the US election of Donald Trump—were one of the hallmarks of 2016. That has led commentators to speculate whether Marine Le Pen, leader of France’s far-right Front National party, could triumph in that country’s presidential elections later this year.

Current French government bond pricing suggests markets believe there is a very small chance of Le Pen winning. That leads us to expect some volatility whatever the outcome. We think unfamiliarity with the French electoral system could exacerbate that.

The first round of the French election is scheduled for April 23. It seems very likely to us that Le Pen will get enough votes to get into the second round. If she were to win the primary election, we think some people outside Europe with a lack of understanding about the electoral process might think she’s won the presidency, so we’d expect markets could react in that eventuality. We see that possibility as an opportunity if French government bonds sell off in anticipation of Le Pen doing well.

The actual election is scheduled for May 7.

German Elections

There seems to be a strong consensus that German Chancellor Angela Merkel will retain power in some form after the German elections, scheduled to take place in September 2017.

We’re not convinced that is a certainty. We think she may have to build a new coalition—maybe made up of three parties instead of the current two—which might mean she’s in a weaker position. There’s even a small possibility she might not be leader. We acknowledge that’s a remote possibility but it seems to us that it’s a possibility that markets don’t seem to have considered, and after the experiences of 2016, we think that’s a mistake.

The US Situation

We can see there’s an interesting and intricate political risk landscape in Europe this year. On top of that, we also have to consider the overlay of the Trump presidency across the Atlantic.

Trump doesn’t seem to have a real affinity for Europe, or at least the EU. His attitude towards the North Atlantic Treaty Organization (NATO) also seems ambivalent; earlier this month he referred to the organization as “obsolete.”

From what we do know of Trump’s attitude, we expect his administration will demand European partners make an increased contribution to defense. In particular, it seems likely the United States will want its NATO partners to meet their commitment of spending around 2% of gross domestic product on defense.

On that reckoning, Spain would have to increase military spending four-fold, and Germany would have to double its current outlay. Any increased contribution would either result in higher overall public spending, which we consider could be positive, or from cutbacks elsewhere.

Brexit: A Topic to Itself

Some of you may think it strange that we’ve penned an entire commentary without mentioning Brexit in any meaningful way.

The reason is that we consider it merits a commentary to itself, and we’ll be publishing that in about a week or so. To ensure you don’t miss it, subscribe to our Beyond Bulls & Bears blog in the box above, or click here.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

© Franklin Templeton Investments

© Franklin Templeton Investments