In the latest edition of “Global Macro Shifts,” the Templeton Global Macro team explores Latin America’s failed experiments with populism and the important lessons those experiences have for the developed world. Here, Michael Hasenstab shares a condensed version of his team’s full paper on the subject.

Populism has been on the rise across a wide range of countries in recent years. While populism can mean different things to different people, we use the term to describe policies that promise rapid solutions to problems, often economic in nature, without the pain that typically accompanies more orthodox prescriptions. Traditional policy advice has been to address macroeconomic imbalances using a macroeconomic toolkit consisting, but not restricted to, prudent fiscal and monetary policies, openness to trade, deregulation and a movement toward greater global economic integration.

In the aftermath of the various global crises of the past decade, these traditional remedies are becoming dangerously unfashionable. This has been especially striking in some advanced economies. It contributed to the Brexit vote, where a majority of UK voters opted to take the country out of the European Union (EU) to limit immigration and re-establish a stronger degree of national control over policies and regulations. Populist and nationalist parties have gained popularity in several other EU countries, raising uncertainty for upcoming elections in 2017.

Populist elements have also been strong and vocal in the recent US presidential election on both the Republican and Democratic sides; they have advocated a more inward-looking and interventionist economic focus as well as a more isolationist approach to global trade, with proposals to impose high import tariffs, scrap or renegotiate trade treaties, and curb immigration. Sharp criticism of the North American Free Trade Agreement and of immigration from Mexico signaled a temptation for the United States to turn its back on Latin America. This would be damaging to the US economy, and especially ironic at a time when key Latin American economies are moving in the opposite direction, turning away from populist economic policies to embrace free-market and pro-business reforms.

We have analyzed the experience of Latin American countries over the last several years. We focused mainly on three countries that had embraced populist economic policies: Argentina, Brazil and Venezuela. The former two have recently reversed course, whereas the latter has not. We think comparing their experiences holds some valuable lessons for any policymakers currently at risk of being seduced by the sirens’ song of populism.

Of course, advanced economies are in a much stronger position than the countries covered in this commentary, in terms of both macroeconomic fundamentals and institutions. However, we believe that the economic consequences of misguided policies would be qualitatively similar. In a situation where the temptation of protectionist policies, in particular, is strong, we believe therefore that this analysis can offer some useful guidance. In addition, we underscore the potential attractiveness of investment opportunities in Argentina and Brazil and, more generally, of countries with solid, orthodox macroeconomic policies.

The Sirens of Populism

Exhibit 1 summarizes the experiences of four Latin American countries, three of which (Argentina, Brazil and Venezuela) were lured into the trap of populist policies, whereas one was not (Colombia). All of these countries were hit to varying degrees by the end of the commodity supercycle, and their ability to sustain their respective policy frameworks was tested—those that turned to populism were found wanting. Exhibit 1 to the right provides a snapshot of the kinds of measures deployed by the more interventionist governments.

The Damage

In all three countries that followed populist policies, such policies have brought about significantly adverse consequences: Inflation rose to high levels, the economic system was severely distorted, productivity growth suffered, manipulation of the exchange rate combined with high inflation caused a significant appreciation of the real exchange rate (which undermined competitiveness), and in some cases public debt expanded rapidly.

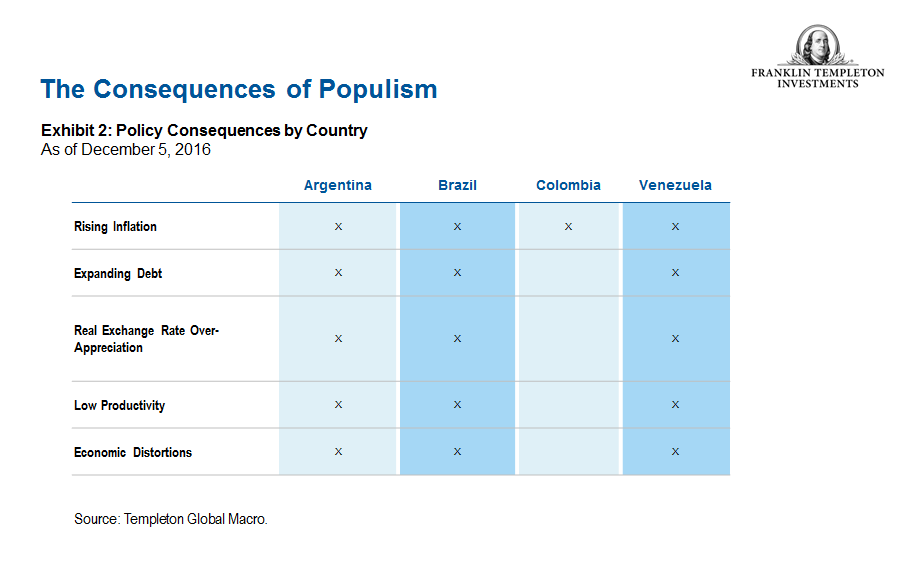

The damage that was inflicted on these economies by the drift away from prudent macro policies is in the process of being reversed in Argentina and Brazil; the experience of Venezuela, which has refused to follow this path, speaks for itself. Exhibit 2 provides a snapshot of the damage suffered by the different countries, with Colombia being the outlier in that it maintained prudent policies.

