If you’re like most working people, you’ve probably received a statement in the mail from the Social Security Administration listing your potential future benefits. Trying to figure out how Social Security arrived at those mysterious figures requires some detective work. Here, Gail Buckner, CFP, our personal retirement and financial planning strategist, attempts to crack the code. She discusses how your benefit is calculated and offers some strategies on how to maximize it.

Gail Buckner, CFP®

Vice President

Personal Retirement and Financial Planning Strategist

Franklin Templeton Investments

One of the greatest mysteries of Social Security can be summed up in one question: “How much?”

As in, “How much is my benefit going to be?”

A corollary to this: “How is it calculated?”

And another common question: “How much will my spouse/ex-spouse/child/etc., get?”

You will find a wealth of information about “How much?” on Social Security’s website.

Unfortunately, you often have to switch from one page to another, the math can be a bit complicated and the explanations still include too much jargon that dates back to when the system was set up. In other words, it can sound like actuary-speak from the 1940s. As with many government entities, there are also tons of acronyms—PIA, WEP, GPO and OASDI to name just a few. (I’ll let you look those up, if you’re interested.)

What follows is a primer—in 21st century lingo—explaining the most common question: “How much?”

“How Much Will My Benefit Be?”

Though nearly 61 million Americans received roughly $918 billion in Social Security benefits last year, most have no idea how the size of their monthly check was determined.1 Research has consistently found “very low levels of Social Security literacy.”2 Since the overwhelming majority of these individuals received retirement benefits (as opposed to disability or survivor benefits), this discussion will focus on them.

In addition, “How much will my retirement benefit be?” is the top question I get from those who are not yet retired.

In a nutshell, your Social Security benefit is based upon two things: how many years you contributed to Social Security as part of the workforce and what your salary was in each of those years. The latter matters for two reasons: 1. those who earn more pay more in Social Security tax (“payroll tax”), and 2. they receive a higher Social Security benefit. However, the sky is not the limit. If you retire this year at full retirement age (FRA), no matter how much you earned over your career, the maximum check you will receive is $2,687/month.3

Important concept: Based upon the way it is calculated, lower income workers get a better deal from Social Security.4

Surprised? Since its inception at the end of the Great Depression, Social Security’s primary objective has been to keep the frailest and poorest members of our society from living in abject poverty. Initially, this meant the elderly. The 1954 Social Security Amendments expanded benefits to include those who cannot work because of a disability.5

From Social Security’s Depression-era inception, the math that determines the size of one’s benefit is deliberately designed to replace a larger portion of earnings for those who made the least. Presumably, it’s assumed that those at the high end of the income spectrum will probably have other assets, such as investments, retirement accounts, real estate, etc., that can help support them when they retire. For the lowest-paid, however, Social Security is likely all of the income they will have to live on. If it weren’t for Social Security, an estimated 22 million Americans would be living at or below the poverty level—particularly the elderly.6

Step 1: Are You Eligible?

To qualify for Social Security benefits, you must accumulate a minimum of 40 “credits.” You can earn a maximum of four credits per year. This year, you will receive one credit for every $1,300 you earn.7 However, whether you earn $5,200 (4 x $1,300) in a single day or over the entire year, the most you will receive is four credits each year. (Credits used to be based on how much you earned each “quarter,” but this changed in 1978.)

Step 2: What Did You Earn Each Year?

The amount you earn is a key factor in determining what your Social Security benefit will be. Whether you worked full time or part time, at the end of the year your employer reports your total earnings. If you had more than one job, each employer submits a report. In addition, the only jobs that count are those where your employer deducted Social Security tax from your paychecks (or if you are self-employed, you paid the self-employment tax on your earnings).

Step 3: How Many Years Did You Work?

When calculating your monthly benefit, Social Security looks at all of the years you worked and adjusts each year’s earnings for inflation, which converts your older earnings into what the equivalent salary would be today. Then it selects your 35 highest (adjusted) years of work.

Here’s a hypothetical example. Margie is a baby boomer born in June 1954, and she worked at a fast food restaurant the summer after high school graduation. She continued working there during summer breaks and didn’t begin working full time until graduating from college at age 22. Her starting salary was $14,000—a respectable income for a new grad in 1976. She got married at age 28, then had her first child at age 30. At that point, Margie quit her job. Her second baby arrived when she was 33.

Step 4: In What Year Did You Earn It?

Like Margie, when we first enter the workforce most of us start out with a fairly modest salary. Over the years, through promotions or job changes, we (hopefully) earn more money.

In 1993, Margie re-entered the workforce. After her hiatus, she was happy to land a job paying $35,000/year. She took classes at night and earned an MBA. At age 42, Margie was hired for a junior executive job paying $80,000/year. Through hard work and long hours she continued to climb the corporate ladder. In 2016, at age 62, she earns $225,000/year.

The Importance of 35

The first step in calculating Margie’s monthly Social Security benefit is to determine her 35 highest years of earnings. Again, each annual amount is adjusted to reflect how much wages in general have increased. Remember that summer job slinging hamburgers Margie had in 1972? The minimum wage back then was $1.60/hour.8 Since Margie worked 20 hours/week, her paycheck (before deductions) was $32/week. Her gross earnings for the eight weeks she worked that year totaled $256. To determine what this equates to in today’s wages, Social Security multiplies $256 by 6.74, the “national average wage index” for 1972.9 In other words, if Margie had the same job today, her total wages would theoretically be $1,725.44. That’s the amount of earnings she will get credit for.

This same approach is taken for each year of earnings Margie has until she turns 62. From then on, Social Security stops adjusting her earnings for inflation and uses the actual amount her employer reports.

What to “AIME” For

Next, Social Security selects Margie’s highest 35 years of earnings and adds them up. Then this amount is divided by 420, the number of months in 35 years. This determines her Average Income Monthly Earnings (or AIME) the building block for determining “how much” her benefit will be.10

In Margie’s case, because of the time she was out of the workforce while her children were young, her top 35 years of income would include two very low-earning years when she had that summer job at the fast-food restaurant. However, if she continues working, her more recent and much higher earnings will replace those earlier years. This will significantly boost her AIME.

Important concept: If you do not have 35 years of earnings, a value of “zero” will be entered for each missing year.

From AIME to PIA

Your Primary Insurance Amount (PIA) is the monthly benefit you will get if you wait until you are Full Retirement Age (FRA) to begin receiving Social Security. It is also the number used to determine how much others—such as your spouse, children and/or dependent parents—will receive.

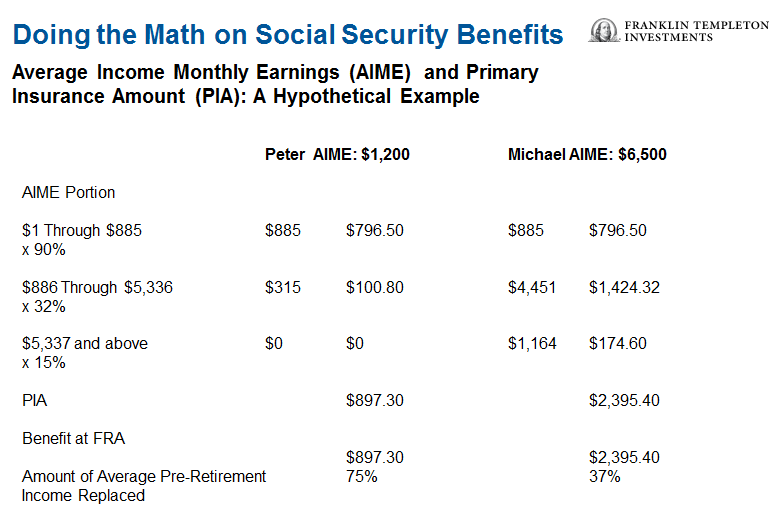

PIA is calculated by breaking up your AIME into up to three amounts and multiplying each one by a different percentage.[11]

For 2017, the steps are:

- Multiply first $885 of AIME x 90%

- Multiply AIME over $885 and through $5,336 x 32%

- Multiply AIME over $5,336 x 15%

- Add up these amounts and round down to the nearest multiple of $0.10

Intuitively, it should be clear from this example that Social Security benefits replace a larger portion of income for those who have made less compared to those whose income was higher. In other words, if your lifetime earnings resulted in an AIME of exactly $885, your PIA would replace 90% of this income. On the other hand, if you had higher earnings over your career, your Social Security benefit will replace a smaller portion.

Here’s another hypothetical example. Peter’s AIME is $1,200 and Michael’s is $6,500. The table below illustrates how their respective PIAs would be calculated. Notice that although Michael’s AIME is nearly 5.5 times larger than Peter’s, his monthly Social Security benefit is only about 2.7 times higher.

Starting Early/Working Longer

Most people are aware that the Social Security benefit they receive depends upon their age when they begin to collect it. You can start as early as 62. However, if you start before your FRA, the amount will be reduced—permanently.[12]

On the other hand, delaying the start of benefits past your FRA increases the size of your check. Let’s suppose your FRA is 66, you are still employed and plan to keep working as long as you can. Since your paychecks cover your financial needs, you decide not to file for Social Security. Every 12 months past the month of your FRA, your benefit automatically goes up by 8% thanks to the Delayed Retirement Credit (DRC). If you postpone starting Social Security until you turn 70, your benefit will go up a minimum of 32% compared to what you would have received at FRA.

In Peter’s case, if he waited until age 70 to start benefits, he would receive roughly $1,184/month instead of $897. In addition, his benefit would also be credited with any Cost-of-Living-Adjustments (COLAs) Social Security beneficiaries received over those four years.

Important Concept: Delayed Retirement Credits stop once you turn 70. So, do not start Social Security any later than age 70!

Spouse Benefits

Since Peter is married, his wife, Stacy, is eligible for a benefit based on his earnings. However, she is not entitled to this until he files. Her maximum benefit is 50% of his PIA, i.e., $448.50. However, Stacy will only get the maximum amount if she waits until she is full retirement age to apply for Social Security. If she files before she is FRA, it will be reduced. On the other hand, spousal benefits do not earn Delayed Retirement Credits, so it makes no sense to claim them later than FRA.

If Stacy earned a Social Security benefit based on her own work history, Social Security will compare this to her spousal amount and assign her whichever benefit is higher. This choice is permanent.

Important concept: Whether Peter starts Social Security before, at or after FRA, his wife’s spousal benefit will be based upon his PIA.

To Sum It Up

Your PIA is the keystone of your Social Security benefit. It also determines how much other individuals—spouses, children, dependent parents—are eligible to receive. The building blocks of your PIA are the number of years you work and, to a lesser degree, how much you earn.

And, ask your professional advisor to run your personal scenario though the independent third-party LifeYield Social Security Optimizer tool, which can help you and your advisor consider your personal goals and circumstances, and begin to determine when the right time to start taking Social Security benefits might be.

© Franklin Templeton Investments

http://us.beyondbullsandbears.com

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments