SUMMARY

- The World Can’t Afford to Retire

- Cash Is No Longer King

- Don’t Get Too Concerned About Consumer Debt

Nine months after I started my first banking job, I got an official-looking letter from an insurance company I had never heard of. It informed me that I would be provided with a monthly annuity of about $60 upon my retirement, the result of the bank’s decision to close its pension plan. I filed the letter away without giving it much heed, since retirement seemed a long way off.

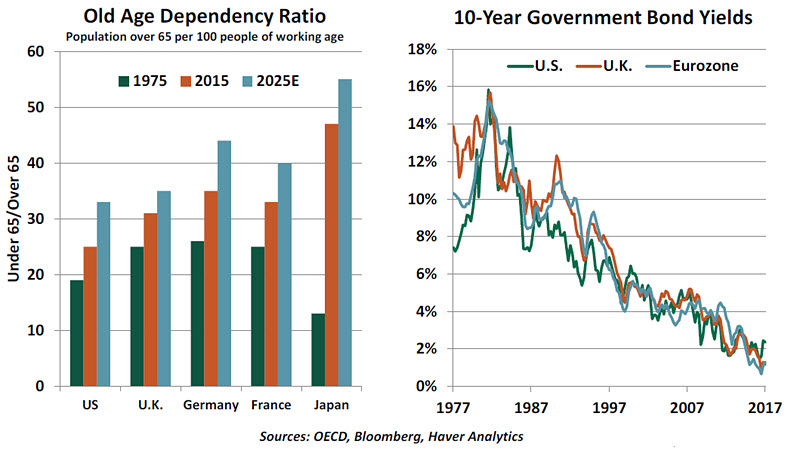

I didn’t realize it at the time, but that event was significant at a micro and at a macro level. The gradual fade of private pension plans has shifted responsibility for retirement preparedness to employees, a responsibility that some have not borne well. For the pensions that remain, the secular decline in global interest rates that began in the early 1980s has created new challenges to solvency. Today, with populations aging, the challenge of fulfilling retirement expectations is an immensely expensive problem.

Pensions are centuries old. Post-retirement payments were often offered as an incentive to military enlistees to fill out the ranks. Governments gradually offered these schemes to the general population as a means of combatting indigence among the elderly. Today, government pensions provide more than 60% of retirement income in the United States and Western Europe.

Corporations began providing pensions to augment compensation packages. In the United States, wage controls implemented after World War II led firms to compete for talent using other means. (Corporate health plans began gaining popularity at around the same time.)

When beneficiaries are young and asset returns are ample, pension systems enjoy robust health. Given long time horizons, programs are free to invest aggressively, without much regard to the timing of prospective liabilities. Under these circumstances, funded ratios (which compare the values of plan assets to the value of benefit commitments) are easy to sustain.

But today, pension systems in the public and private sector are grappling with a perfect storm. With the ranks of retirees growing rapidly, plans have had to shift to fixed income investments just as interest rates are at generational lows. Pensioners are living longer, extending the annuity of benefits owed to them. Funded ratios are consequently slipping.

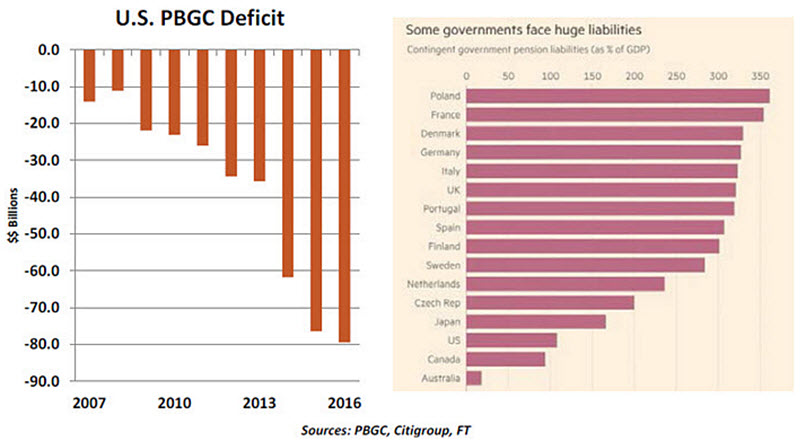

Well managed programs thought ahead, taking risk off the table by setting terms carefully and matching their prospective liabilities. Others weren’t so fortunate. Private sector pension backstops, like the Pension Benefit Guarantee Corporation in the United States and the Pension Protection Fund in the United Kingdom, have seen their caseloads grow and their financial positions tested.

Pensions in the public sector are a particular problem. In this arena, pension contributions compete with other fiscal priorities, and often are limited to keep budgets in balance. (This is a fundamental design flaw.) Proposed benefit reforms meet significant resistance and create a political furor. Aggressive investment strategies, aimed at digging out of the deep hole, haven’t been successful.

As a result, retirement obligations threaten the solvency of U.S. states and some national governments. Pensions remain a point of stress in negotiations over Greece’s debt restructuring, and Brazil must soon enact changes to its national pension plan to avoid a painful reckoning. These are not isolated incidents: a series of governments will need to think creatively to avoid seeing pensions bankrupt their economies.

The consequences of underfunded retirement systems will be wide-spread. Keeping pension promises will require significant amounts of revenue from taxpayers. The monies channeled in this direction will not be available for public investment, and high tax rates can be a deterrent to businesses and residents. Certain areas are already in a demographic death spiral, and others may join them.

Changing benefit formulas as a path to solvency will be exceedingly difficult. Broad communities of people around the world are reliant on their pensions, having set aside relatively little for their own retirements. The strain they feel has been, and will be, expressed at the ballot box. Challenging encounters between local governments and international financiers will likely become more frequent in the years ahead.

Defined contribution plans, which have replaced pensions in many sectors, are no panacea. These plans require participants to make intelligent choices about saving, investing and taking distributions when the time comes. Studies suggest that many struggle with these concepts.

To compensate, behavioral economists have intervened with default selections that participants have to take active steps to undo. This kind of “

nudging” was once looked at as overbearing, but is now viewed as essential to avoiding bad outcomes.

While pension systems have acquired a bad reputation, they do include elements of intelligent design. They relieve individuals of responsibility for decisions they find difficult to make on their own. Pension professionals are in a much better position to do the calculations and formulate the strategies that maximize the chances of retirement security. It’s a shame that some custodians of these structures, primarily in the public sector, have done their constituents such a disservice.

The bill for bad decisions is now coming due. The invoice threatens global growth, creates dangerous generational divides, and invites financial instability. Demographic change and its impact on fiscal positions could be the most significant global economic issue of the coming generation.

My bank was one of the smart ones. By terminating its pension plan when interest rates were near their peak, the company was able to record a sizeable gain. But $60 per month is not going to pay my mortgage. The latest calculations suggest that I will have to work until age 85 before retiring … so you’ll have to put up with my writing for a long time to come.

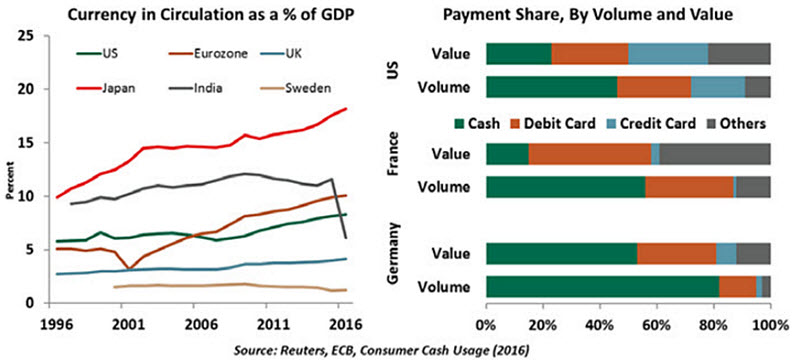

Cashing OutIt seems that move toward “cash-lite” if not “cash-less” systems is accelerating, with a considerable assist from governments.

At the end of last year, the Indian government retired 500 and 1,000 rupee notes ($7.50 and $15 at current exchange rates). The ECB has announced that it will be phasing out the €500 banknotes. Meanwhile, the Bank of England offered reassurance again this week that it has no plans to discontinue its £50 bank notes.

The policy thrust against currency (especially large denomination notes) has been driven by concerns over its use for illicit activity and tax evasion. As well, printing and retiring currency is costly for central banks, and paper currency remains subject to counterfeiting, despite improved designs.

It is

estimated that nearly half of all U.S. dollars and euros are held abroad, a significant portion of which is likely being used for illegal activity. The Internal Revenue Service

found last year that tax evasion in the United States amounted to an annual average of $458 billion between 2008 and 2010, or more than 40% of the combined Federal budget deficit for those years. The problem is even more acute in Europe, where income tax rates tend to be higher, with the European Commission

suggesting that tax evasion levels reached about a trillion euros in 2012, or double the combined budget deficit of EU member states.

India lacks credible estimates of tax evasion or of illicit wealth kept in cash, but indicators such as the disparity between the consumption of luxury goods and the income tax payer statistics suggests that the number is high. Moreover, medium and small businesses in a cash heavy and informal economy like India rely on informal or kinship credit networks that exclude large sections of people. A “cash-lite” economic system backed up by better technological and banking infrastructure can be a nudge to formalize the economy, improve tax collection and expand banking coverage.

Studies suggest that cash is still king for now, or as the Swiss central bank

says, “Reports about the death of cash are not just exaggerated — they are unfounded.” Switzerland is home to world’s most valuable bank note, 1,000 francs ($990), and with the circulation increasing, the central bank has no plan to get rid of it. A

survey found that Germans and Austrians conduct majority of their transactions in cash, even the more pricey ones. Cash by far remains the dominant mode of transaction in the seven countries surveyed. Even in India, the surge in digital transactions during demonetization has largely cooled down.

The popularity of cash can be explained by a number of legitimate factors, including privacy concerns, inadequate technological infrastructure or training, and incomplete availability of banking accounts. The survey suggests that cash is seen as a widely acceptable, cheaper and easier transaction method than debit or credit cards.

However, the survey also reveals that cash is typically used only for small ticket transactions. Thus, any orderly phasing out of large denomination currency in industrialized economies is unlikely to be economically disruptive or even erode the faith in fiat money, as some worry.

Technological progress means that we may move to a “cash-lite” economy whether there is a policy push or not. But it may be a long time before we have no paper in our wallets. In fact, the elimination of larger bills may mean even more paper in our wallets.

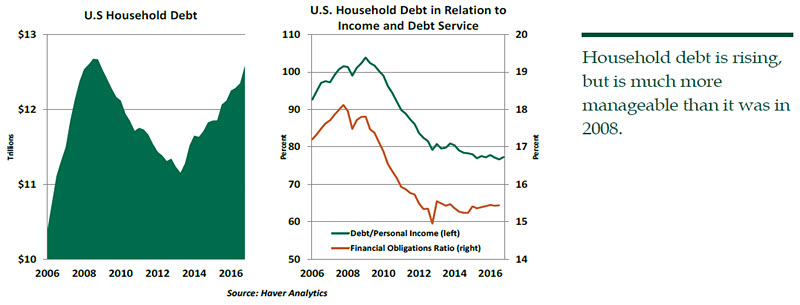

Service MattersThe financial press notes that U.S. household debt is close to the level seen in 2008. On the surface, this might appear to be cause for concern, but there is more to the story. For the time being, personal leverage does not seem to be a threat.

A Pew Center study indicates that 80% of Americans carry some form of debt: mortgages, car loans, unpaid credit card balances, student loans or a combination of these. The deleveraging that followed the Great Recession brought down household debt to its low mark in 2012. It has since advanced and now nearly matches the pre-crisis peak ($12.6 trillion). It is therefore not surprising that the level of household debt caught the eye of analysts.

But the composition of household liabilities is different today than it was in 2008. Mortgage debt is not growing at a rapid pace, and it stands on firm fundamentals. Only 1.6% of mortgage loans are delinquent today, down from a peak of 8.9% in 2010. Household debt is only 13.7% of household net worth, a vast difference from nearly 23% in 2008.

The rate of delinquent auto loans is moving up, while the student loan delinquency rate shows a sideways movement, after a significant increase during the past recession. The rapid growth of auto loans to $1.15 trillion and student loans to $1.3 trillion is being closely watched.

Debt is not harmful to economic growth as long it can be serviced on a timely basis. The important difference between the current situation and the 2008 experience is that the ability to service debt is not impaired now and the share of personal income required to meet debt obligations (the financial obligations ratio) is close to the historical low.

To be sure, the debt situation merits monitoring, and debt service will rise with interest rates. But for now, there is little cause for alarm.

© Northern Trust

www.northerntrust.com

© Northern Trust

Read more commentaries by Northern Trust

Well managed programs thought ahead, taking risk off the table by setting terms carefully and matching their prospective liabilities. Others weren’t so fortunate. Private sector pension backstops, like the Pension Benefit Guarantee Corporation in the United States and the Pension Protection Fund in the United Kingdom, have seen their caseloads grow and their financial positions tested.

Well managed programs thought ahead, taking risk off the table by setting terms carefully and matching their prospective liabilities. Others weren’t so fortunate. Private sector pension backstops, like the Pension Benefit Guarantee Corporation in the United States and the Pension Protection Fund in the United Kingdom, have seen their caseloads grow and their financial positions tested.

While pension systems have acquired a bad reputation, they do include elements of intelligent design. They relieve individuals of responsibility for decisions they find difficult to make on their own. Pension professionals are in a much better position to do the calculations and formulate the strategies that maximize the chances of retirement security. It’s a shame that some custodians of these structures, primarily in the public sector, have done their constituents such a disservice.

While pension systems have acquired a bad reputation, they do include elements of intelligent design. They relieve individuals of responsibility for decisions they find difficult to make on their own. Pension professionals are in a much better position to do the calculations and formulate the strategies that maximize the chances of retirement security. It’s a shame that some custodians of these structures, primarily in the public sector, have done their constituents such a disservice.  Studies suggest that cash is still king for now, or as the Swiss central bank

Studies suggest that cash is still king for now, or as the Swiss central bank

The rate of delinquent auto loans is moving up, while the student loan delinquency rate shows a sideways movement, after a significant increase during the past recession. The rapid growth of auto loans to $1.15 trillion and student loans to $1.3 trillion is being closely watched.

The rate of delinquent auto loans is moving up, while the student loan delinquency rate shows a sideways movement, after a significant increase during the past recession. The rapid growth of auto loans to $1.15 trillion and student loans to $1.3 trillion is being closely watched.