An Economic Look at Deregulation

- An Economic Look at Deregulation

- Beware of Border Taxes

- Capital Flows Complicate Currency Values

Editor’s note: You can now follow our musings on ![]() Twitter @NT_CTannenbaum.

Twitter @NT_CTannenbaum.

In Eastern culture, red symbolizes good fortune. During the recent Lunar New Year, celebrants exchanged red envelopes filled with money and displayed red lanterns to ward off evil. In keeping with the symbolism, we shared a spicy red hot pot dinner with friends. I am not sure my palate has recovered, but no evil spirits have approached me since.

In the West, the color red has a bad reputation. Stop lights are red. Red marks denote corrections in written documents. The devil is drawn in red. Red cards are used to eject players from games.

Among the things most likely to cause someone to see red is a confrontation with red tape, a term used to describe regulation that hinders progress. During its initial weeks, the new U.S. administration has vowed to use a machete to cut through red tape, in the hope of adding momentum to economic growth. The tussle between President Trump and entrenched bureaucracies will be interesting to watch.

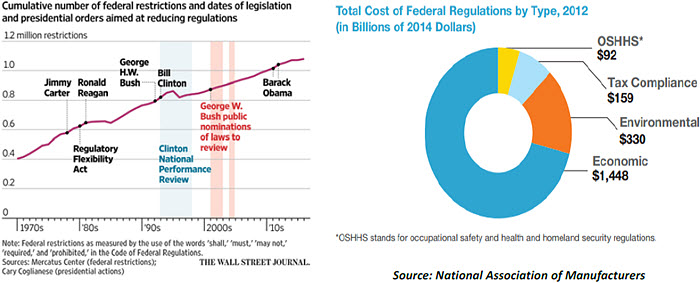

As we discussed last fall, regulation is often well-founded. We want assurances that our food is safe, our water is clean, and our physicians are properly tfrained. Often, however, the translation of these worthy principles into specific language can create unintended consequences. The challenge of complying with thousands of pages of rules can tax businesses. And so American Presidents going back almost forty years have vowed to seek reforms, with limited success.

Once entrenched, bureaucracies can be difficult to unearth. In rare instances where restrictions have been relaxed, others have arisen to take their place.

Doing things the right way is incredibly important. This essay is not intended to be an anti-regulation manifesto. But complying with and enforcing regulation carries costs, which are often passed along to consumers. If the time and money spent are not producing the desired outcomes, they might be better applied differently.  For that reason, there is a school of thought that regulation should be subjected to a cost/ benefit analysis. This is the spirit behind the “Two for One” regulation proposal advanced by the White House. While the quota of removing two regulations for every new one enacted could be considered too specific, reviewing new and proposed restrictions through an economic lens can be useful background for discussion.

For that reason, there is a school of thought that regulation should be subjected to a cost/ benefit analysis. This is the spirit behind the “Two for One” regulation proposal advanced by the White House. While the quota of removing two regulations for every new one enacted could be considered too specific, reviewing new and proposed restrictions through an economic lens can be useful background for discussion.

It isn’t easy to apply cost-benefit analysis to some types of regulation. What price do you put on pollution, or lives saved? While compliance is a four-letter word to some, incomes earned by compliance professionals are spent on products and services offered by regulated firms. Capturing all the effects and after-effects takes care, and an objective eye.

The drive to deregulate has focused on financial services, specifically on the Dodd-Frank Act (DFA). The Act, passed in 2010, was very much the product of the desire for reckoning after the financial fcrisis. The momentum behind the DFA made it a magnet for a range of regulatory desires.

The DFA became a good example of how worthy concepts (in this case, ensuring a safe banking system) can get lost in the translation to written rules. The Act itself was 2,300 pages long, but that was only the start. The law directed regulators to flesh out requirements in several areas; some have estimated that the resulting addenda have increased the size of the re-regulation tenfold.

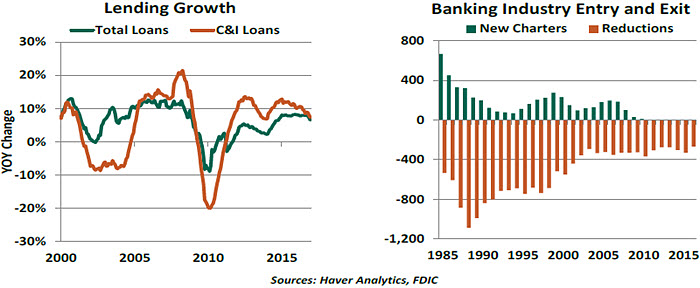

Given its scale and cost, the DFA is a good candidate for a cost/ benefit analysis. DFA detractors have claimed that the added regulations have hindered the flow of credit in the economy and deterred new entrants to the industry. That, they claim, is a core contributor to the sluggish pace of economic expansion.

A critical look at banking trends raises some questions about this line of reasoning. Credit growth, especially directed to small businesses, has been robust over the past few years (and especially so at community banks). Mortgage lending growth has been more modest, but this is a product of household deleveraging and a desire for better balance in housing finance. No one wants to go back to the standards of 2006. There are always anecdotes of potential borrowers being turned away, but the outcome is often a product of their creditworthiness, not excessive regulation.  There have been almost no new banking charters granted in the United States over the past several years, and the cost of compliance with regulation has been blamed for the apparent lack of vitality in the industry. But studies suggest that low interest rates and competition from large bank branches and online financial portals may be a more critical factor.

There have been almost no new banking charters granted in the United States over the past several years, and the cost of compliance with regulation has been blamed for the apparent lack of vitality in the industry. But studies suggest that low interest rates and competition from large bank branches and online financial portals may be a more critical factor.

The Consumer Financial Protection Bureau (CFPB) is also in the cross-hairs of Congress. Financial products can be difficult to understand, and there are instances where purveyors have not always operated in the best interests of their customers. The recent example of Wells Fargo has been used on both sides of the existential debate over the CFPB: at once, it is justification for ongoing oversight and evidence that the regulation is not working.

Legislatively, the DFA will be difficult to overturn. But through the appointment of leadership at financial regulatory agencies, the administration will have the opportunity to set a distinct tone. As a lifelong banker and a former regulator, I hope the policy tone balances the yin of economic advancement with the yang of good financial behavior.

Building a Financial Wall

Borders have become more of a focal point around the world. The international flow of people and products is receiving a great deal of additional scrutiny.

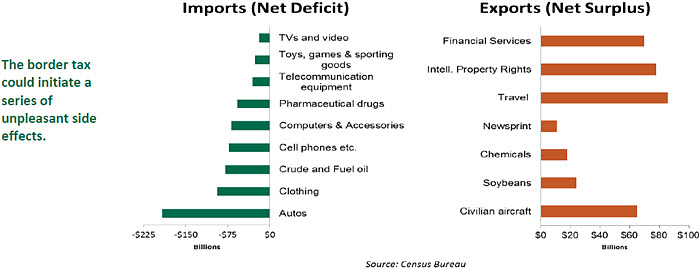

During his first two weeks in office, President Trump used direct decrees to slow the flow of new entrants, issuing orders to build a wall along the Mexican border and suspending immigration from a selection of countries. To deter the excessive flow of goods, softer methods are being contemplated. The border tax is one of them.

The border tax (also known as the “destination-based cash flow tax,” or DBCFT) is simple in concept, but complicated in execution and impact. U.S. firms would no longer be able to consider goods purchased from overseas as costs for tax purposes, which would increase what they owe to the Internal Revenue Service. Exports to overseas purchasers would not count as revenue, which would serve to reduce tax bills.

These elements would create a significant disincentive to source from overseas and a significant incentive to export. It would have an impact comparable to import tariffs combined with export incentives for American producers. Proponents note that the border tax levels the playing field with countries that either have very low corporate tax rates or that use their tax codes to promote exports. It also greatly diminishes the attraction of moving corporate headquarters or profitable operations outside of the United States solely to save on taxes.

Since the United States runs a very large trade deficit, the border tax would (at least initially) be a significant revenue raiser for the U.S. Treasury. Congress may use some of the proceeds to “pay for” tax reductions they might be contemplating in other areas.

As with most things in economics, however, the impact of the border tax would unfold in several stages. There are a number of potential second-order effects that could complicate the outcome.

- Inflation could increase. Imports would cost more, since they would be subject to higher levies. And while some operations are located outside of the U.S. for tax reasons, others are outsourced because of lower costs. If production were re-shored to more expensive facilities, that would also place upward pressure on inflation. The burden of this outcome would likely fall disproportionately to families of more modest means.

If inflation rises significantly, it might prompt higher rates from the Federal Reserve, which could adversely affect both economic growth and the Federal budget.

- The dollar could increase. The border tax would promote exports; foreign buyers would have to acquire an increasing amount of dollars to purchase them. The demand for foreign currencies would go down if U.S. producers brought production back home.

So depending on how strong the dollar gets, the currency markets could serve to offset any realignment that the border tax would have on trade flows into and out of the United States. There is an active academic debate underway on how large this effect might be.

- Other countries could certainly retaliate to offset the prospective impacts of the border tax. This could lead to a “race to the bottom” of competitive devaluations or tax cuts, a contest no one would win. Several countries have already pledged to review their tax systems if the U.S. implements the border tax in an effort to sustain competitiveness.

- Emerging markets reliant on exports to the U.S. and which have debt denominated in U.S. dollars (such as Mexico) would come under significant pressure.

It is often said that some of our key trading partners have been pursuing managed trade, not free trade. Border tax supporters suggest that it would correct trade inequities that have been building for some time. But while simple in concept, the consequences of the border tax could be quite complicated. It warrants careful study.

Capital Trumps Trade

The new U.S. administration has sharpened its rhetoric on trade, tariffs and currency valuation. Two weeks ago, President Trump said the U.S. dollar was “too strong…and it’s killing us.” Such a statement was unusual for America’s chief executive, as the President has traditionally avoided commenting on currencies. But the dollar’s centrality to world commerce means that some of the government’s aims may be incompatible with reality.

This is not the first time that America has tried to steer the value of the dollar downward. The Plaza Accord, signed by major advanced economies in 1985, attempted to make American products more competitive with those produced in Japan and Europe. The Accord succeeded in devaluing the dollar, but the impact on the trade balance was debatable — Japan continued to run a large trade surplus with the U.S. In that case, Japan’s system of industrial promotion proved more powerful than the currency markets.

In the present day, the dollar has once again become very strong against a series of major currencies, despite a persistently deep U.S. trade deficit. Economic theory tells us that a weak trade balance should make the currency weak over time. Net importers need to acquire foreign currency to complete their purchases, which places downward pressure on the local currency. But in the present case, the opposite has occurred.

A key reason why this identity has broken down for the U.S. is that international capital flows have grown exponentially over the last three decades. For those countries that are favored destinations for investors, the persistence of capital inflows creates strong demand for the currency of that country. This limits the ability of governments, or even trade flows, to influence exchange rate values for a sustained period.

Short of a spectacular reversal of global financial integration, a loss of confidence in U.S. markets, or a domestic U.S. recession, the administration is unlikely to be successful in “talking down” the dollar. In this case, speaking softly might be best advised.

© Northern Trust