Given the unpredictability of today’s financial markets, many investors are looking to reduce the impact of market volatility on their portfolios. Hedge-fund strategies—a type of alternative investment strategy—may help by potentially offering additional diversification, new sources of return and reduced risk. K2 Advisors seeks to add value through active portfolio management, tactical allocation and diversification across four main hedge strategies: long-short equity, relative value, global macro and event driven. Here, K2’s Rob Christian discusses why the team favors activist hedge strategies as a subset of the event-driven strategy, and how attitudes toward activist investing have changed.

When describing hedge-fund performance—and more specifically hedge-fund alpha1 —words like “generating,” “producing,” and “creating” are often used. These expressions are somewhat misleading, in my view. They imply that hedge funds, by their own sheer will and determination, can somehow conjure alpha on demand. For the majority of hedge funds this is not the case. Technically speaking alpha is not generated, nor is it produced, manufactured or built. Indeed, for the majority of successful hedge-fund managers, the most that can be expected of alpha is that a fair amount of it may be captured over the course of an investment horizon. That is the key—alpha is largely captured. A good market day for a hedge fund means that the fleeting alpha ghost has had the misfortune of stepping into a cleverly constructed trap—if only momentarily. The nature of alpha is elusive, and that is why investors will pay for it.

The Exception to the Rule

Like all good rules however, there are exceptions. In my view, activist hedge funds represent one such exception. It could be said that activist managers in some ways represent the only strategy that generates alpha to some degree. While not always successful, activist funds seek to unlock “hidden” value in the companies they invest in.

They look for stocks that are trading at a discount to intrinsic value, and then instead of waiting passively for the market to recognize this perceived hidden value, the activist hedge fund will proactively work to expose—or elevate—that value to the market. In this way the strategy quite literally attempts to generate or harvest alpha proactively by promoting the catalysts that may increase stock value.

Activism: A Primer

Briefly, the strategy of activist investing involves taking a minority position in a public company, with the goal of helping unlock said company’s value by influencing management to modify its capital allocation activities. That is, run their businesses in a more efficient and profitable manner. Tactics include financial restructurings, operational turnarounds and/or strategic initiatives.

Implicit in the strategy is the notion that the targeted company is undervalued and generating earnings below its potential (based on the hedge fund manager’s assessment) and the activist has a plan to help unlock this potential.

More than three decades ago, some of the same players in the activist space today may have grabbed headlines under different—perhaps less flattering—characterizations as part of the leveraged buy-out (LBO) frenzy of the late 1980s and early 1990s. Indeed, some of the same iconic names that today are held up as defenders of the average investor, often praised for holding management teams accountable, were in days of yore condemned as “robber barons,” “corporate raiders” and “barbarians at the gate.”

Not anymore. The “barbarians” of the 1980’s no longer crash the gates as much as they wish to repair them.

The game today is more about diplomacy than aggression, as activist investors have found it easier (and clearly more profitable) to work with corporate management to help implement positive change, versus trying to take full control of a company and possibly liquidate its prized assets. In this way, the spoils are shared among many.

Today it is about building venerable brands versus destroying them, and activists no longer need to take over a company to influence action. Often it is possible for a hedge fund with a minority stake (perhaps just over 5%) to initiate change with cooperation from management, possibly by nominating a member of the hedge fund’s team to the company’s board of directors.

As a high-profile activist stated to Bloomberg, “the least effective way to do activism these days is to come in with a big club. The best result is to have a board hear your ideas, realize they are good and then acquiesce…we prefer to work with management in making changes that increase shareholder value, but sometimes you have to go to the mat.”2

All of the tools once used to avert activists in the boardroom, from “poison pills” that derail takeovers to golden parachutes that enrich management, are today generally viewed as negatives for shareholders.

Investor sentiment over excessive compensation levels and lax oversight has shifted moods in favor of activists and away from corporate management. Many investors view the lure of stock options and other cozy perks often available to senior management in public companies as a disincentive to long-term strategic thinking.

Attractive Opportunity

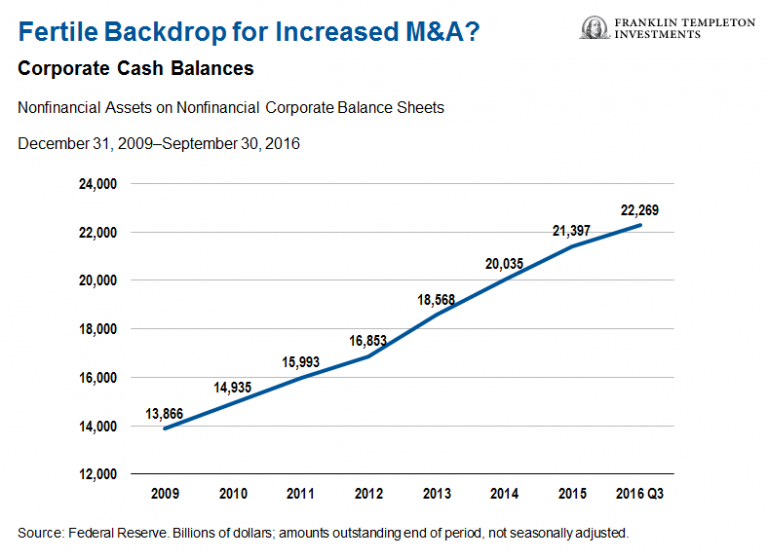

The market and economic environment is perhaps more favorable to activist investment strategies today than it has been in some time. With the outlook for growth muted, corporate balance sheets flush with cash, financing rates still very low, and an increasingly hospitable public attitude toward activist investors—the opportunity set appears robust.

Huge cash balances may create a significant drag on corporate earnings, and many companies will likely choose to allocate this cash through strategic M&A or via stock buybacks and dividends—both significant areas of focus for activist funds.

Management teams may lack the skill set or incentives required to successfully undertake such strategic maneuvers, and this is where we believe hedge funds may find opportunity.

In addition, there remains a substantial amount of uninvested private-equity (PE) capital on the sidelines, much of which is likely to be invested over the next several years (as investment periods expire). We believe this activity should increase opportunities for activist investors to participate in buyouts and other strategic acquisition deals.

Some Final Thoughts on Alpha

When thinking about the unique value I see in activist hedge-fund strategies, I find it helpful to remind myself of the nature and composition of alpha. Alpha is a byproduct of an inefficient market. Mathematically speaking, alpha represents the abnormal rate of return on a security or portfolio in excess of what would be predicted by an equilibrium model like the capital asset pricing model (CAPM). So it is the coefficient—or residual of the expected return of a security—based on the security’s market sensitivity, or beta.

In an efficient market, the expected value of the alpha coefficient would be zero; however, we believe markets are naturally inefficient. As such, if a security returns more than what would be expected given its beta (market sensitivity or risk), it has positive alpha. If it returns less than its beta predicts, it has negative alpha. In other words, alpha is the portion of return that is the result of factors other than exposure to the market. Activist hedge funds seek to not only capture, but cultivate them.

Comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. The identification of attractive investment opportunities is difficult and involves a significant degree of uncertainty and there is no assurance any such alternative investment strategies will be successful. An investment in these strategies is subject to various risks, such as those market risks common to entities investing in all types of securities, including market volatility. It is always possible that any trade could generate a loss if the manager’s expectations do not come to pass.

The market values of securities held in the K2 liquid alternatives portfolios will go up or down, sometimes rapidly or unpredictably Hedge strategy outlooks are determined relative to other hedge strategies and do not represent an opinion regarding absolute expected future performance or risk. Conviction sentiment determined by the K2 Research Group is based on a variety of factors and may change from time to time.

For more information on any of K2’s alternative strategies funds, contact your financial advisor or download a free prospectus. Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. The prospectus contains this and other information. Please read the prospectus carefully before investing or sending money. _____________________________________________________

1. Alpha refers to a risk-adjusted measure of the value that an active portfolio manager adds to or subtracts from a portfolio’s return.

2. Source: Bloomberg, “The Good Barbarian: How Icahn, Ackman, and Loeb Became Shareholder Heroes,” May 14, 2012.