Reversing Course

In Argentina, the protracted deterioration in economic conditions eventually resulted in the ouster of Cristina Kirchner by Mauricio Macri in November 2015. President Macri was elected on a strong economic liberalization platform. The new government swiftly launched a broad range of reforms, including strengthening institutions, tightening monetary policy, fiscally consolidating, normalizing FX policy, and regularizing international relationships. This strong and broad-ranging reform effort represents a clear departure from the past, and sends a strong signal to international investors that the government is strongly committed to its new economic policy course—we think the willingness to immediately tackle many of the toughest challenges is the most convincing way of establishing credibility.

In Brazil, policy correction was forced upon the former president, Dilma Rousseff, as the market increasingly denied her the financing needed to continue on her unsustainable path and her popularity ratings plummeted. The new Brazilian government, led by President Michel Temer, has pushed forward with the first steps toward fiscal consolidation, lowering the ceiling on public spending and readying a possible reform of social security. The government has also begun to reverse the previous micro-management of the economy so as to reduce policy-induced distortions. One of the biggest steps was to begin deregulating administered prices in 2015. Faced with rising inflation and an economy still in recession, the central bank had to strike a difficult balance in 2015; after keeping the real interest rate stable through mid-2015, it allowed it to creep up (even while starting to reduce nominal rates) to secure a decline in inflation in 2016. A more prudent monetary policy was also manifested in a reversal of the previous credit expansion.

In Colombia, despite the lack of any serious deterioration of policies, the government has actually taken steps to tackle the inflation that resulted from exchange rate depreciation. Monetary policy was tightened; steps have been taken to consolidate the fiscal accounts further to address any potential impact from lower revenues on the back of lower oil prices; and finally, in parallel, negotiations with the Revolutionary Armed Forces of Colombia—People’s Army (FARC-EP) were pursued to end the long conflict with the guerrilla group, further strengthening and safeguarding the democratic institutions of the country.

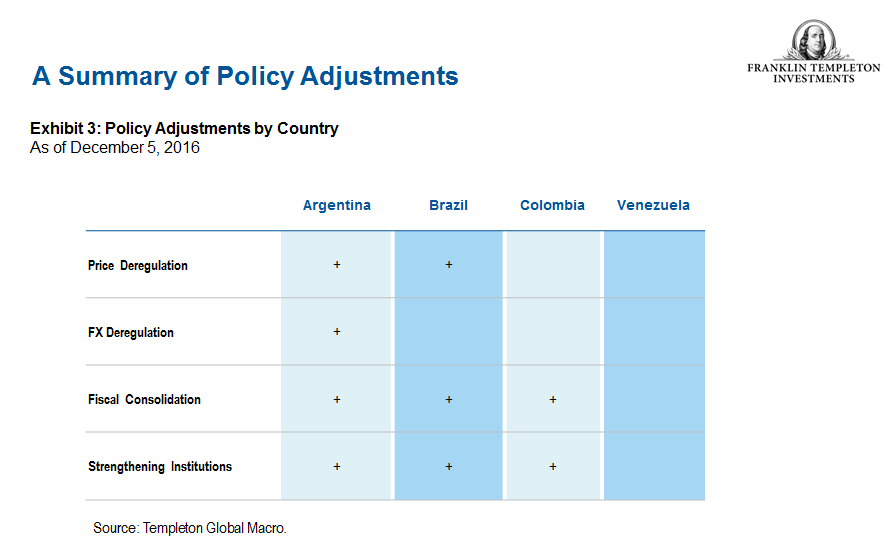

Venezuela’s populist policies are still in full swing at the time of this writing. The population now faces extremely harsh conditions, with high unemployment and a severe lack of food and other basic necessities. This has triggered protests and increased the risk to social stability but has not yet resulted in political change, much less in a policy correction. Exhibit 3 provides a summary of policy adjustments (or lack thereof) implemented by each country.

Forging Into the Decade Ahead

Colombia’s policymaking stands as the mirror image to Venezuela—steadfast in its rejection of populism. It is notable that Colombia, having maintained prudent macro policies, only suffered from the increase in inflation brought about by the depreciation of the exchange rate. A starker contrast is hard to draw.

In both Argentina and Brazil, there are reasons to be optimistic, although the policy correction has just begun. While it will be crucial to maintain the momentum in the coming years, in both countries the most important factor—political commitment—appears to be in place, and if the new policies are maintained, we think the benefits will be substantial.

By contrast, it is hard for us to feel anything but pessimistic about the outlook for Venezuela. It simultaneously has greater oil reserves than Saudi Arabia and the world’s fastest contracting economy, inflation that is estimated to be heading toward 1000%,1 and shortages of food and medicine that are pushing the country toward a humanitarian crisis. It is difficult to come up with a more dire set of circumstances for a country.

These examples that we have drawn from Latin America have important lessons to offer the developed world. While we are not suggesting that the United States or the various countries in Europe that are flirting with populism are at risk of traveling down some of the extreme paths we explore in the full paper, these examples do offer a cautionary tale at a time when orthodox economic policymaking is at risk of falling increasingly out of favor.

The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline.

_____________________________________________

1 Source: IMF World Economic Outlook, October 2016.

© Franklin Templeton Investments

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments